Victor Emanuel

Part 1: From Gilded Age Dealmaker to Turnaround Artist

This is the story Victor Emanuel, a dealmaker and financier who made a fortune in the utilities industry when he sold out to the infamous Samuel Insull in 1926. A few years later, just before the Great Depression began, Emanuel would make an even bigger go at consolidating the utility industry in America. Then, in 1937, Emanuel would gain control of Cord Corporation, on the seeming verge of collapse, from a motivated seller. Emanuel fixed Cord up with a healthy dose of restructuring and financial engineering and then renamed it after one of its major holdings: Aviation Corporation (AVCO). During World War II, AVCO would become an important provider of military and naval aircraft, airplane engines, propellers and parts, and naval vessels. After WWII, Aviation Corporation would divest one of its most significant subsidiaries, Convair, and then embark upon the path of diversification and conglomeration.

Victor’s Early Years

Victor Emanuel was born in Dayton, Ohio, in 1898. He was the son of Albert Emanuel, a wealthy utilities investor and executive. Coincidentally, Victor also grew up just two doors down from scientist, engineer, and businessman, Charles F. Kettering. Kettering would become the founder of Delco, later acquired by General Motors, whereupon Kettering would lead GM’s research and development from 1920 to 1947.

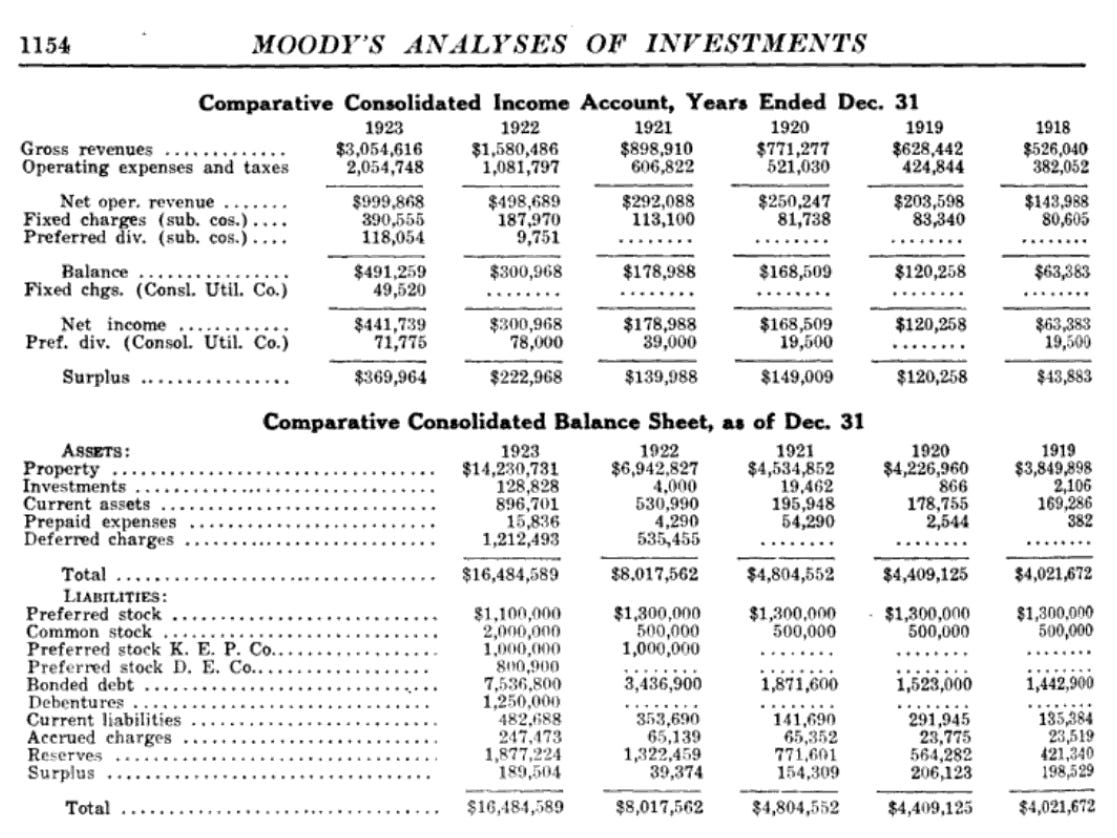

Later in his life, Victor would become a naval aviator for the U.S. during World War I. After the war, when Albert Emanuel came to be in poor health, Victor went to work at his dad’s utility business. Operating from New York, Victor helped acquire, grow, and manage numerous utilities. By 1923, the main holding company of Albert Emanuel was The Consolidated Utilities Company with assets in Kansas, Indiana, Ohio, Pennsylvania. Consolidated served 66 towns and cities with a cumulative population of 220,000 in its areas of operation. Below is a chart showing Consolidated’s financials from 1918-1923.

