Patience Wanes With CoStar's Residential Foray

A Continuing State of "Show Me the Money"

“When we signed the deal to acquire LoopNet, it had $78 million in revenue. Since then, we’ve grown it and reduced costs and it now has $78 million in EBITDA instead of $78 million in revenue. As my great grandmother always used to say, ‘Buy them for revenue and convert it all to EBITDA.’ She didn’t, really. We should finish this year with about $150 million in LoopNet revenue, so we are approaching doubling the top line since the acquisition.”

—Andy Florance, CEO and founder of CoStar Group, Q3 2015 earnings call

Turning a third-rate asset like Homes.com into a first-rate asset requires time and money. Perhaps a lot of money if you’re going up against the likes of Zillow, which only increases the chance this alchemy fails in its effort to turn lead into gold. Despite Andy Florance’s history of vanquishing competitors and creating several leading online listing portals for commercial real estate and apartments, people are once again in a state of “show me”. Whether its Jerry Maguire or investors in CoStar, they are all shouting, “Show me the money!”, as the company continues to aggressively invest in its primary residential real estate portal with underwhelming financial results thus far.

Homes.com Results as of Q1 2025

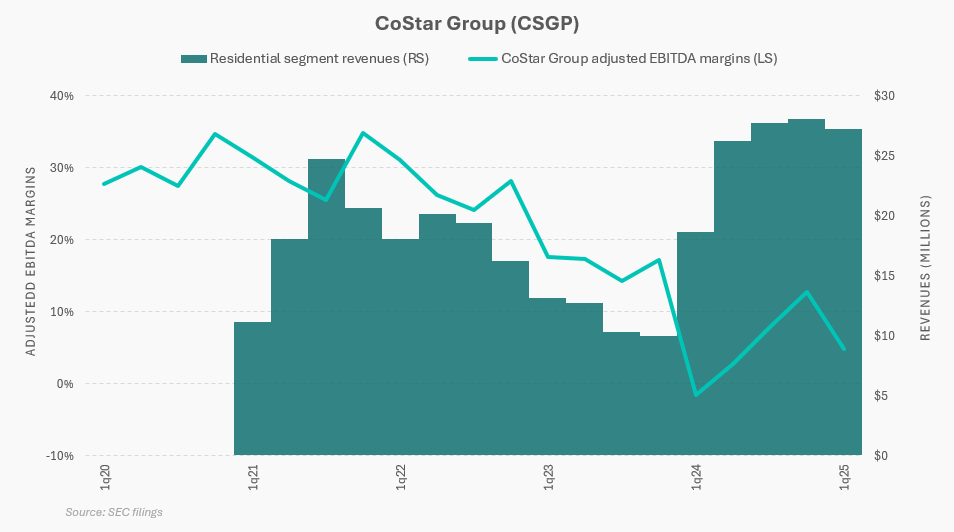

CoStar acquired Homes.com in the second quarter of 2021 for $156 million in cash. Since then, they’ve upgraded the website, integrated it with other CoStar platforms, invested in content creation, and then launched a $1 billion marketing campaign in 2024 beginning with Super Bowl LVIII.

This marketing campaign took down company-wide EBITDA margins down from the 30s to zero. Apparently, the board of directors believed Florance this is what it takes to build the next Apartments.com. Five quarters since the inauguration of this brand-building extravaganza, CoStar has increased Homes.com quarterly revenues from $10 million in Q4 2023 to …

… just $27 million in Q1 2025.

This seemingly reckless investment is the primary concern for nearly all current and prospective CoStar shareholders. But let’s not get ahead of ourselves! If you consider yourself a long-term investor, you should not fail to recognize that it takes more than just a single year of investment to build a valuable brand…

“I have consistently set the expectation of building a B2C brand takes 3 to 5 years. To reach this level of unaided awareness and unaided intent in an audience of hundreds of millions in 14 months is excellent progress. I feel that over the next 2 to 4 years, we can take a solid and very valuable leadership position in the industry.”

—CoStar CEO and founder, Andy Florance, Q1 2025 earnings call

Although quarterly revenues haven’t grown as much as anyone would like given the extraordinary amount of capital already allocated, there are a few non-financial metrics that have seen upticks. These are things like the net promoter score (NPS), average monthly unique visitors to CoStar’s residential network (includes both Homes.com and Apartments.com), and the number of dedicated Homes.com sales reps. These are all worth tracking as they are the few things that might be predictive of future financial results. So far, it’s a mixed bag for these indicators.

