Remembering Marlboro Friday

The 33rd Anniversary

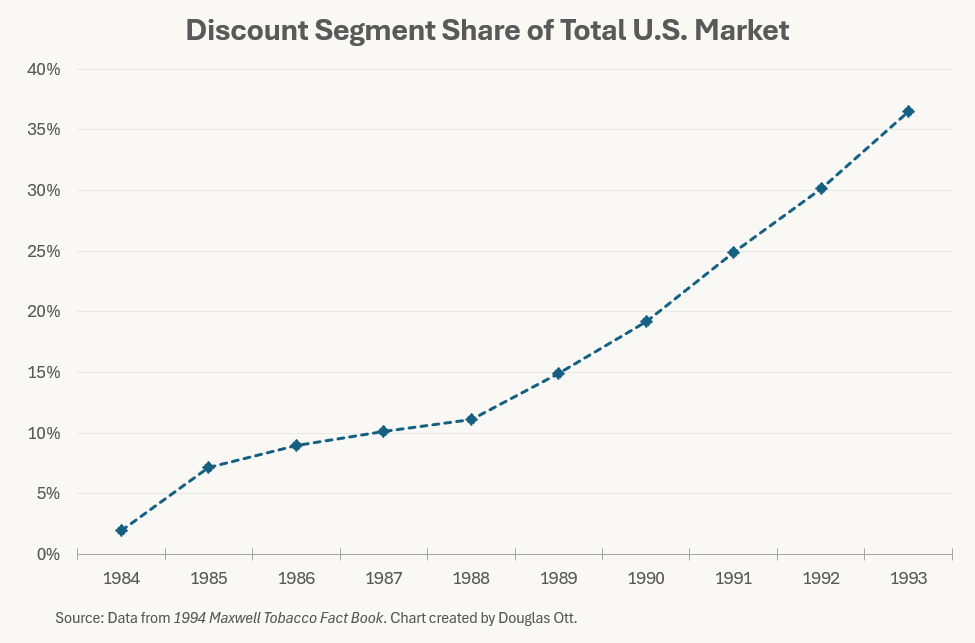

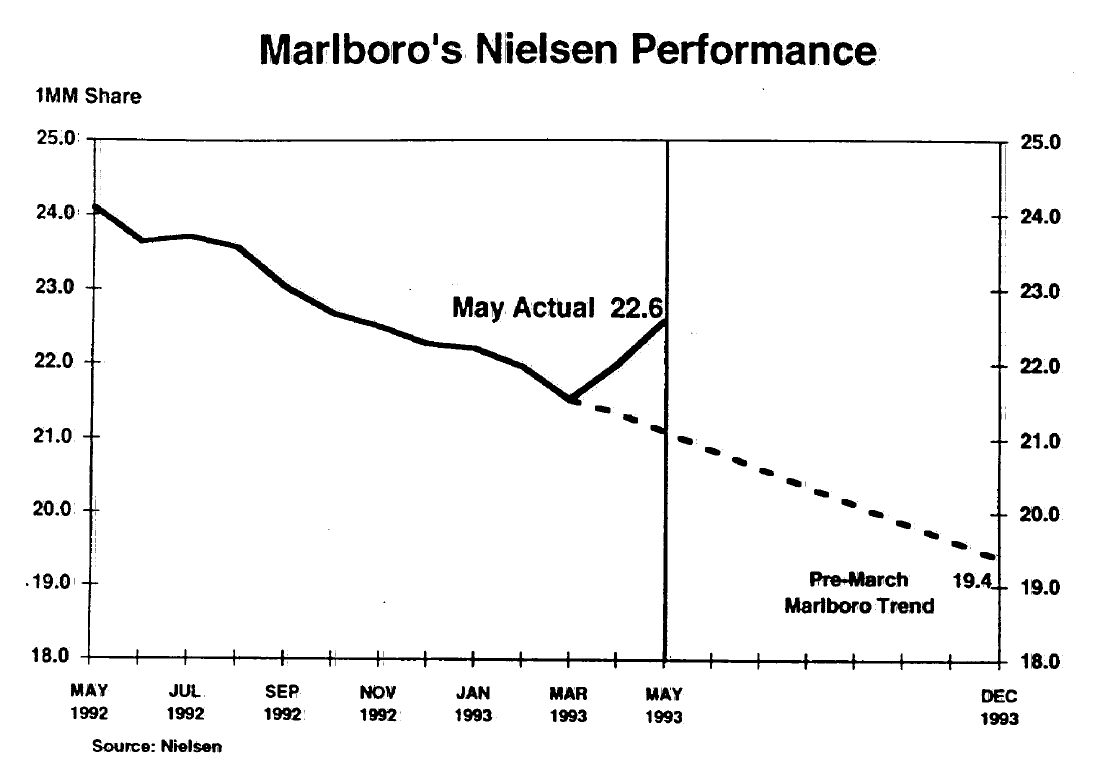

Nearly 33 years ago, on the Friday morning of April 2, 1993, Philip Morris USA, the U.S. tobacco division of Philip Morris Companies Inc., announced it would slash the prices of its premium brand Marlboro by almost 20%. The announcement was a shock given that Philip Morris had regularly increased the per-pack price of its premium Marlboro brand. However, the price gap between Marlboro and deep discount brands had continued to widen. Although Marlboro continued to gain share in the premium category, it was losing overall share. Since 1982, deep discount and generic brand total share had increased from just 1% to about 36%. This, coupled with economic weakness in 1992-1993, meant that by the end of March 1993, Marlboro’s overall share had experienced six consecutive month-to-month declines, falling from a 24.3% share in the prior year to a 22.2% overall share.1

