Tobacco Advertising and Marketing from 1913-1994

Cigarette Brand Decline Curves

William Slocum wrote in 1951 about the conundrum of how to sell a certain tobacco-based consumer product:

“The extraordinary part of this tale is that no matter how you cut it, flavor it, toast it, pack it or glamorize it, it is basically the same product. And always has been.

Another strange factor is that no cigarette is any stronger than its next advertising campaign and nobody in the advertising or cigarette business can predict the success of a campaign. They all know that it costs money … but they all know to their fiscal horror that mere money will not sell cigarettes. One of the Big Three curtailed its ad budget $4,000,000 in the uncertain early 1930’s and the economy cost them $20,000,000.”

“Their Sales Go up in Smoke”, Nation’s Business, June, 1951.

In 1950, the tobacco industry in the U.S. sold more than 393 billion cigarettes. 25 years prior, the industry sold fewer than 100 billion. One factor in this growth was certainly the rapacious consumer demand. The other factor was the not so gentle fueling of this demand with modern advertising and marketing techniques.

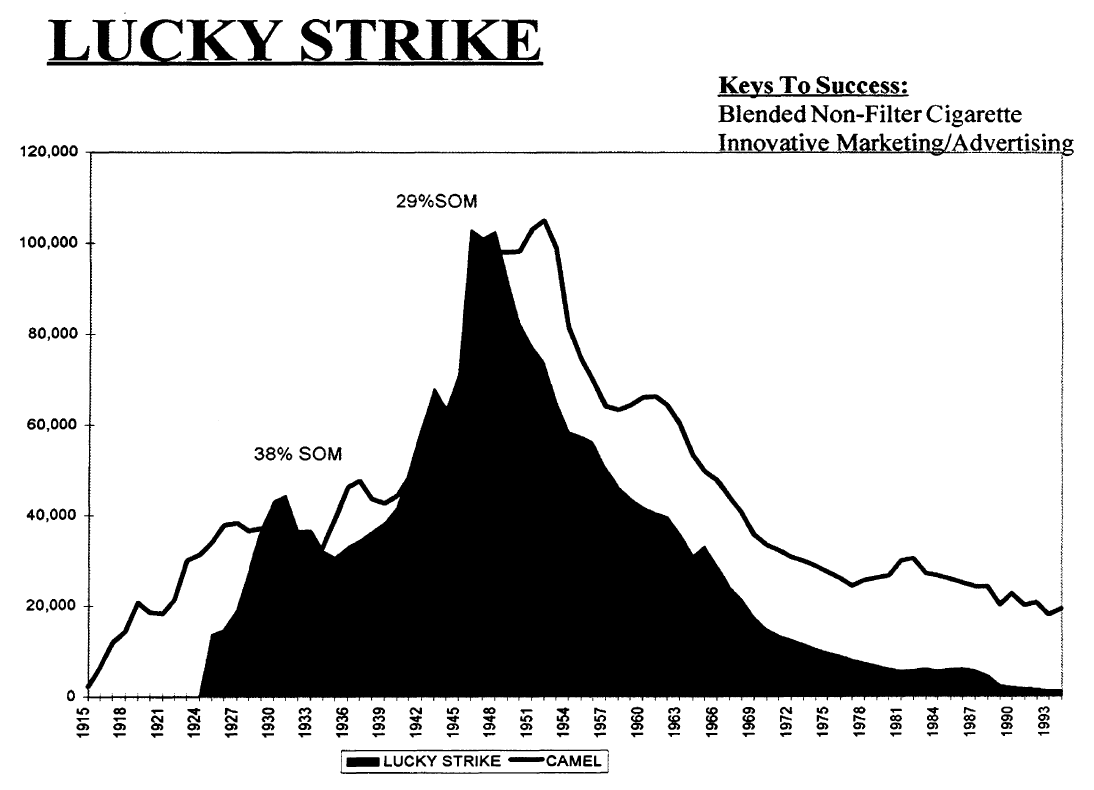

In Slocum’s 1951 article, he also wrote about the battle between Camel and Lucky Strike (from 1925 and 1949), where Lucky was the leading seller for 14 of those years while Camel was leader for the other 11. In that same time, Chesterfield took second place seven times. At the end of the 1940s, Camel was the leading brand (by just one percentage point), Lucky was second, and Chesterfield third. In terms of marketing dollars spent, a conservative guess was that $500 million in total was spent to advertise both Camel and Lucky in a contest that wound up being a stalemate.