In 1925, Victor would buy out his dad’s business interests. He had grand plans.

National Electric Power Co.

To buy out his father, Victor got together with Chicago banker Arthur Cecil Allyn. The two of them incorporated the National Electric Power Co. (NEPCO) on March 3, 1925. They pooled $750,000 of their own capital and raised another $5 million by issuing shares to the public.

NEPCO expanded rapidly and would soon control 14 utilities across the nation. For 1925, its first full year of operations, NEPCO reported gross earnings of $15.64 million and total assets of $95.9 million. It now served over 400 communities with a total population of 1.125 million. After competing against each other to buy various utilities, Samuel Insull himself would buy out the personal interests of Emanuel and Allyn in 1926 for about $13 million ($230 million in 2024 money). Emanuel was now a multi-millionaire at the age of 28.

After the sale of his interest in NEPCO, Emanuel would leave the U.S. to live in England among the upper crust of society. He also began to play in the stock market and would amass a paper wealth of $40 million by 1928 at the age of 30.

Another Go At Utilities

Although Emanuel lived a life a leisure for several years, it was unsatisfying. With his wealth he wanted and needed a grander business adventure. He wanted to take over “just about all the utilities in the U.S.” With this monumental goal in mind, Victor went to London banker J. Henry Schroder & Co. and to old friend Arthur Cecil Allyn. Amazingly, the outline of the plan was written down in a memo on May 13, 1928 and G.F. Beal of the Schroder Trust Company had written at the top, “Not to be taken too seriously.”

Regardless of the audacity of the plan, the bankers helped Emanuel raise $60 million. Emanuel formed the U.S. Electric Power Corporation (USEPCO) in 1929 as a holding company for the utilities he’d soon acquire.

The first acquisition target was Standard Gas & Electric Power Corp. However, two groups controlled the business: H. M. Byllesby & Co. and Ladenburg, Thalmann & Co. Emanuel purchased the Ladenburg interests for $25 million: $10 million in cash and $15 million in notes. For the $15 million in notes, USEPCO had to pledge as collateral virtually all the Standard Gas stock it acquired.

The New York Times reported on speculation in the shares of Standard Gas on September 28, 1929:

“An advance of 40 points in three days in the price of Standard Gas and Electric Company common stock on the New York Stock Exchange in a generally weak market brought in its wake yesterday rumors of a battle between powerful groups for control of the company. The stock opened at 219 yesterday…; soared to 243¾, the highest level in its history, and closed at 235½, up 16½ points…. The low point this year was 80¾.

The Standard Gas and Electric Company is one of the few billion-dollar utilities in this country. Since its organization in 1910 it has been controlled by H. M. Byllesby & Co. of Chicago, who owns all of the 1,000,000 shares of $1 par 6 per cent preferred stock, which is a voting stock. There are also 1,560,841 no-par common shares, also with voting rights. Utility and Industrials, an investment trust organized and controlled by the Byllesby group last Spring, is believed to own sufficient Standard Gas common stock to prevent control from passing into other hands without the consent of Byllesby & Co.”

Further along in the same article, we see the extent to which Byllesby had control over Standard Gas:

“Byllesby & Co. is tightly controlled by the directors, who are reported to have undertaken some years ago an agreement whereby no director can dispose of his holdings except to other members of the board, thereby assuring permanence of control to the ownership.”

Needless to say, Byllesby & Co. would do their best to hold out against a determined Emanuel, but they ultimately lost to Emanuel who chose to wage a campaign where he “forced Byllesby to capitulate by filing a list of charges of misappropriation of funds, mismanagement, etc.” However, Emanuel did give a consolation prize to Byllesby. USEPCO would control 75 per cent of Standard Gas’ future security floatations and Byllesby would get 25 per cent.

