The Mastercard logo is by now easily recognizable. It’s two circles. One red, one dark yellow, both overlapping each other in a Venn-like diagram. The meaning behind the logo is to “express the idea of connection, while the basic circular shapes suggest inclusiveness and accessibility, key to Mastercard’s brand message of ‘priceless possibilities.’”

I accept this interpretation, but as a numbers guy and investment analyst, I think there is now an additional interpretation. For me, these two circles also represent the two revenue streams of Mastercard: the revenues from its payment network business and the revenues from its value added services (“VAS”) businesses.

And guess what? These two businesses/circles are—and have been—reinforcing each other for a while. Without one, the other would be less valuable. And furthermore, both businesses/circles are converging closer and closer such that we are seeing more and more of the overlapping red-orange hue.

“It comes back to the virtuous cycle between payments and services. We have to be … relevant in payments. We have to be in the flow so we can apply our Payment Solutions and our Services Solutions.”

—Mastercard CEO, Michael Miebach, Jan. 30, 2025

Mastercard must be in the flows of payments and transactions for its value added services (VAS) to remain valuable and to increase in value. The converse is also true. For its VAS to retain and increase in value, it must be involved in all aspects of payments and transactions with its network. Both reinforce each other. VAS is becoming more important to help sell the payment network services, and the payment services is becoming more and more the appetizer to the incredible selection of entrees of the value added services.

FY2024 Results

Here are the highlights from Mastercard’s FY2024 results it reported last week:

Net revenue growth of 12.2%, comprised of VAS growth of 16.8% and payment network growth of 9.5%

For all of Mastercard’s worldwide credit, charge and debit programs, purchase volume increased 11.4% and number of transactions 11.9%;

EBITDA margins remain high, but declined slightly from 61.1% in 2023 to 60.9% in 2024;

Free cash flow per share increased 27.3% year over year; and

Mastercard returned $13.5 billion to shareholders in the form of dividends and buybacks in 2024. The company currently has a $508 billion market cap.

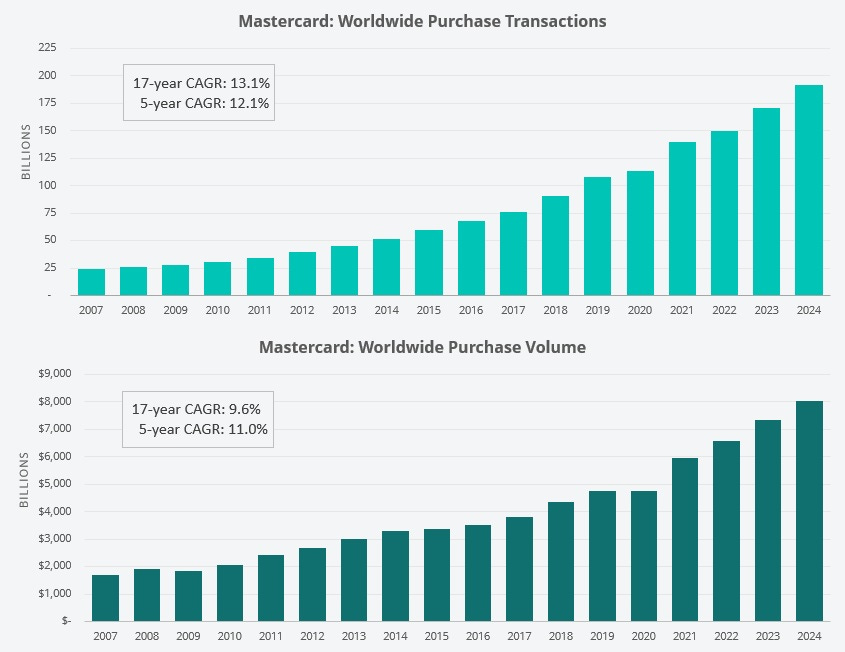

Purchase Volumes and Transactions

The long term trend in growth of purchase transactions and purchase volumes (measured in dollars) remains in place. Purchase transactions in 2024 grew 12.2% over the prior year, very close to the 17-year CAGR of 13.1% annualized. Purchase volumes grew in 2024 grew 9.2% over the prior year, very close to the 17-year CAGR of 9.6% annualized.