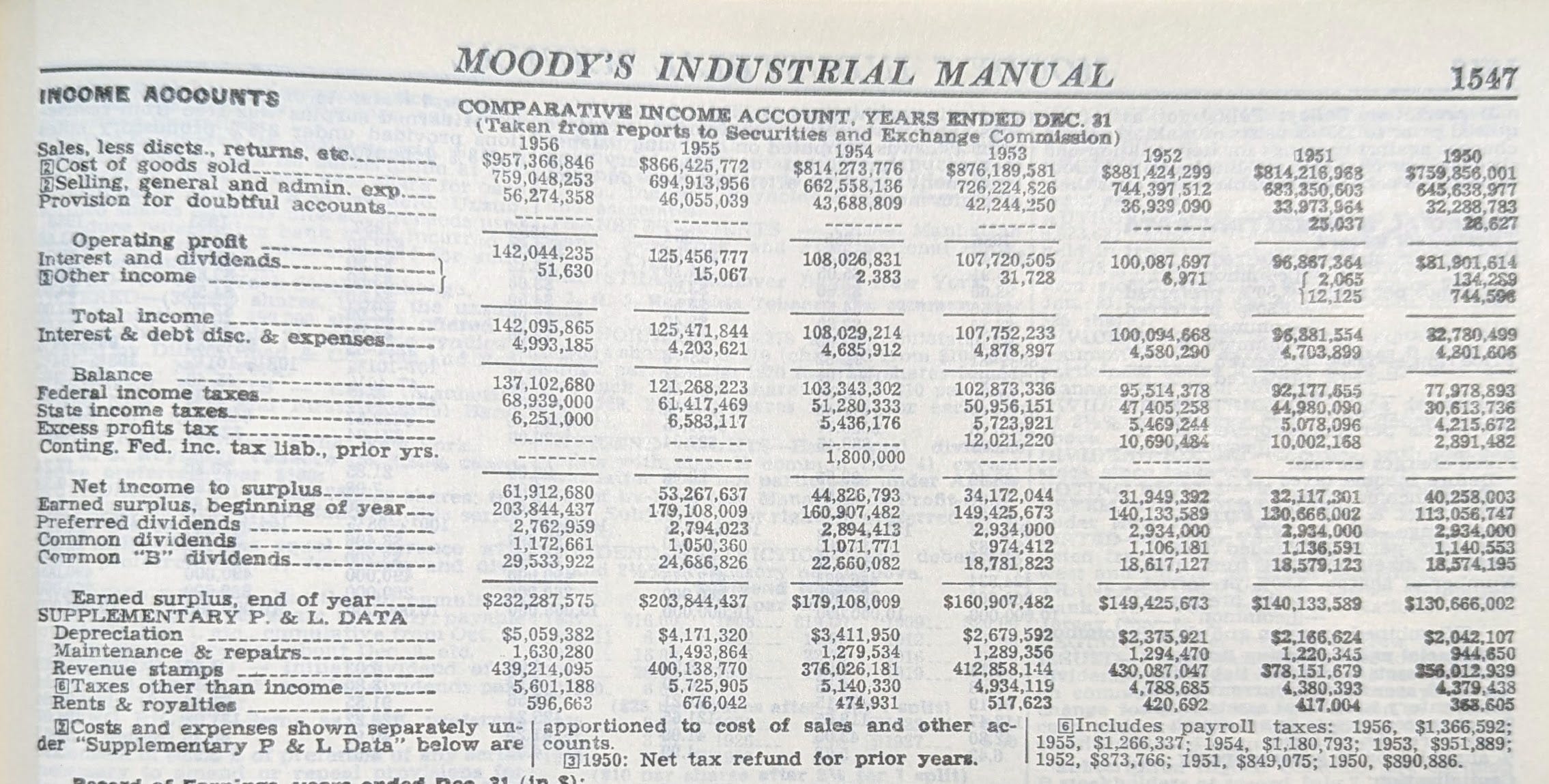

Another interesting point from Slocum’s article is none of the tobacco companies would even hint at the exact sums spent on advertising and marketing. None shared these figures with journalists, nor even their own shareholders. Marketing dollars for the publicly traded tobacco companies were either lumped in with COGS (cost of goods sold) or grouped in with some catch-all operating expense line item. The reason? “Promotion figures are kept under cover because when things go well no firm wants to tell a rival how much it is costing.” See the income statements for R. J. Reynolds (RJR) below for 1950-1956:

Drilling For Dollars and Market Share

In some ways, establishing a new cigarette brand has borne some similarities to drilling for oil. You spend money upfront for market studies and product tests. You pick the sites (or demographics) with the highest likelihood for success. Maybe you invest in some R&D to further differentiate your product. You estimate a range of outcomes and then set a budget that will enable the best return on investment.