On December 27, 1929, the New York Times reported on the shift in power from Byllesby to a new group:

“Participation in the control of the $1,000,000,000 Standard Gas and Electric System, hitherto held by … Byllesby & Co. alone, will be shared by the latter with the United States Electric Power Corporation, controlled by the Harris-Forbes Corporation and a large international banking group, upon consummation of a reorganization plan announced yesterday.

The new group, which has won its way to a dominant financial position at the head of the Standard System through the acquisition of large blocks of common shares in Standard Gas and Electric, will be the principal interest represented on the board of the Standard Power and Light Company, which is to become a holding company of the entire Standard System.”

With Byllesby and Ladenburg taken care of, Emanuel finally had what he wanted. Control of a utility with a presence in 20 states and with over $1 billion of assets. At the end of 1930, Standard Gas would grow to $1.2 billion of assets with $19.49 million of earnings.

Stock Market Crash and Great Depression

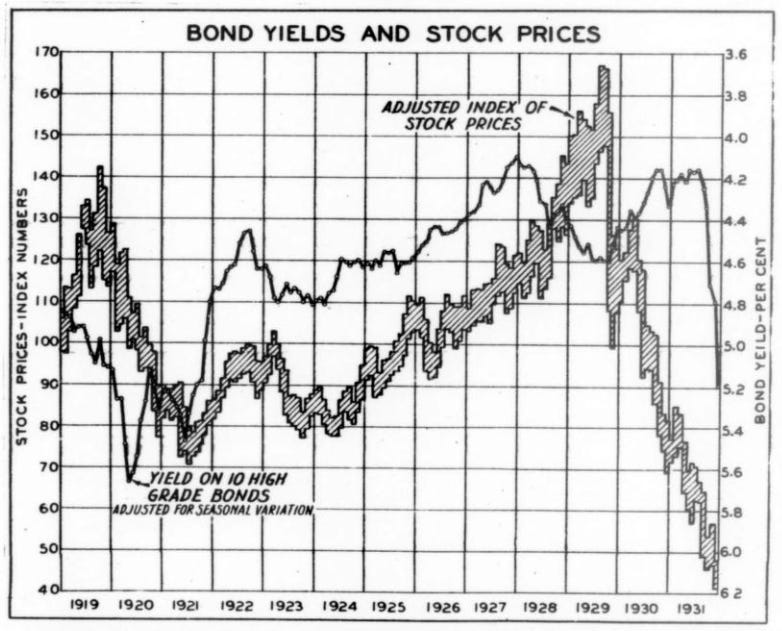

But Emanuel’s victory would eventually transform into the Pyrrhic variety. The timing was unfortunate—he bought, with leverage, and then expanded an enormous asset at peak prices. Standard Gas earnings fell from $19.49 million in 1930, to $15.4 million in 1931, and then to $7.656 million in 1932. With the Great Depression unfolding, the stock market declined quickly over two years and would be stuck in a rut until the beginning of World War II. Emanuel’s personal fortune evaporated.