However, it might be important to note that the 5-year annualized growth rate of purchase volumes has come out to 11%. Is this acceleration noteworthy or not? Faster growth is typically a good sign in most things, but what are the reasons? We think it likely comes down to a mixture of higher inflation increasing the prices of goods and services. We also think it is more people using Mastercard’s services for more purchases and more transactions.

Expense Categories

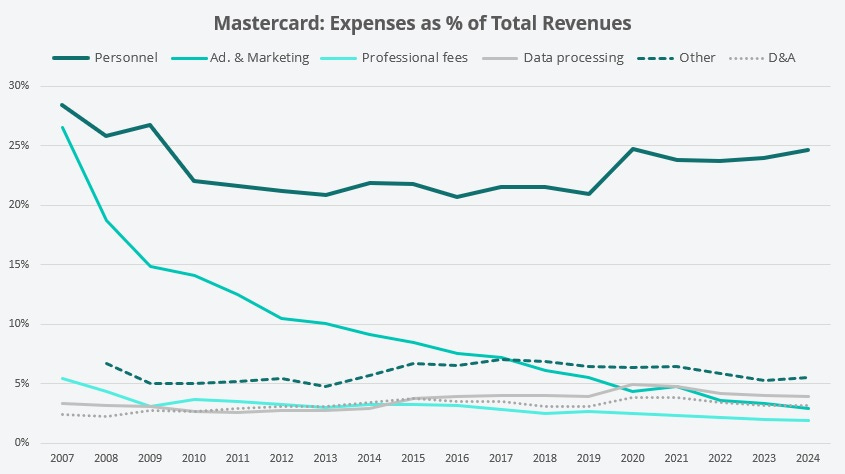

Let’s now look at the major expense categories as a percent of total revenues.

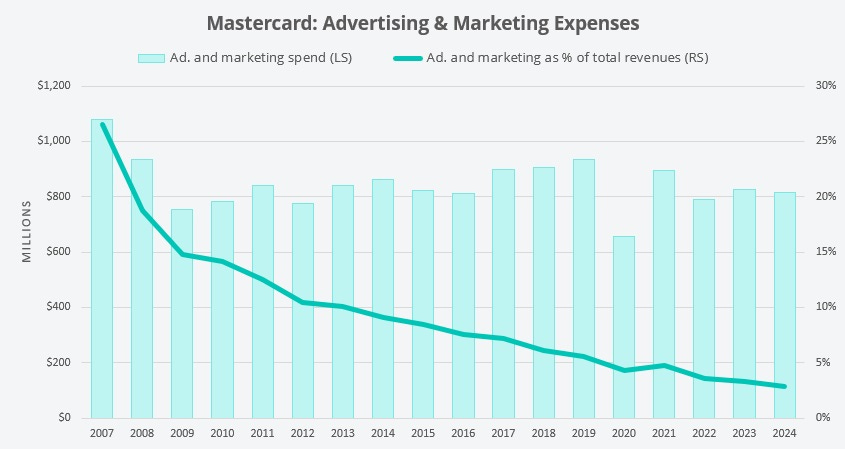

You can see that advertising and marketing remains the one category that has benefited the most from Mastercard’s growing scale. This category has remained fairly static in terms of dollars spent as Mastercard has grown over the years. Professional fees as a percent of revenues has also declined somewhat.

Yet, the spend on personnel seems to have not benefited from Mastercard’s growth. But this should not necessarily disappoint a shareholder. I think there are a few things going on here. First, investment in people has generally been a large driver of growth in the first place. Second, growth in personnel expenses—roughly in line with revenue growth—is also a function of Mastercard’s increasing emphasis on value added services to sell alongside its core payment network business. As most of the value added businesses Mastercard has acquired (or grown internally) are similar to niche consulting businesses, they naturally require more humans for their expertise and judgment.

