The Mighty Florance

CoStar Group FY2024 Results: Margins Up, Growth Continues

It seems Andy Florance relishes a challenging battle. He defied tradition and the odds when he digitized commercial real estate listings beginning in 1987. Through perseverance, hard work, and a seeming joy of crushing competition on his way to being the best, CoStar is now the preeminent commercial real estate data firm in the world.

Thirty four years later, CoStar entered the residential real estate arena via its acquisition of Homes.com. Since then, the overall investment story—and share price—has been in flux. What are the odds of success? When will the enormous spending slacken and group margins go back up? As a shareholder, I am of course rooting for success here, but some shareholders might be thankful if CoStar cried uncle and gave up on Homes.com. Either way, shareholders will eventually have greater certainty and the story will once again be more “investable” for those who can’t stand uncertainty.

In spite of CoStar’s extraordinarily successful acquisition of Apartments.com and its investment in the multifamily segment, many in the real estate and investment community question whether Andy Florance (CoStar’s founder and CEO) has bitten off more than he can chew. After all, Zillow has been the dominant player for 10+ years.

Our view is that Andy is—as usual—playing the long game. There’s a decent shot CoStar can take market share from Zillow, or at least a bunch from the other minor players. Faster growth in Homes.com has been and will be the result of a superior service offering and superior brand investment. One significant advantage that CoStar has over Zillow? CoStar’s super-profitable commercial real estate businesses (40%+ EBITDA margins) are there to fund the necessary investments.

Here are the highlights from CoStar’s press release on February 18, 2025:

Full Year 2024 revenue increased 11% YoY;

Q4 ‘24 net income increased 13%, EBITDA increased 43% & adjusted EBITDA Increased 47% from Q3 ‘24

Homes.com network solidified its position as the number two residential real estate marketplace in the United States; and

CoStar’s board approved a $500 million stock repurchase program.

I think it’s important to note this is the first significant stock repurchase program in CoStar’s history. They’ve historically repurchased shares to offset the dilution of stock compensation, but this program will certainly more than offset it.

The Long-Term Financial Picture

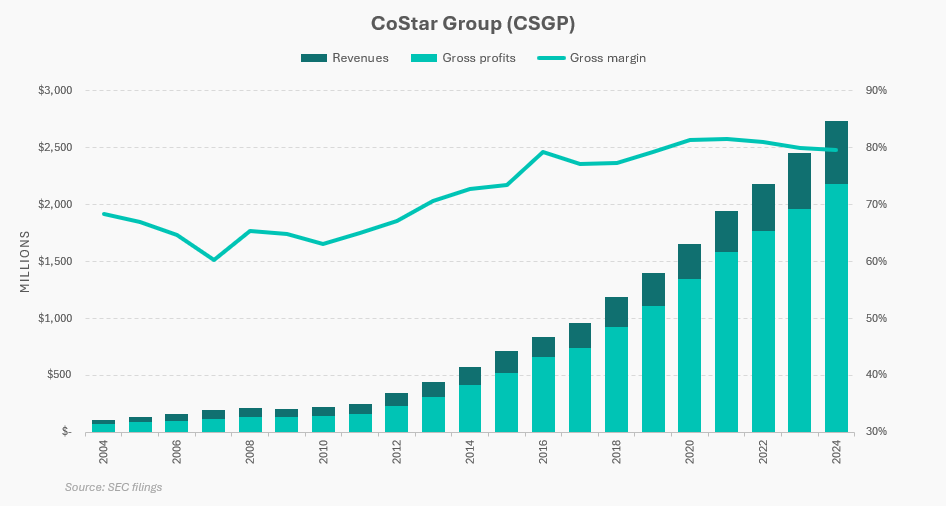

The overall CoStar financial picture remains the same. It’s a highly profitable business with predictable and growing revenues. It plays a tiny, but important, role in the global real estate market, an asset class worth $300 trillion in total value.