In the morning press release,2 William I. Campbell, President and CEO of Philip Morris USA said:

“We have determined that in the current market environment caused by prolonged economic softness and depressed consumer confidence, we should take those steps necessary to grow our market share rather than pursue rapid income growth rates which might erode our leading marketplace, position.”

Furthermore:

“As part of its shift in strategy to grow market share and longer term profits and cash, flow, the company will take four key actions. First, the company will execute an extensive promotional program which, over the next several weeks, will reduce the average price of Marlboro to a level which has proven in test market to be effective in encouraging consumers to make brand selections based on brand preferences rather than price. Second, Philip Morris USA will expand the Marlboro Adventure Team, a popular promotion that has increased the visibility of Marlboro and consumer involvement with the brand. Third, the company will intensify its efforts to obtain market share in all industry segments and will take prompt action to expand the distribution of its discount brands. Finally, the Company said it expects to forego any further price increases on premium brands for the foreseeable future.”

According to The New York Times on April 3, 1993,3 officials at Philip Morris couched their plans in terms of promotions rather than price cuts. Adding to the uncertainty was the fact there was no time limit to the promotions which would lower their national retail average price from $2.20 to $1.80 per pack, including excise taxes.

The Build-Up to Marlboro Friday

Roger Enrico, CEO of PepsiCo’s Frito-Lay subsidiary, in May 1993 stated Marlboro’s decision was more monumental than New Coke and would be studied in business schools for “the next century.”4 Harvard Business School indeed published a case study in 1996. It provides a decent summary, but I thought the way it framed Philip Morris’s size and success was excellent:

“Philip Morris was a $61 billion company with a proud legacy and a history of success. Between 1983 and 1993, the company realized a compound average annual growth rate of 16.5% in operating revenues, 16.2% in net earnings, 14.6% in net earnings per share, and 25.3% in total return to stockholders. In 1993, Philip Morris directly employed 173,000 people. When taxes on corporate income, cigarettes, employee wages, and other items were totalled, Philip Morris was the largest taxpayer in the United States and the largest nongovemment tax collector in the United States.”

Thus, prior to 1993, Philip Morris was one of the largest and most important consumer businesses in the U.S., if not the world. However, an array of problems and unique circumstances had been coalescing for a long time. These factors culminated in March of 1993 and seemed to force the hand of PM execs to cut drastically the prices of its premium cigarette brands:

A decade of flexing extreme pricing power. As a Fortune article would soon posit—and even a former Philip Morris executive—perhaps Marlboro raising prices at a rate of 10% for a decade (more than double inflation) had finally become untenable?