First, average monthly unique visitors (AMUs) on the Homes.com network has doubled from 4Q 2022 to the most recent quarter. On the other hand, the $1 billion ad blitz that began in 1Q 2024 quickly produced a 50%+ increase in AMUs, but AMUs have since declined nearly back to where it began at roughly 100 million. Not that impressive given the level of spend. But to be fair, Homes.com as a standalone entity prior to being acquired by CoStar was a nobody in the world of dominant residential real estate portals like Zillow, Realtor, and Redfin.

What has improved a great deal over the same period of time is the net promoter score. This started out at a negative 42 at the beginning of 2024 and now sits at a positive 43, a very noteworthy gain of 85 points in a few years.

Side Note

Net Promoter Score (NPS) is a metric that measures customer loyalty and satisfaction by asking a single question: "On a scale of 0 to 10, how likely are you to recommend this company/product/service to a friend or colleague?" Based on their responses, customers are categorized as Promoters (score 9-10), Passives (score 7-8), or Detractors (score 0-6). The NPS is then calculated by subtracting the percentage of Detractors from the percentage of Promoters, resulting in a score ranging from -100 to +100. This score provides a snapshot of customer sentiment, indicating the likelihood of customers to advocate for the brand (a higher score is better) and can be predictive of business growth.

For comparison, T-Mobile's most recent NPS was 32, Apple's hardware division had a NPS of 60, and Netflix had a score of 68.Unaided awareness of the Homes.com brand has also increased greatly, from 4% to now 36%. CoStar CEO and founder Andy Florance adds some more color on this subject:

“Early last year, our unaided awareness surpassed Trulia. Last summer, we surpassed Redfin’s unaided awareness. And last month, we crossed Realtor.com. When we began, Zillow was 64 points above our unaided awareness. We’ve closed the gap to 24 points and are still improving.

Our unaided intention or the percentage of people surveyed that say they intend to use our site has grown from single digit to 26%. We've also crossed Realtor, Redfin and Trulia on unaided intent. Zillow and Realtor have been trending down while we’ve been growing.”

— Q1 2025 CoStar earnings call

Finally, the number of dedicated sales reps for Homes.com has rapidly increased. There were just 50 at the beginning of 2024 and now there are 378 reps (314 in production and 64 in training). CoStar hopes to have 500 reps by the end of 2025. Florance explains the financial math regarding sales rep productivity:

“Under the very strong leadership of our Senior Vice President of Sales, Andy Stearns, we have grown that small initial team of 50 dedicated sales reps, 600% over the last 14 months to 314 reps in production. Those reps with 4 months of production are turning in a steady $1,612 monthly net new revenue, which implies our straight lines to $232,000 in billings per average rep at the end of 12 months or $1.1 million billings per rep at the end of 5 years of accounting.

The sales force is still growing very rapidly with 64 more in training and with offers out to an additional 214 salespeople. In Q4, we anticipate we’ll have 500 salespeople with 4 months of experience selling Homes.com. That would suggest we could be adding over $800,000 a month new billing each month by Q4.”

— Q1 2025 CoStar earnings call

Another interesting anecdote Florance shared on the Q1 2025 call was that the Homes.com team had a demonstration-to-close rate of 56% in April. Florance said this was the highest monthly close rate he’s ever seen for any CoStar brand. Furthermore, projected cancellations of the Homes.com service to brokers are likely going to fall 70% this May. This has all led Florance to remark, “I believe that by year-end, our Homes.com sales team will be our largest and will be turning in the most net new revenue of … any product area in CoStar Group with regular $1 million net new months for Homes.com.”

Hmmm. We shall see. Time will tell if improvements in any of these metrics will actually lead to growth in revenues and profits for Homes.com.

CoStar Board Refresh

One recent development that should help ease the minds of shareholders—as Florance invests heavily to take on Zillow—is the recent refresh of CoStar’s board of directors.

News came out on April 6, 2025 that CoStar entered into a “support agreement”—apparently a new euphemism for the more typical and Mexican standoff-ish term of “standstill agreement”—with two heavy-hitting investors: D.E. Shaw and Third Point. Both these investors have impressive multi-decade track records of performance and many examples where they have become actively involved in prior investments.

Interestingly, the most recent 13F filings (12/31/24) show D.E. Shaw holding 1.43 million shares of CoStar while Third Point held zero shares. CoStar currently has 410.5 million shares outstanding as of March 31, 2025.

What this likely means is that both accumulated a significant number of shares in just the first quarter of 2025 to the point where they reached out to CoStar and where CoStar felt it had to make some concessions before things got ugly.

The support agreement basically says that D.E. Shaw and Third Point cannot influence other shareholders to vote their proxies a certain way, cannot present any stockholder proposals, or seek the removal of any board member. D.E. Shaw and Third Point also cannot acquire ownership of CoStar above 7.5% and 4.9%, respectively. Finally, this agreement only lasts for less than a year.