With gross margins in the 80% range and significant ability to generate cash, CoStar can afford to make large acquisitions as well as to invest heavily in new businesses and related ventures. Just look at the quarterly EBITDA margins below and the two times they dipped in 2015 and in 2023-2024. These were periods of significant investment in two new and adjacent businesses.

The first big investment was Apartments.com (categorized as their “multifamily” segment). This acquisition turned into a grand slam. Below, you can see total EBITDA margins dropping from 30% to nearly zero after CoStar acquired it and began to invest heavily. But total margins eventually shot back up as they grew the business and gained market share. Revenues at Apartments.com were originally less than $50 million every quarter—where Homes.com is right now—and now they are over $250 million every quarter.

The same thing is hopefully happening again with Homes.com. CoStar’s total margins dipped as it invested heavily in sales and marketing efforts as well as to update Homes.com’s website and offerings. Total margins are now picking up again as Florance eases off the spending pedal a bit. If the Apartments.com pattern holds true with Homes.com, I expect revenue growth to continue and total margins to go back into the 20%-30% range over the coming 1-2 years.

The spend thus far has produced results, albeit web traffic results. In CoStar’s recent call, Florance sums up the amazing progress on building web traffic and brand awareness (emphasis mine):

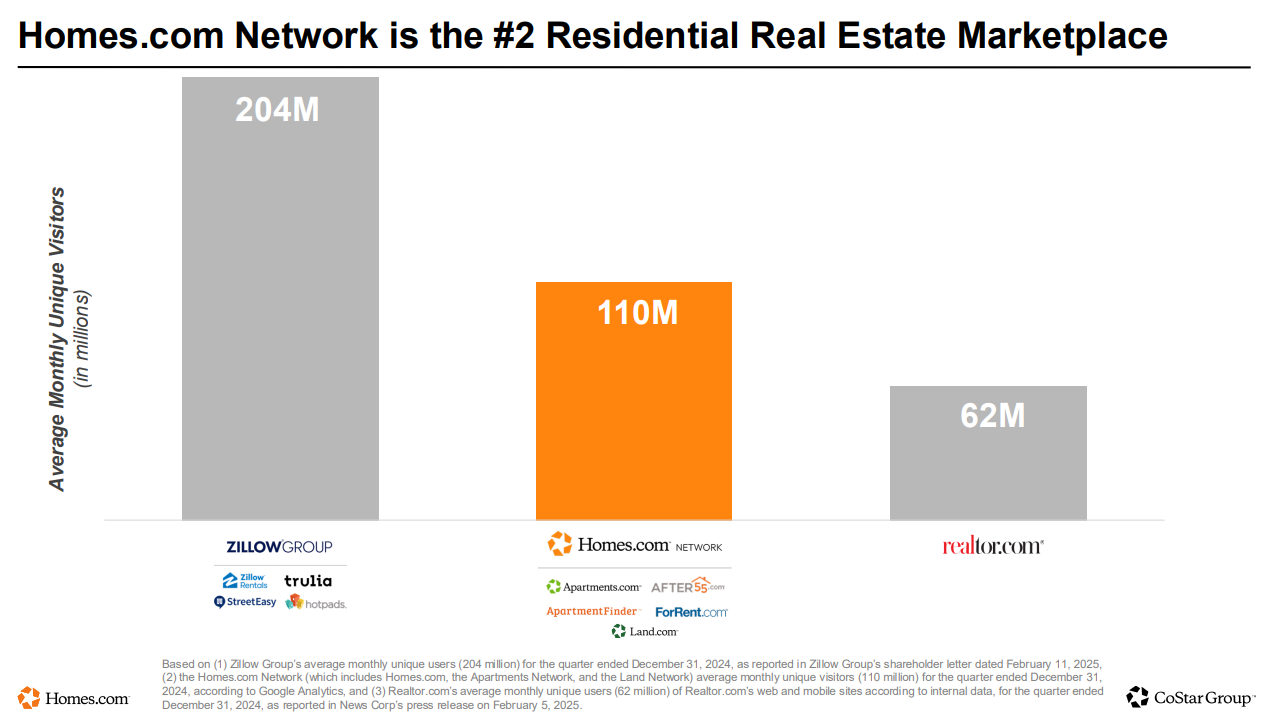

“In less than 1 year, the Homes.com network became the second largest real estate portal in the United States, based on traffic, with an audience of 110 million average monthly unique visitors in the fourth quarter, according to Google Analytics. 110 million unique visitors is nearly double Realtor.com’s 62 million average monthly unique visitors that News Corp reported for the same quarter recently.

I think that’s remarkable. Realtor.com launched 30 years ago in its predecessor form back in 1995, and we passed them in apples-to-apples traffic in our first year of the relaunch.

We began the year with our low single-digit unaided awareness and during the year, built and grew that awareness number to as high as 33%. As we complete our second successful Super Bowl campaign and launch our 2025 campaign, I believe that we can reach 50% unaided awareness this year, potentially surpassing in 2 years what our competitors spent 30 years building.”

And the progress will continue. Whereas in 2024 Homes.com did not have a truly dedicated sales force, 2025 is the year where all people selling Homes.com will only be selling Homes.com and not other CoStar services. These dedicated sales reps will be more productive and more effective at servicing customers, which will aid in retention.