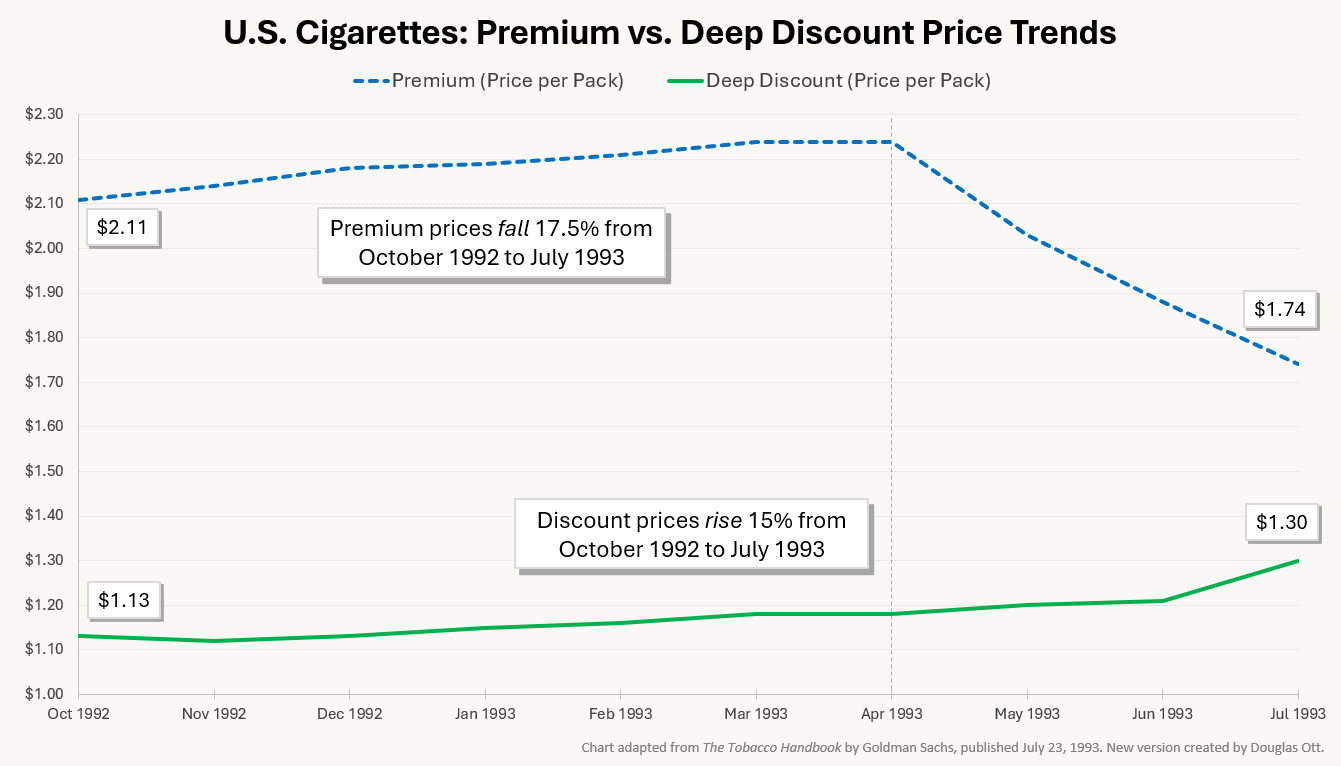

A widening price gap between premium brands and discount brands had caused Marlboro to lose overall market share. Inflation and a poor economy in 1992 and 1993 only fueled continued share gains by the discount brands.

The tobacco industry and its wholesalers had a historical problem of channel stuffing. With regular and large price increases—sometimes multiple in the same year—there was an incentive for wholesalers to purchase excessive inventory in anticipation.

Gene Hoots relates in his ongoing remembrances of the tobacco industry, RJ Reynolds was still in a weak, indebted position, even 4.5 years after KKR’s enormous LBO of the business. Hoots wrote, “The cigarette price cuts meant that RJR, already hampered financially, could not match Philip Morris’ aggressive pricing. This further eroded RJR’s market position.” Furthermore, RJR’s chairman, Louis Gerstner had resigned on March 26, 1993, to become CEO of IBM. If Philip Morris had already been thinking about cutting cigarette prices, perhaps a major competitor with a stressed balance sheet and management turmoil might have been the spoonful of sugar to make the medicine go down?