Yields and Ratios

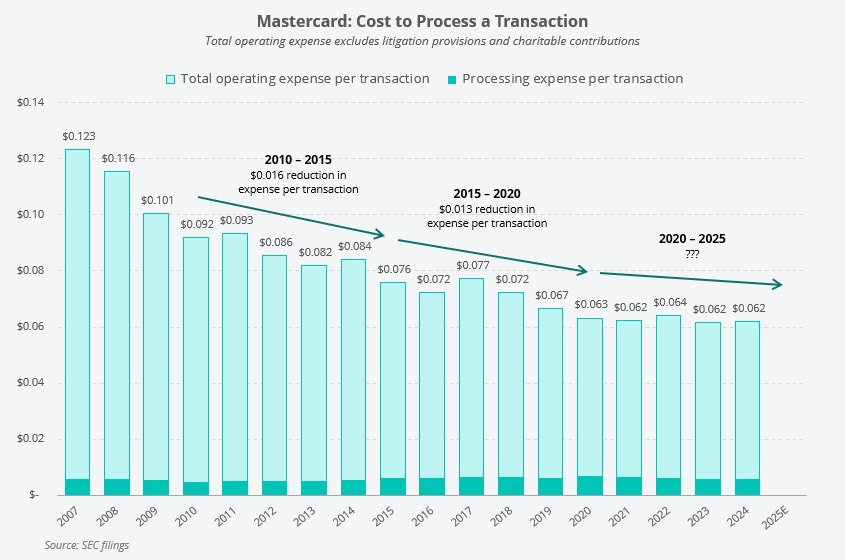

Now, on to the costs to process a transaction. Since 2007, Mastercard has lowered costs on a per transaction basis. However, it is a bit disappointing to see barely any improvement from 2020 to 2024. I suspect the reason for this has to do with VAS, which has greater costs and lower margins, attaining greater importance to the overall business.

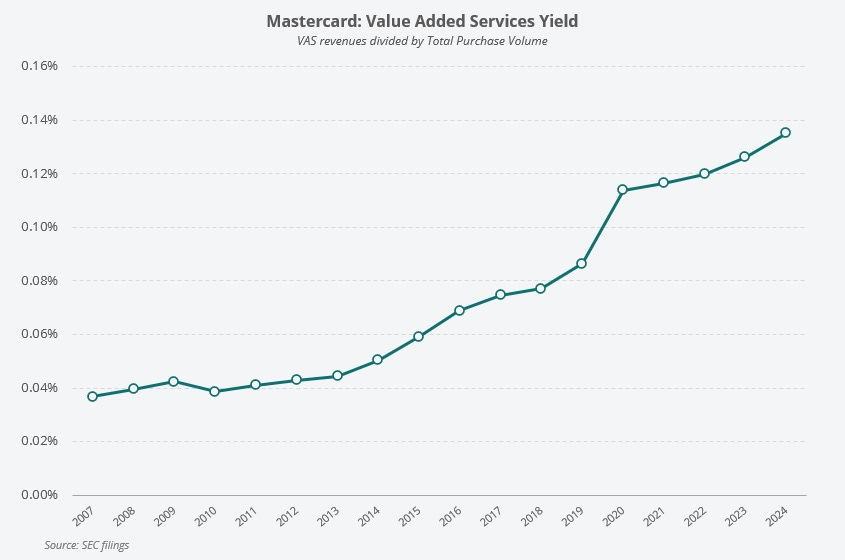

Another interesting metric I’ve started to follow is the value added service yield. You simply take the revenues from value added services and divide it by total purchase volume. The metric simply shows how much VAS revenues Mastercard achieves relative to the purchase volumes that flow through its network.

As you can see, the yield has steadily increased over the years. The obvious conclusion is that VAS revenues have increased at a faster rate than purchase volumes. There are two reasons for this.

Inorganic. Mastercard has increased the VAS component of its revenues with acquisitions.

Organic. More customers find the VAS to be increasingly valuable. Customers can use a variety of Mastercard’s services to optimize over a dozen different aspects of their credit/debit card businesses or just assist in effectively transferring value to their constituents.

Mastercard's Overlooked Metrics

With this post, I discuss what I think are some overlooked metrics that are the result of Mastercard’s scaled payment network.