In exchange, D.E. Shaw and Third Point supported the election of three new board members following the (forced?) resignations of long-time board members Michael R. Klein, Christopher J. Nassetta and Laura C. Kaplan. Concurrently, the CoStar board established a new “Capital Allocation Committee” chaired by Florance and where the three new board members—Christine M. McCarthy, John Berisford and Robert W. Musslewhite—will also serve. From the April 7, 2025 press release:

“The Board also established a Capital Allocation Committee to support the Board’s and management’s comprehensive review of the Company’s capital structure, capital allocation priorities and financial targets, including for international expansion and significant investments by the Company’s major brands, including CoStar, Apartments.com, LoopNet and Homes.com. As part of its work, the Committee will review the Company’s ongoing investment in Homes.com and ensure an appropriate timeline for profitability.”

The new directors are all experienced in finance and capital allocation. Christine McCarthy most recently was Disney’s CFO and also serves on the board of P&G. John Berisford was most recently President of S&P Global Ratings. Robert Musselwhite is a seasoned CEO, having led the The Advisory Board Company from 2008 to 2017 when it was acquired United Health’s Optum business and where he then assumed leadership of Optum in 2019.

In its Q1 2025 letter, Third Point wrote this about CoStar (emphasis mine):

“Despite the continued strength of its core business, we believe recent capital allocation decisions have derailed CoStar’s compounding algorithm. Over the past five years, management has increasingly focused on leveraging CoStar’s dominance in commercial real estate (CRE) to expand into residential real estate (RRE). The primary vehicle for this expansion has been its nascent Homes.com business, which aims to supplant Zillow as the leading digital marketplace for home sales in the U.S. In pursuit of that goal, we estimate that CoStar is spending almost $1 billion annually on growth investments (and will have spent more than $3 billion cumulatively by the end of this year), but this investment has yet to generate meaningful revenue. Expanding losses at Homes.com have obscured rapid growth in the core business and reduced consolidated EBITDA by approximately 80%.

The market is increasingly questioning the magnitude and duration of future losses, and investment performance has stagnated. After compounding at a ~25% IRR for two decades following its IPO, the stock has now been flat for more than five years, underperforming indices and peers by wide margins.

After several years of uncertainty, we believe it is time for CoStar to begin the journey of meaningful self-help. During the first quarter, we engaged with the company and its founder and CEO, Andy Florance, with the goal of helping the company improve its capital allocation framework. CoStar agreed to add three new directors (all of whom have deep capital allocation experience), create a Capital Allocation Committee of its Board of Directors tasked with establishing a rigorous framework for future capital deployment, including that of Homes.com, and review its executive compensation programs to ensure management’s incentives remain aligned with stockholder value creation. Third Point has signed a standstill agreement that lasts for less than one year, and while results will not be immediate, we expect to see a meaningful improvement in capital allocation by YE 2025.”

For shareholders worried about a lack of discipline in CoStar’s residential investments, a new capital allocation committee composed entirely of fresh outsiders, and the threat of two significant shareholders holding Florance accountable, should feel like a soothing balm.

Summary

Although CoStar is still just at beginning of its journey in building up Homes.com, investor skepticism has only increased. Qualitative metrics have been a mixed bag and financial results underwhelming. This situation has attracted the venerable firms of D.E. Shaw and Third Point, both investors who are willing to take large positions and advocate for change. In the next round of 13F filings, I expect to see that CoStar is a much more substantial holding for both. And instead of the scene from Jerry Maguire where Jerry is begging Rod Tidwell, “Help me… help you”, I believe D.E. Shaw and Third Point are (or will be) in the position to command Florance and the board, “Help us… help you.”

Whatever happens in the coming years, I think at least one thing is likely to happen. Business schools will either be teaching case studies of how CoStar successfully took on the dominant residential real estate portals or how CoStar squandered billions of capital by straying from its commercial real estate roots and attracting the attention of activist investors.

Please Share and Subscribe

If you enjoyed this content, please share and subscribe.

Disclaimers for this Substack

The content of this publication is for entertainment and educational purposes only and should not be considered a recommendation to buy or sell any particular security. The opinions expressed herein are those of Douglas Ott in his personal capacity and are subject to change without notice. Consider the investment objectives, risks, and expenses before investing.

Investment strategies managed by Andvari Associates LLC, Doug’s employer, may have a position in the securities or assets discussed in any of its writings. Doug himself may have a position in the securities or assets discussed in any of his writings. Securities mentioned may not be representative of Andvari’s or Doug’s current or future investments. Andvari or Doug may re-evaluate their holdings in any mentioned securities and may buy, sell or cover certain positions without notice.

Data sources for all charts come from SEC filings, Koyfin, and other publicly available information.