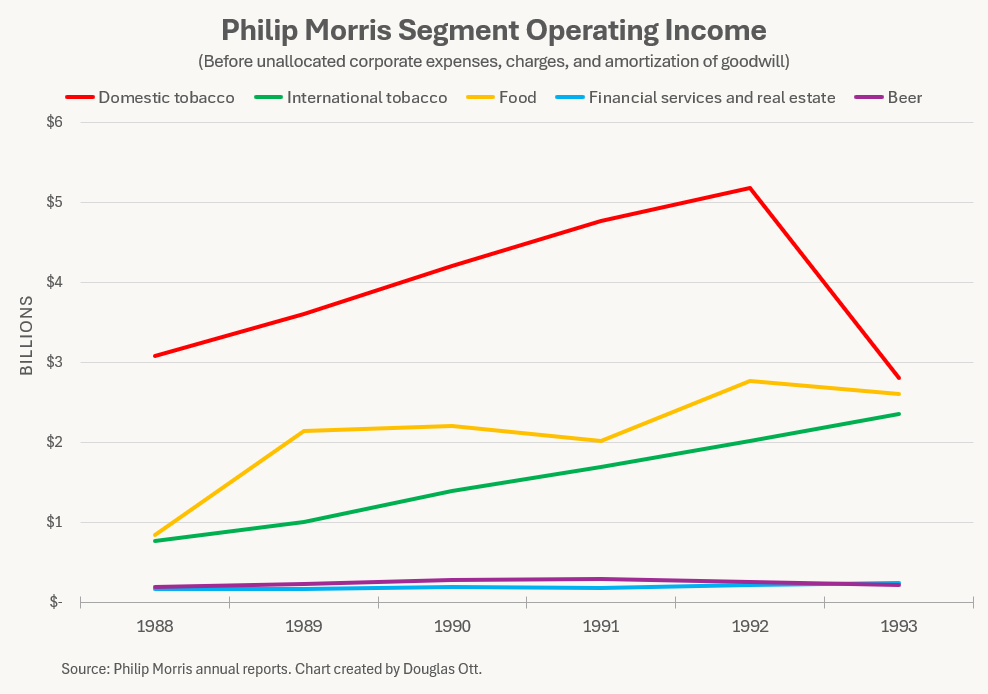

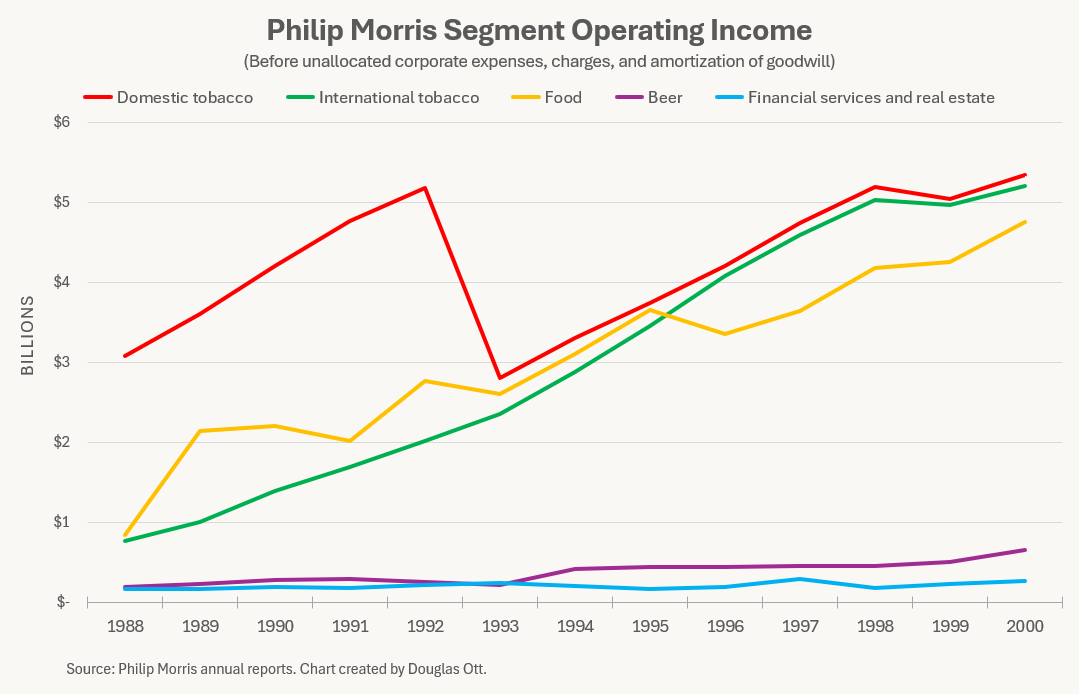

Finally, the U.S. tobacco division of Philip Morris was just one of its four major divisions. It likely was an easier decision to cut prices in one division knowing it could lean on the other four (Food, International Tobacco, Beer, and Financial Services and Real Estate) for support.

Below are probably the charts that likely frightened Philip Morris execs into action.

The Aftermath

The disruption was immediate. The share price of Philip Morris declined 23% on the day of the announcement. In a serious understatement, The New York Times wrote, “The move startled investors, who knocked $14.75 off the price of Philip Morris shares, to $49.375.” This knocked off $13.4 billion of PM’s market cap and was the largest one-day decline in a single stock since October 19, 1987. Sell-side analysts forecasted that PM’s U.S. tobacco operating profits would be down by $2 billion in 1993, a reduction of 40% from the prior year.

The share prices of all other tobacco companies declined by similar degrees as well. Even the share prices of other non-tobacco consumer product companies declined because investors worried that any well-regarded brand might not be worth as much as previously thought. The share prices of Procter & Gamble, H.J. Heinz, Quaker Oats, and Colgate-Palmolive swooned in sympathy.

Three weeks after what everyone now referred to as “Marlboro Friday”, the R. J. Reynolds Tobacco Company announced it also would cut the prices of its leading premium brands, Winston and Camel, in a comparable manner “for at least one month.”

By July 1993, the stock price of Philip Morris had fallen 50% from its 52-week high. It now had a P/E of 8.6x and a 5.5% dividend yield. In exchange for this extreme punishment by shareholders, the price gap between premium and discount cigarettes did narrow substantially. The gap was now $0.64 per pack as opposed to $1.00 per pack. Marlboro was beginning to take back share of the total market. Wholesalers were reporting an “average 25%-30% increase in Marlboro sales velocity, which equated to a 4-percentage point positive swing in market share.”5

Was It Worth It?

According to projections for pricing and profitability for the tobacco industry by Goldman Sachs in July 1993 (emphasis mine):6