Emphasizing Value Added Services

Putting an emphasis on VAS makes sense for Mastercard. The payment network business has faced near constant pressure from governments, regulators, and retailers. These groups have continuously complained that the fees the payment networks charge are too high. And yet there is nary a mention or acknowledgment from these antagonists of the enormous value (direct and indirect) the payment networks provide to everyone. Thus, Mastercard for nearly two decades has grown and maximized its network given the aggressive regulatory pressure while at the same time investing heavily in VAS—businesses and revenue streams that do not have the same regulatory pressure and scrutiny. VAS revenues will eventually eclipse revenues from Mastercard’s payment network.

But in addition to the benefit of revenue streams with little or no regulatory pressures, VAS also serves to increase the value of Mastercard’s network. It increases the likelihood a financial institution will choose to work with Mastercard and it increases the length quality of customer relationships.

During its investor day in November 2024, Mastercard put some numbers out on how customers have increasingly embraced its VAS. For example, from just 2021 to 2023, Mastercard customers have gone from an average of three services utilized per transaction to five services utilized per transaction. With newer and more helpful services being rolled out or acquired, and with increasing understanding of the value proposition by customers, it seems assured Mastercard will increase this figure over time.

Opportunity Remains Enormous

To sum things up, Mastercard continues to execute. With their payments network, they have adapted and evolved in continuously challenging regulatory and legal environments across the world. And despite their historical success in displacing cash and introducing new ways to transfer value, the opportunities to grow and grab market share remain enormous.

In the U.S. alone, there is $1 trillion in cash and 27% of all transaction in the U.S. are still done with cash;

Invoice payments is a $63 trillion market and only $2 trillion of that is carded right now; and

With its current suite of value added services, Mastercard claims the total addressable market (TAM) is $165 billion. Revenues from Mastercard’s VAS in 2024 were $10.8 billion, which means it has a 6.5% market share. Even if the true TAM for VAS is half the size of its claim, it’s still an large opportunity.

The growth algorithm of attacking multiple fronts within the payments space has been outstanding. Thus far, exceptional financial and business results have translated into exceptional shareholder results. As friend and colleague Lawrence Hamtil of Fortune Financial recently pointed out, shares of Mastercard since its IPO on May 25, 2006, has kept up with or exceeded the returns of the likes of Apple and Amazon in the same period.

In the end, it seems Mastercard is an underappreciated business and brand. It saves everyone time and money, but most can’t help but complain about it. It benefits from network effects, but its not Facebook or Instagram. Everyone knows the brand, but no one knows the name of its CEOs. It’s tech, but it’s not in Silicon Valley, it’s in Purchase, NY. To paraphrase one of its famous slogans, although it likely can never buy the respect and admiration it deserves, for everything else there will always be Mastercard.

Please Subscribe

If you enjoyed this content, please share and subscribe.

Other Recent Writing

Victor Emanuel

This is the story Victor Emanuel, a dealmaker and financier who made a fortune in the utilities industry when he sold out to the infamous Samuel Insull in 1926. A few years later, just before the Great Depression began, Emanuel would make an even bigger go at consolidating the utility industr…

Q4 2024 Andvari Letter

Andvari Associates has allowed us to share an excerpt of its Q4 2024 letter. Please enjoy.

Disclaimers

The content of this publication is for entertainment and educational purposes only and should not be considered a recommendation to buy or sell any particular security. The opinions expressed herein are those of Douglas Ott in his personal capacity and are subject to change without notice. Consider the investment objectives, risks, and expenses before investing.

Investment strategies managed by Andvari Associates LLC, Doug’s employer, may have a position in the securities or assets discussed in any of its writings. Doug himself may have a position in the securities or assets discussed in any of his writings. Securities mentioned may not be representative of Andvari’s or Doug’s current or future investments. Andvari or Doug may re-evaluate their holdings in any mentioned securities and may buy, sell or cover certain positions without notice.

Data sources for all charts come from SEC filings, Koyfin, and other publicly available information.

Visa and Mastercard have nearly identical business models, the visa stock has not been performing as well, would be interesting to see a comparison. Also from an ROE standpoint Mastercard always beats Visa due to leverage. Why doesn’t Visa follow the same playbook?