However, there is only a finite amount of oil and gas beneath the well head and you’ll eventually extract it all. Likewise with cigarettes, there’s a finite number of smokers at any point in time that can only smoke a finite number of cigarettes every day.

Another trait I think oil wells and cigarette brands have shared is the decline curve or decline rate. The amount of oil or gas one can extract over time generally follows a predictable curve. This is the decline rate. It’s a term that sounds a bit depressing, but it is, nonetheless, realistic. Production spikes after you start extracting and then steadily declines over the life of the well.

A key source to the remainder of this post is a 1996 RJR document describing the history of cigarette brand introductions. It is definitively instructive to the many brands that experienced decline curves and the few that did not. According to this document, only five full price brands achieved “leadership” status in the U.S. since the early 1900s, and those are:

Camel (1915-1929, 1934-1940, and 1949-1959)

Lucky Strike (1930-1933, and 1941-1948)

Pall Mall (1960-1965)

Winston (1966-1974)

Marlboro (1975-present)

After reviewing the multitude of charts of market shares and volumes of various cigarette brands, it was most interesting that so many looked just like the decline curve of an oil well. Yes, the introduction of regulations and a shift in consumer demand eventually contributed to the decline curves of many brands, but not all.

But all else equal, shouldn’t a good brand—with the correct amount of cultivation—be able to maintain its market share and volumes for generations?

But all else is not equal, and from the 1920s through the 1970s many cigarette brands arrived to the scene. A handful of brands became dominant. Some of the dominant brands eventually ceded all or most of their share. Challenger brands emerged, gained share, and then proceeded to lose it. One brand became one of the greatest of all time. And yet one thing remained true: up until the most draconian bans on cigarette advertising were enacted, the tobacco companies never stopped drilling to find that new gusher or to plug a hole in their portfolio.

The Brand Leaders

Camel

Camel is the original cigarette branding success story. Created by R. J. Reynolds, in 1913 Camel was the first cigarette brand to be introduced to the entire country—and with good helpings of advance marketing and teasing. Reynolds positioned Camel as a superior cigarette in terms of quality. The company also priced Camel at 10 cents per pack versus 15 cents for the competitors. In just 12 or 13 years, Camel went from zero market share to 45% of all cigarettes in the late 1920s. Camel did falter in the early 1930s when it faced increased competition from Lucky Strike and others that ramped up their respective advertising. But starting in 1934, 80% of company earnings were used to promote Camel which led to it regaining leadership status.

Then, in the 1950s, volumes peaked and market share shrunk to 27%. Volumes would decline from then on. Amazingly, Camel in 1993 was selling the same volume as it was in 1919. Amazing for it having grown and then shrunk so much? Or amazing that it had held on to as much as it did for so long in the face incredible competition? You decide.

Lucky Strike

Lucky Strike followed a similar pattern as Camel. American Tobacco Company advertised Luckies as better than Camels or Chesterfields because “they’re toasted”. The public then began to see ads that asked them, “You Wouldn’t Eat Raw Meat, Why Smoke Raw Tobacco?”, and the public responded by buying more Luckies. In response to Lucky’s ads, Camel played up that their cigarettes were “made fresh and kept fresh, never parched or toasted”…

Also helpful in boosting demand was the fact that Luckies and several other brands were included in rations for soldiers during WWII. Lucky’s volumes went from 40 million to over 100 million as it vied with Camel for market share leadership.

And yet volumes for Camel and Lucky went on a steady decline after the end of the war. The causes? A combination of smokers looking for something new and increasing concerns regarding safety and health? What about a younger generation ready for newer brands? And what were these new brands that could possibly interest both new smokers and those loyal to Camel or Lucky?

Winston

R.J. Reynolds introduced the Winston brand in 1954 as the first, good tasting cigarette with a filter. The initial slogan was “Winston Tastes Good Like A Cigarette Should”. Winston became the #1 selling cigarette just one year after introduction and it was also one of the first brands to advertise nationally on TV. However, despite solid growth in volumes and market share, Winston eventually followed the same decline curve as its sister brand, Camel.

And then, seemingly out of nowhere, the brand to rule all brands emerged in 1954.

Marlboro

But let’s back up a bit from 1954. Philip Morris first introduced the Marlboro brand in 1923-1924 as a luxury cigarette for women. In 1930, it even incorporated a red “beauty tip” to mask lipstick smears. By 1954, Marlboro was just selling a measly 18 million cigarettes a year. Compare that to the top brand Camel who was selling 81.3 billion sticks a year and had a 22% market share. But in 1954, Philip Morris decided to reposition the Marlboro brand in a few key ways.