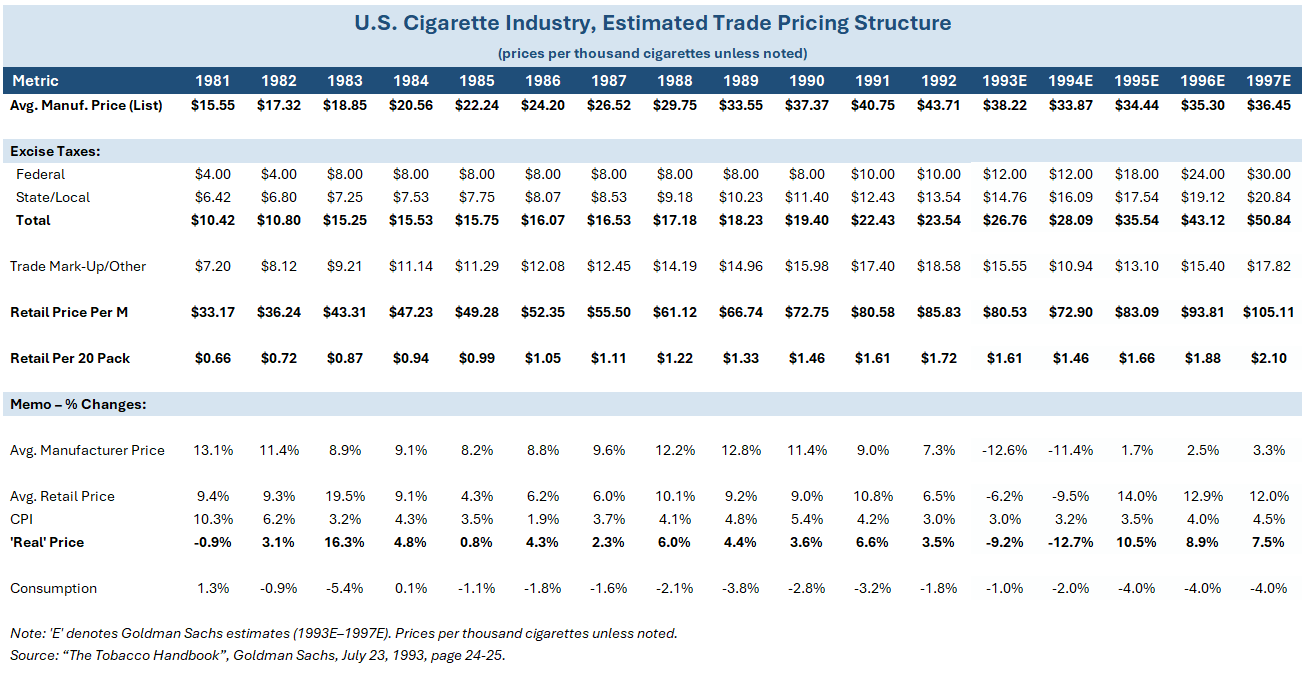

“Not surprisingly, we expect a sharp decline in net pricing and profit margins during 1993 and 1994. Manufacturer net prices could decline 20-25% over the two year period due to the permanent reduction of the premium brands and downward price point repositioning of mid-priced brands. We do not expect employment reductions and decreases in marketing spending to match the unit revenue declines. The net result is that the industrywide operating profit margin appears set to decline by nearly 11 percentage points to 32%. By our estimation, this rolls back the unit profit margin to about the $11-per-thousand (22¢ per pack) level that prevailed in 1987 and the percentage profit margin is now down to the level prevailing in 1984.”

Setting back industry profit margins back nine full years was the estimated effect! It’s only natural to ask if Marlboro Friday was worth it.

Goldman Sachs sounded sympathetic to PM’s decision (emphasis mine):7

“[O]ur belief is that it is incorrect to merely measure the incremental contribution that the Marlboro share gains are generating in a one-year timeframe vis à vis the profit decline that will be reported by the U.S. subsidiary this year. Marlboro was declining at a double-digit rate and Philip Morris was running into the limits of pricing flexibility before it launched this effort. A more accurate view is to compare the rapidly declining cash flows that would have been generated if no action was taken with those that can now be anticipated. Although there is some early dilution, the effort could be additive within three or four years if Marlboro’s share recovery can be sustained and it should produce a positive long-term effect on company value.”

Morgan Stanley’s Howard W. Penney would also post on October 8, 1993, an update (“Where I Stand”) supportive of the long-needed change on pricing in the tobacco industry:8

“As I have said before, the tobacco companies, like other consumer product companies, must correct the excess pricing, of the 1980’s. A new pricing strategy makes sense, given a new competitor: the value conscious consumer. The trend by consumer product companies to go to the value pricing strategy was started by PepsiCo, when it restructured its Frito-Lay division. The company then took this strategy to its Taco Bell division, which touched off a wave of menu changes in the fast food industry. The list of consumer product companies restructuring their business is growing rapidly: Procter & Gamble, Tambrands, Grand Metropolitan and Anheuser-Busch. For tobacco companies—Philip Morris, RJR Nabisco and American Brands—restructuring will not come as soon as investors would like. Basically, any restructuring moves that enhance shareholder value will not occur until the Clinton Administration announces its plans for excise taxes.

Given the fact that every major consumer product company is restructuring their business, why should tobacco companies be any different?”