Finally, we might even see CoStar acquiring a large competitor like Realtor.com. Given the more business friendly administration in the White House, it’s much more likely the Justice Department would allow CoStar to acquire Realtor.com with the goal of creating a true competitor to Zillow.

If Homes.com were to acquire Realtor.com, this would cement them as the credible challenger, going from 110 million monthly unique visitors to 172 million, just a bit behind Zillow’s 204 million monthly uniques.

Revisiting CoreLogic

Continuing on the theme of potential M&A activity, and although it might be a long shot, CoStar could conceivably take another bite at the CoreLogic apple. CoStar made a bid for CoreLogic back in early 2021, but CoreLogic rebuffed them due to concerns the deal wouldn’t pass DOJ muster. But Florance couldn’t help but have the last word on the matter. Rather than be the one who was rejected, Florance would be the one doing the rejecting. CoStar formally withdrew its bid on March 4, 2021:

“CoStar Group believes rising interest rates will negatively impact the outlook for the mortgage refinancing market. Accordingly, these rising interest rates have caused valuations for residential property technology companies to decline significantly in recent weeks, which has changed CoStar’s view of the value of CoreLogic. ‘With Interest rates moving up, now is not the time for us to aggressively buy into the residential mortgage market,’ said Andrew C. Florance.”

Private equity ultimately acquired CoreLogic for $6 billion, or $80 per share instead of accepting CoStar’s bid of $95.76. Since then, inflation and rising interest rates, like Florance projected, has been a prime factor in a much diminished mortgage market.

With a good bit of CoreLogic’s business tied to a poorly performing mortgage market and a good bit of debt coming due—$750 million of senior secured debt coming due in May 2028 and a $3.75 billion of first-lien loan maturing in June 2028—its owners might be willing to part with the company sooner rather than later. CoStar currently has $4.7 billion of cash on its balance sheet. I wouldn’t be surprised if, yet again, Florance maintains a good track record on optimally timing asset purchases and sales.

Underappreciated International Results

An underappreciated area of investment for CoStar has been its international businesses. Their results have been excellent over the years. CoStar is now in the U.K., France, and Spain with their CoStar Suite, information services, and LoopNet (commercial real estate marketing). Over the last seven years, these three international segments tripled combined revenues from 2017 to 2024, going from $30.8 million to $94.7 million.

Florance updated listeners on the recent call regarding international segments. First, CoStar will institute a little bit more financial discipline. Second, they will continue to hire aggressively.