First, was a packaging innovation, the flip-top box. Second, and most importantly, was re-positioning Marlboro as a definitively masculine brand. Marlboro started to use cowboys and men with visible tattoos in its ads. And then came many brand line extensions. Marlboro would continually gain market.

The Four-Percenters of 1994

Although its interesting that some of the earliest and most popular brands like Camel, Lucky, and Winston eventually lost share and volumes, what might be more interesting is that by 1994, only four full price brands had a 4% (or greater) market share:

Marlboro - 28.1%

Winston - 5.8%

Newport - 5.1%

Camel - 4.0%

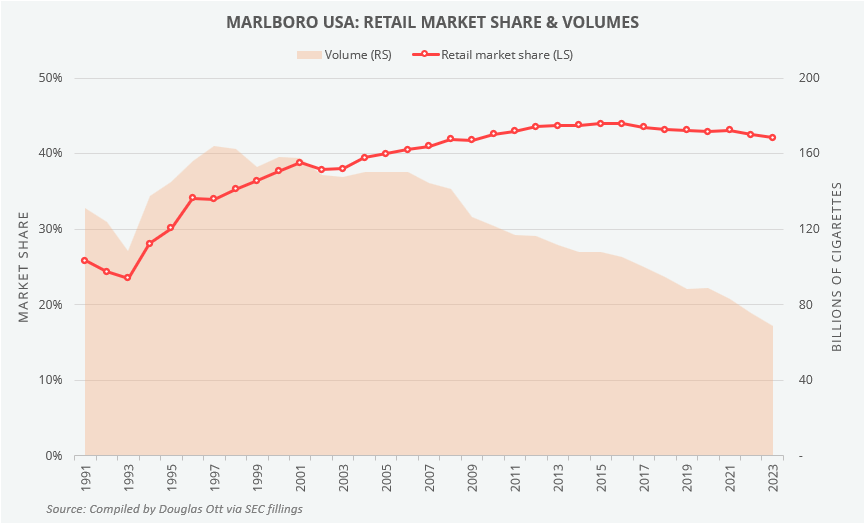

In the chart below, we see the continuation of the volumes and market share of Marlboro from the 1990s to present day. Market share continued to climb from the high 20s up into the 40s, where it still stands today despite steady declines in volume.

Newcomers Struggle to Maintain Market Share

In addition to Marlboro, many brands were launched or relaunched between 1950 and the late 1970s. Some were successful, some not. But for the few that were successful, most wound up giving back all or most of the market share they initially gained. Let’s look at a few examples.

Lorillard Tobacco first introduced Kent in 1952 as a premium brand. Then it added a Micronite filter and it was the first brand to be marketed as a cigarette with the lowest amount of tar. Then in 1957, the Kent brand received an indirect endorsement from Reader’s Digest. This immediately boosted its market share from 1% to over 8%. And then, Kent slowly lost share over the next several decades.