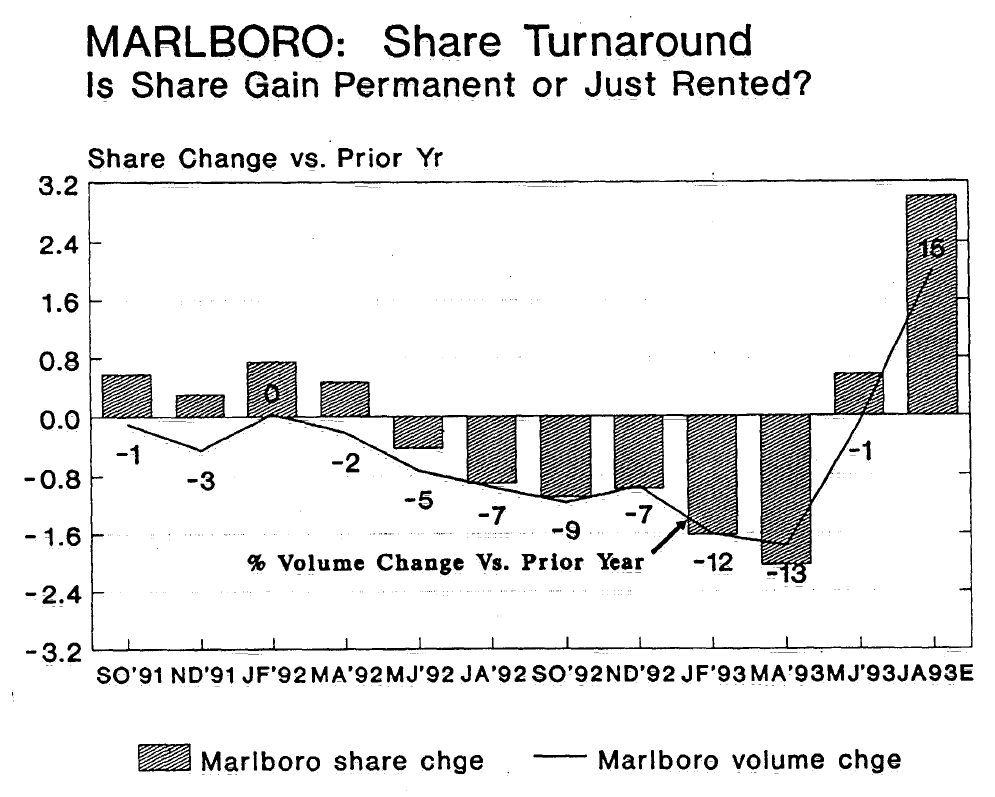

Somewhat less charitable was the tone from Bernstein Research in September 1993: would Marlboro’s share gains post April 2 be permanent or just rented?9 But to be fair, the evidence of the impact of Marlboro Friday was still just coming in…

Summary

When Philip Morris published its 1993 annual report in early 1994, management restated its rationale behind the repricing of its brands:

“Our new pricing strategy and actions had a simple objective: to narrow the price gap between our premium product and discount competitors to a point where consumers would once again base their purchases on brand quality, imagery, and preference, rather than on price alone. Our goal was to recover our lost premium brand share, and thereby to protect the long-term profit and cash-generating power of these strong brands.”

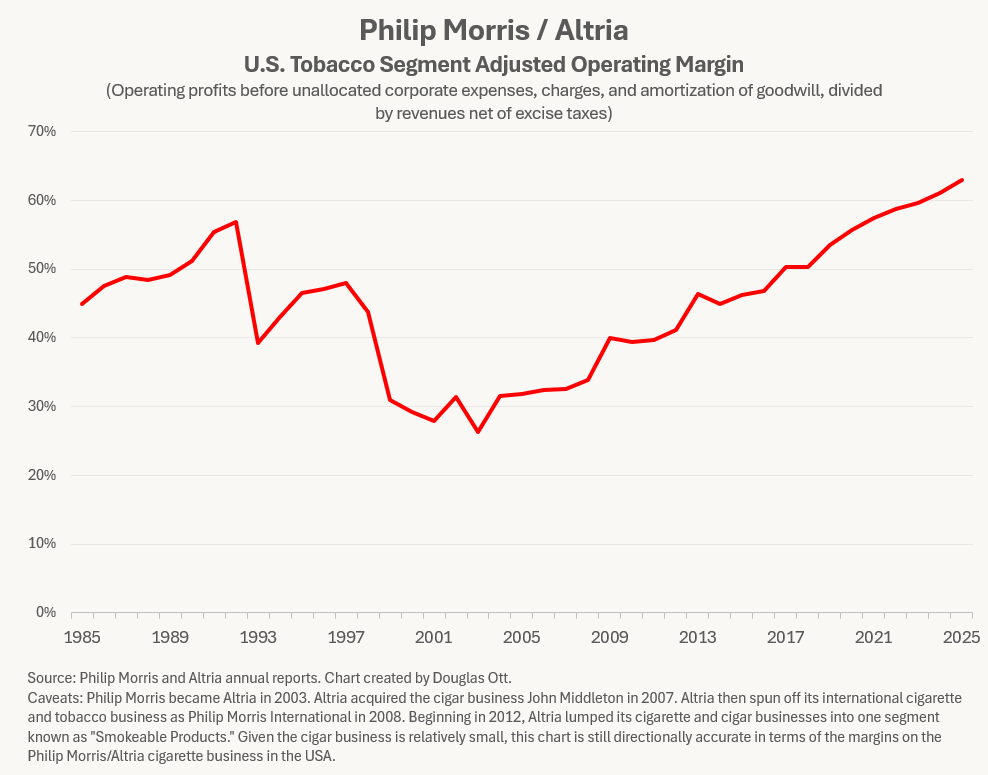

From the book Ashes to Ashes, author Richard Kluger shared that PM’s former chief executive in Europe, Ronald Thompson, had remarked privately, “They just got a bit too greedy, and now they have to pay some of it back.” However, even by 1998, it was still a challenge to answer in the affirmative whether Marlboro Friday was worth it. For Philip Morris, it was six long years before its U.S. tobacco division reached 1992 operating income levels in nominal terms.