“We are in the process of implementing a little bit of financial discipline on P&L across our European operations and making sure that we’re not running multiple versions, the same product running both the acquired and the general broader LoopNet CoStar platform. So we have a little bit of a case where we're running some duplicative costs.

So one of the reasons you won’t see as big a hit in the P&L in the years to come is that we're rationalizing some of those European operations not to run dual initiatives and move towards just a consistent CoStar LoopNet platform in Europe.”

Also on the recent call, Andy highlighted the strength of CoStar’s product in the U.K. with a major competitor pulling completely out of the market:

“EG or Estates Gazette was founded 166 years ago in 1858 during Queen Victoria’s reign and before Abraham Lincoln became President. CoStar has competed against EG and its various companies since we acquired FOCUS in the U.K. in 2004.

When we first began competing with them, they were primarily a weekly commercial property news magazine, stuffed with hundreds of high-paying property ads, but they launched an online commercial property service. EG has also launched an online marketing service called EG Propertylink that compete with LoopNet.

As CoStar gained leading share in the U.K., EG merged their information offering into a brokerage affiliated consortium called Radius. EG was owned by the information giant RELX. In their announcement, they cited irreparable impact of headwinds that have struck the whole of commercial real estate industry hard. I’d like to believe that to some degree, the quality of … research service and technology that our team provides played some competitive role.

RELX may have sold or may in the future sell elements of discontinued businesses to other companies. It is with respect that we acknowledge the hard work contribution achievements of one of the U.K.’s leading commercial property and information sources over 166 years. It’s our competitors that motivate us to be the best we can be.”

Although it only took two decades for CoStar to force this competitor completely out of the market, let this be yet another lesson for anyone who chooses to go up against CoStar and Florance.

Summary

The CoStar story (and share price) has been in flux for the past several years since the acquisition of Homes.com and turning Zillow into a direct competitor. Given Andy’s prescience regarding Zillow’s doomed effort to get into the home flipping business—an eventual multi-billion failure—investors should give him a bit of deference in the residential space. At the minimum, I believe either a negative or positive outcome for Homes.com will result in a positive for the share price.

But even outside of Homes.com, opportunities still abound in international and other adjacent markets in commercial real estate. With $4.7 billion of cash and ample capacity for debt, who knows what the next large acquisition for Florance will be?

Please Subscribe

If you enjoyed this content, please share and subscribe.

Related Content

Q1 2024 Letter: Kelly Partners, CoStar, and Rates

Below is Andvari’s latest letter to clients. Please share and enjoy.

Zillow Ignores CoStar's Shade

Zillow had an interesting 2Q 2024 earnings call. They ignored some of the shade thrown at them a week earlier by Andy Florance, CEO of CoStar Group. Zillow co-founder, and on-again-off-again CEO, Rich Barton, passed the reins. Zillow’s stock price closed up 18% the day after. I snarkily asked on X/Twitter

Q4 2024 Andvari Letter

Andvari Associates has allowed us to share an excerpt of its Q4 2024 letter. They write about cell tower REITs, CoStar, and Topicus.com. Please enjoy.

Disclaimers for this Substack

The content of this publication is for entertainment and educational purposes only and should not be considered a recommendation to buy or sell any particular security. The opinions expressed herein are those of Douglas Ott in his personal capacity and are subject to change without notice. Consider the investment objectives, risks, and expenses before investing.

Investment strategies managed by Andvari Associates LLC, Doug’s employer, may have a position in the securities or assets discussed in any of its writings. Doug himself may have a position in the securities or assets discussed in any of his writings. Securities mentioned may not be representative of Andvari's or Doug’s current or future investments. Andvari or Doug may re-evaluate their holdings in any mentioned securities and may buy, sell or cover certain positions without notice.

Data sources for all charts come from SEC filings, Koyfin, and other publicly available information.

Highly promotional management, questional M&A strategy, underperforming (broken) share price, still high valuation, I think that will not end well.