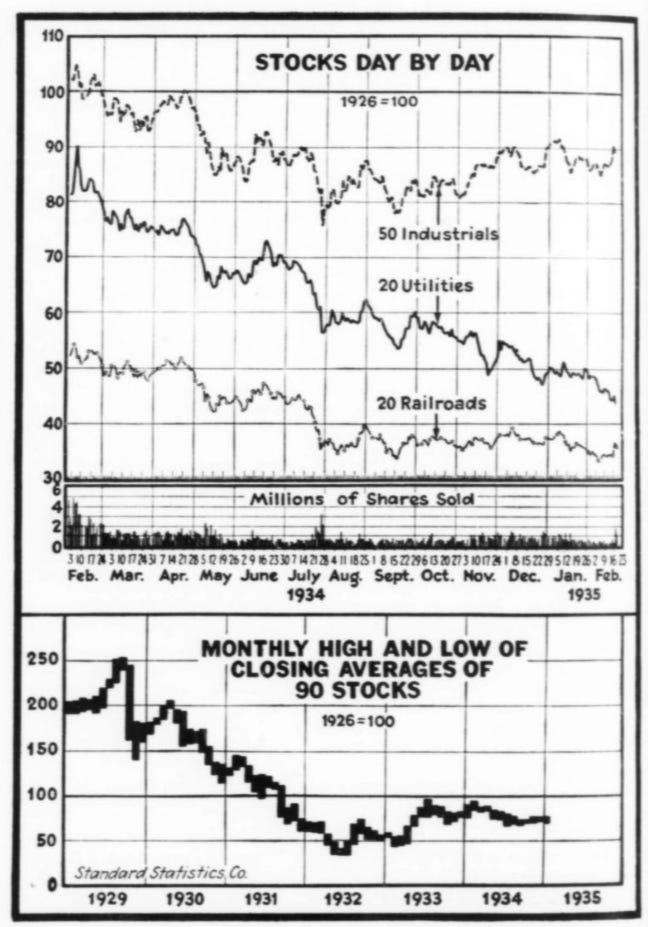

The below chart from the February 23, 1935 edition of Business Week showing that utility stocks in particular just continued their decline during the depression such that most were 50% below their 1926 prices.

As Standard Gas & Electric traveled down its path to eventual receivership in September 1935, Emanuel and his group salvaged some of their personal wealth by profiting from the issuance of new shares of Standard Gas. The SEC eventually caught on and stopped this practice. Emanuel stepped up to lead the company during its receivership period, but would step aside in 1940 to allow Leo Crowley to lead the utility.

Cord Corporation

In addition to salvaging his personal fortune and managing Standard Gas during the Great Depression, Emanuel was still on the hunt for deals. In 1937, Emanuel found an opportunity in Cord Corporation which had a controlling stake in another public company: Aviation Corporation.

Errett Lobban “E.L.” Cord had become an enormously successful salesman of Moon Motor Car Company vehicles in the early 1920s. His commissions at the Chicago dealership at which he worked were running at $30,000 a year. When 1923 rolled around, Cord had had enough of selling cars. He had saved up $100,000 and instead wanted to start making them. Cord was introduced to Ralph Austin Bard who controlled the Auburn Automobile Company. Although Auburn wasn’t profitable and sales were lackluster, Cord saw a situation that could be turned around.

Cord offered the owners of Auburn interesting terms for him to lead their ailing company. He wanted to be paid the greater of $1,000 per month or 20% of the net profits, and he’d also get options to buy shares of the company. The owners of Auburn agreed. Cord quickly turned around the company and by the end of 1925 he owned 70% of the business. Cord used a judicious amount of debt—$250,000—to fund his share purchases, thus affecting a leveraged buyout of the prior owners.

Cord grew Auburn and then acquired many other companies along the way. In 1929, he formed the Cord Corporation as a public holding company for his collection of businesses. Over the years, Auburn Auto and Cord Corp. would (this is not an exhaustive list):

acquire Duesenberg Automobile in 1926;

acquire Lycoming, Ansted Engineering, and Lexington Motor Company in 1927;

acquire Stinson Aircraft, Limousine Body Company, and Columbia Axle Company in 1929;

acquired Aircraft Development Corporation in 1932 to invest behind Gerard Vultee and bring his Vultee V-1 plane into production;

acquire New York Shipbuilding, Checker Cab, and Smith Engineering (maker of airplane propellers) in 1933. Cord was also reported to have acquired 20% of Kansas City Southern Railway in 1933, but he denied these reports.

In 1931, Cord Corp. also founded two airlines: Century-Pacific in California and Century Airlines in Chicago. By April 1932, Aviation Corporation acquired these two airlines from Cord in exchange for 140,000 shares of Aviation. Cord Corporation would go on to acquire another 500,000 shares of Aviation Corporation in the open market for a total ownership of 25% of the company. E.L. Cord would become chairman of Aviation.

The year 1934 is likely the beginning of the end for Cord Corporation. E.L. moved to England for two years and the business was likely undermanaged for the tough economic times it was facing. When Cord moved back to the U.S. in 1936, he came under SEC investigation for stock manipulation of Checker Cab shares and other businesses under his control. Many of Cord Corporation’s subsidiaries and holdings were in dire financial straits. And to further compound the troubles, E.L. would soon have to agree to a consent decree which would prevent him from trading shares in the companies he owned. He needed and wanted an exit from his business interests.

The Solution to E.L.’s Problem

A turnaround situation with a forced seller? What’s not to like? Victor Emanuel again raised capital with Schroders. He also got assistance from E.L. Cord’s own right hand man, Lucius Manning. Everyone together bought out E.L. Cord’s personal stake in Cord Corporation for $2.632 million in August 1937. At the end of it, Lucius Manning was appointed the new president of Cord Corporation and owned a little over 12% of the company. Victor Emanuel and his group now owned 22.15% of the company.