On the flip side, operating margins in 1998 were now in the mid-40s, well below the 57% operating margin in 1992. It wasn’t until 2021 that the U.S. smokable products segment of Philip Morris/Altria would equal the operating margins that had been achieved prior to Marlboro Friday.

For the tobacco industry as a whole, it took much longer to reach again its 1992 profit pool in real terms. As veteran tobacco analyst Rae Maile shared on the Preferred Shares podcast (emphasis mine):

“Marlboro Friday came about because a shampoo salesman was put in charge and he saw a declining market. Can I say these things on your podcast? Too late now!

Anyway, he saw a declining market share and cut price. If you look at what happened to the profit pool in real terms, it was 15 years before it got back to the level of industry profit that had prevailed before Marlboro Friday. That to me was a huge failure on part of the U.S. industry.”

Additionally, one of the benefits for PM was a “punishing blow to RJR for having plunged so deeply into discounting.”10 With its debt load, RJR was paying nine cents for every dollar of sales while PM only was paying 3 cents. RJR only avoided bankruptcy due to an additional equity infusion from KKR.

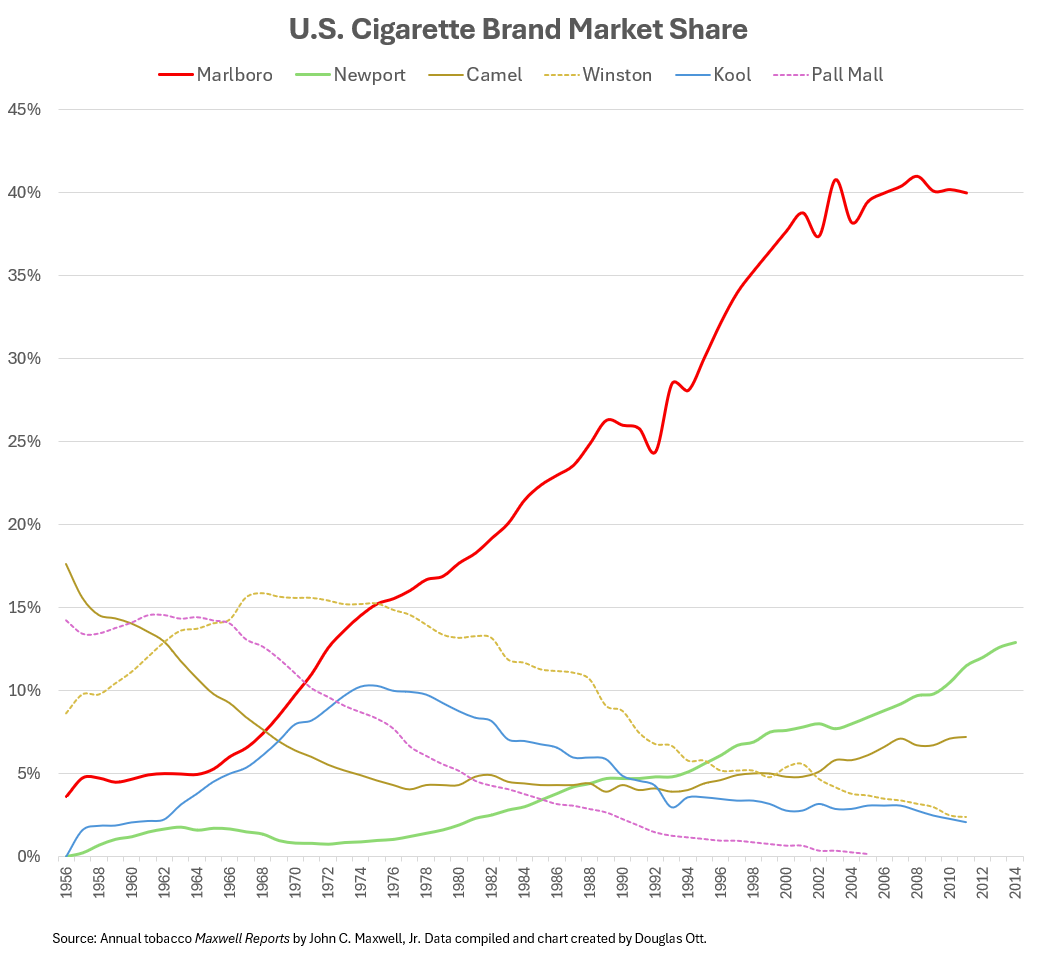

Over the long haul though, Marlboro’s total share of the U.S. cigarette market shot up into the low 40s over the next 13 years after April 1993. The only other cigarette brand to make decent gains over the same period was Newport. Marlboro remains to this day the dominant premium brand in U.S. cigarettes.