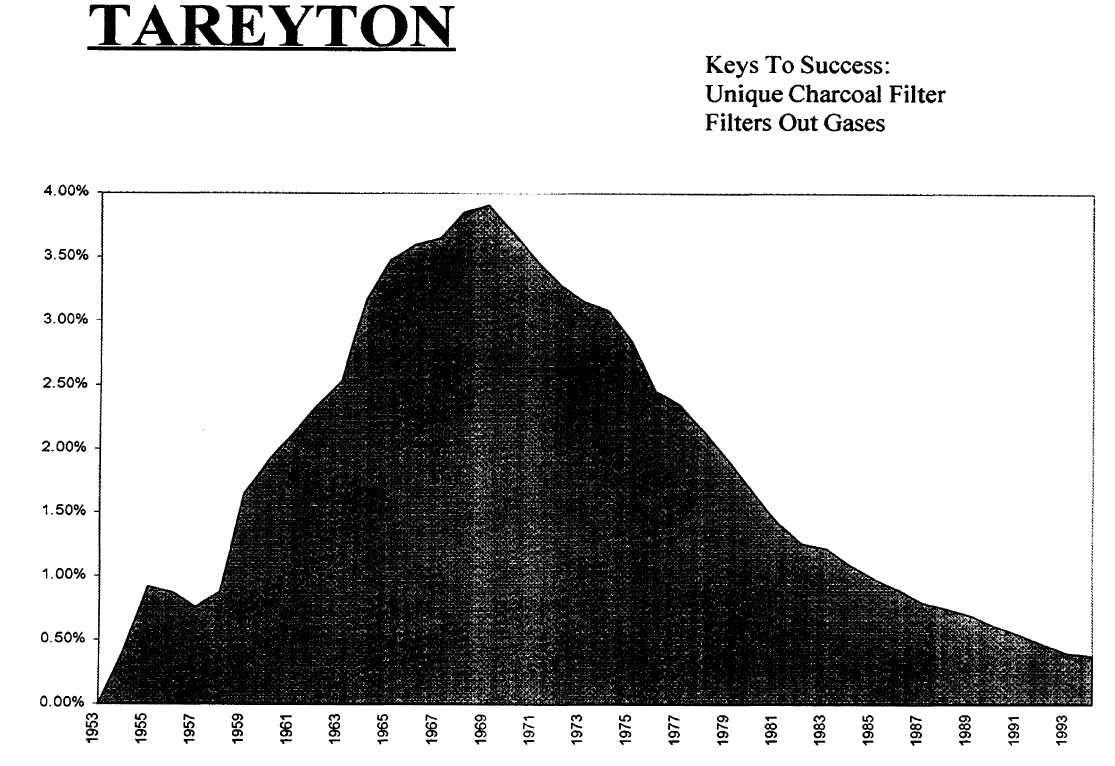

Prior to 1954, Tareyton was an old brand acquired from Tobacco Products Company by American Tobacco Company in 1923. “By mid-1954, American Tobacco was the only major company without an entry in the runaway filter field” (Tareyton Brand History, R. J. Reynolds, 1954) and so American re-introduced Tareyton in 1954 as the first with a charcoal filter. The marketing centered on this technology. Tareyton grew its market share to nearly 4% by 1970 after which the brand continually lost share.

RJR introduced Vantage in 1970 and positioned it with the statement, “Fuller Flavor Low Tar”. Vantage also had a “revolutionary” filter that had six times more surface area than other filters. It’s market share peaked in the early 1980s and then slowly declined.

L&M, a brand introduced by Liggett & Myers is our final example of the cigarette brand decline curve.

Takeaways

Introducing a new brand in any industry is a risky proposition, perhaps even more so in a highly competitive space like cigarettes where brand loyalty has tended to be strong and where the return on marketing dollars is highly uncertain.

Whether you’re in the business of extracting fossil fuels or delivering nicotine via cigarettes, one of the pivotal questions is the degree to which you can extract what might be a finite resource over a certain period of time. With oil and gas, the finite source is the oil and gas under the ground that will eventually be depleted. With cigarettes, what’s being extracted is dollars from the pockets of consumers (a finite resource) who themselves can only smoke a given number of cigarettes in any given day.

There have been many successful (and unsuccessful) attempts to prolong the period of extraction in both oil and in tobacco. Oil and gas companies have developed new technologies and methods like fracking to enhance and boost well productivity. The tobacco companies during 1913 to 1994 have—to varying degrees of success—sustained the life of their cigarette brands with product innovations, line extensions, and renewed ad campaigns.

Needless to say, the extraction business is not an easy one. And that’s before it becomes complicated with concerns for health and safety. Although the decline curves we saw above speak volumes, from the perspective of the tobacco companies, the saving grace has been a consistent ability to raise the prices on their winning cigarette brands to offset decreasing volumes.

Please Subscribe

If you enjoyed this content, please share and subscribe.

Sources and Additional Reading

“Their Sales Go up in Smoke”, Nation’s Business, June, 1951.

“Wanted—And Available—Filter-Tips That Really Filter”, Reader’s Digest, August, 1957.

“History of New Brand Introductions”, R. J. Reynolds, 1996.

Hoots, Gene. “Tobacco Goes to War - World War I”, Reflections on “Going Down Tobacco Road” and Investing, Nov. 11, 2021.

“Brand Histories”, Stanford’s Research into the Impact of Tobacco Advertising.

“Rae Maile: A Lifetime in Tobacco”, Preferred Shares podcast, Sep. 27, 2024.

Disclaimers

The content of this publication is for entertainment and educational purposes only and should not be considered a recommendation to buy or sell any particular security. The opinions expressed herein are those of Douglas Ott in his personal capacity and are subject to change without notice. Consider the investment objectives, risks, and expenses before investing.

Investment strategies managed by Andvari Associates LLC, Doug’s employer, may have a position in the securities or assets discussed in any of its writings. Doug himself may have a position in the securities or assets discussed in any of his writings. Securities mentioned may not be representative of Andvari’s or Doug’s current or future investments. Andvari or Doug may re-evaluate their holdings in any mentioned securities and may buy, sell or cover certain positions without notice.

Data sources for all charts come from SEC filings, Koyfin, and other publicly available information.