With control of Cord Corporation, Victor Emanuel and Lucius Manning would rapidly restructure and reorganize the enterprise. At this point, Cord Corp. owned a total of 45 companies. The plan was to turn Cord from a bad holding company into a good operating company. The first step in the plan was Emanuel creating three operating segments: AVCO (Aviation Corporation), ATCO (Aviation Transportation Corp.), and AMCO (Aviation Manufacturing).

From here, money-losing businesses were shut down or sold. For example, Auburn Auto ended production of all autos in 1937 and then began reorganization under section 77B of the bankruptcy act in 1938. Emanuel also showed his financial prowess in keeping the three operating subsidiaries afloat—AMCO was borrowing from AVCO which in turn was borrowing from ATCO. Over the years, AVCO strengthened enough so that it eventually swallowed the parent company (Cord) along with ATCO and AMCO.

Another World War

And then World War II began in September 1939.

Stay tuned for Part 2 to learn how Victor Emanuel and Aviation Corporation grew and contributed to the war effort during the extraordinary period of time from 1939 to 1946.

Please Subscribe

If you enjoyed this content, please share and subscribe.

Sources

Periodicals

“UTILITY HOLDINGS SHOW LARGE INCOME”, New York Times, May 4, 1926.

“Insulls Buy Stock in Another Utility”, New York Times, July 28, 1926.

“Big Jump in Stock of Standard Gas”, New York Times, September 28,1929.

“New Banking Groups Enter Standard Gas”, New York Times, December 27, 1929.

Hoskins, Chapin. “How Eleven Cord Companies Made 1931 Record Year”, Forbes, January 1, 1932.

“Century Airlines Sold in a Merger”, New York Times, April 3, 1932.

“Motion For Sale”, TIME, January 18, 1932.

“Aviation Concerns Split By Big Deal”, New York Times, November 10, 1932.

“Farley’s Deal”, TIME, April 23, 1934.

“Cord’s Retirement is Predicted Here”, New York Times, August 8, 1937.

“CORD: Ex-Auto Racer Gives Up A Ship-Auto-Airplane Empire”, Newsweek, August 14, 1937.

“Cord out of Cord”, TIME, August 16, 1937.

“Everything, Inc.”, TIME, October 7, 1946.

Berk, Brett. “The father of Cord was a Gatsby-era genius”, Hagerty, October 4, 2022.

General Reference

Books

Byllesby, Henry M. Public Utilities and Progress. 1912. <https://archive.org/details/publicutilitiesp00byll/mode/2up>

Investment Trusts and Investment Companies: Report of the Securities and Exchange Commission Pursuant to Section 30 of the Public Utility Holding Company Act of 1935. Volume 4, Part 5, page 27. <https://bit.ly/3PKs3D1>

Nelson, Edward. KPL in Kansas: A History of the Kansas Power and Light Company. University of Kansas: Lawrence. 1964. <https://archive.org/details/kplinkansashisto0000nels/page/n3/mode/2up>

Beck, Lee. Auburn & Cord. Motorbooks International, Wisconsin. 1996.

Borgeson, Griffith. Errett Lobban Cord: His Empire, His Motor Cars. 1985.

Disclaimers

The content of this publication is for entertainment and educational purposes only and should not be considered a recommendation to buy or sell any particular security. The opinions expressed herein are those of Douglas Ott in his personal capacity and are subject to change without notice. Consider the investment objectives, risks, and expenses before investing.

Investment strategies managed by Andvari Associates LLC, Doug’s employer, may have a position in the securities or assets discussed in any of its writings. Doug himself may have a position in the securities or assets discussed in any of his writings. Securities mentioned may not be representative of Andvari’s or Doug’s current or future investments. Andvari or Doug may re-evaluate their holdings in any mentioned securities and may buy, sell or cover certain positions without notice.

Data sources for all charts come from SEC filings, Koyfin, and other publicly available information.

I am Victor's grandson. My name is Geoffrey . I stumbled upon your Substack post today. Haven't had a chance to read it yet. Looking forward to seeing Part 2

Love your newsletter, Douglas! It's always a pleasure to read the story of less known entrepreneurs and businesses!