Looking at the operating margins of the domestic cigarette/smokable products business, the margin trough after Marlboro Friday was long and deep. But it eventually fully recovered and now has one of the highest margins of almost any business that produces a physical product for consumers.

Could Philip Morris have achieved the exact same results without initiating chaos on April 2, 1993? I lean towards an uncertain “Yes”.

A company always has multiple options available to it. One option could have been to simply stop raising prices for a period of years and take more patient measures to narrow the price gap between premium and discount cigarette brands. The one thing that for sure did not change after Marlboro Friday was the spending on marketing and advertising. As part of its “promotions” in 1993, Marlboro’s “Adventure Team” activities “temporarily turned Philip Morris into the third largest direct mail company in the United States.”11

With all this in mind, it still is conceivable Marlboro could have reached the same level of market share, the same level of revenues, and the same level of profits as it actually did in 2003, but without the disruption and headache of cutting prices by 20% for an initially uncertain amount of time.

Please Subscribe and Share

Please share if you have found this post interesting and illuminating. Make sure to subscribe so all future posts find their way to your inbox.

Further Reading

See my prior post on cigarette marketing and market share evolution of various brands:

Tobacco Advertising and Marketing from 1913-1994

William Slocum wrote in 1951 about the conundrum of how to sell a certain tobacco-based consumer product:

My friend Gene Hoots remembers “The Dark Age” of R. J. Reynolds under its ownership under KKR and the wave of lawsuits the company faced in the 1990s:

My friend Devin LaSarre has his own take on Marlboro Friday he published in November 2022:

Disclaimers for this Substack

The content of this publication is for entertainment and educational purposes only and should not be considered a recommendation to buy or sell any particular security. The opinions expressed herein are those of Douglas Ott in his personal capacity and are subject to change without notice. Consider the investment objectives, risks, and expenses before investing.

Investment strategies managed by Andvari Associates LLC, Doug’s employer, may have a position in the securities or assets discussed in any of its writings. Doug himself may have a position in the securities or assets discussed in any of his writings. Securities mentioned may not be representative of Andvari’s or Doug’s current or future investments. Andvari or Doug may re-evaluate their holdings in any mentioned securities and may buy, sell or cover certain positions without notice.

Data sources for all charts come from SEC filings, Koyfin, and other publicly available information.

Footnotes

Transcript of April 2, 1993 presentation by W. I. Campbell, President and CEO of Philip Morris, USA. <https://www.industrydocuments.ucsf.edu/docs/ggpf0131/>

April 2, 1993 press release by Philip Morris Companies Inc. <https://www.industrydocuments.ucsf.edu/docs/hnfj0111/>

Myerson, Allen R. “Philip Morris Cuts Cigarette Prices, Stunning Market”, New York Times, April 3, 1993. <https://nyti.ms/4luColr>

Sellers, Patricia. “Fall for Philip Morris”, Fortune, May 3, 1993. <https://bit.ly/3NFE1Aa>

Cohen, Marc. “The Tobacco Handbook”, Goldman Sachs, July 23, 1993, page 14.<https://www.industrydocuments.ucsf.edu/docs/thfj0111/>

Ibid, page 21.

Ibid, page 32.

Penney, Howard W. “Tobacco: Where I Stand”, Morgan Stanley, October 8, 1993. <https://bit.ly/47az9Ke>

Black, Gary. “The Tobacco Industry”, Bernstein Research, September 1993, page 5. <https://www.industrydocuments.ucsf.edu/docs/zgpf0131/>

Kluger, Richard. Ashes to Ashes. New York : Alfred A. Knopf : Distributed by Random House, 1996.

Shapiro, Eben. “Cigarette Maker and Time Aim Ads at Smokers,” Wall Street Journal, December 16, 1993.

Nice write up & interesting to note a consumer products repricing decline started with the 1993 “Marlboro Sunday”. Typically you hear that consumer prices caused by inflation “never go down”, but as this article indicated & per the 10/8/1093 Morgan Stanley’s Howard W. Penny statement below, that while rare, apparently it isn’t a 100% truism;

Per Howard W. Penny / Morgan Stanley in 1993:

“As I have said before, the tobacco companies, like other consumer product companies, must correct the excess pricing, of the 1980’s. A new pricing strategy makes sense, given a new competitor: the value conscious consumer. The trend by consumer product companies to go to the value pricing strategy was started by PepsiCo, when it restructured its Frito-Lay division. The company then took this strategy to its Taco Bell division, which touched off a wave of menu changes in the fast food industry. The list of consumer product companies restructuring their business is growing rapidly: Procter & Gamble, Tambrands, Grand Metropolitan and Anheuser-Busch. “