DOJ Sues Visa Over Debit Card "Monopoly"

My Takes on the Complaint

News leaked this past Tuesday morning the Justice Department would be suing Visa for supposedly anti-competitive practices with its monopoly on debit card processing in the United States.

“Justice Department Sues Visa, Alleges Illegal Monopoly in Debit-Card Payments”, WSJ, Sept. 24, 2024.The complaint came out Tuesday after news reports and I wanted to highlight portions that I thought were most interesting or deserving of some colorful sniping on my part.

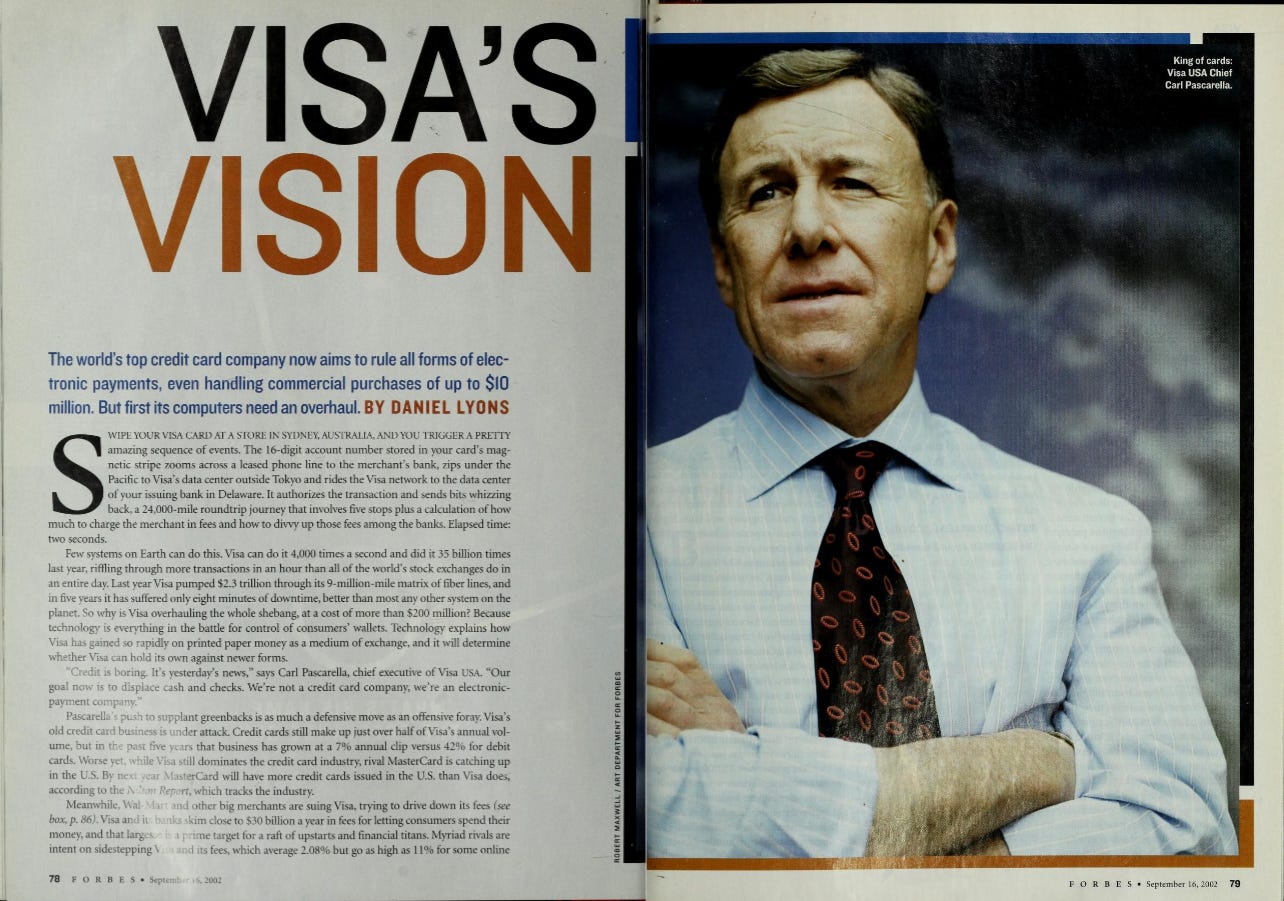

Visa’s Vision

Coincidentally, the recent complaint came almost exactly 22 years after Forbes published a feature article entitled “Visa’s Vision”.

Back then, Visa had the goal of establishing a dominant foothold in all forms of electronic payments. Here are the first three paragraphs of the 2002 Forbes article:

Swipe your Visa card at a store in Sydney, Australia, and you trigger a pretty amazing sequence of events. The 16-digit account number stored in your card’s magnetic stripe zooms across a leased phone Une to the merchant’s bank, zips under the Pacific to Visa’s data center outside Tokyo and rides the Visa network to the data center of your issuing bank in Delaware. It authorizes the transaction and sends bits whizzing back, a 24,000-mile roundtrip journey that involves five stops plus a calculation of how much to charge the merchant in fees and how to divvy up those fees among the banks. Elapsed time: two seconds.

Few systems on Earth can do this. Visa can do it 4,000 times a second and did it 35 billion times last year, riffling through more transactions in an hour than all of the world's stock exchanges do in an entire day. Last year Visa pumped $2.3 trillion through its 9-million-mile matrix of fiber lines, and in five years it has suffered only eight minutes of downtime, better than most any other system on the planet. So why is Visa overhauling the whole shebang, at a cost of more than $200 million? Because technology is everything in the battle for control of consumers’ wallets. Technology explains how Visa has gained so rapidly on printed paper money as a medium of exchange, and it will determine whether Visa can hold its own against newer forms.

“Credit is boring. It’s yesterday’s news,” says Carl Pascarella, chief executive of Visa USA. “Our goal now is to displace cash and checks. We’re not a credit card company, we’re an electronic payment company.”

And Visa invested accordingly. Even in the 1990s, debit was not a sure thing. But by 2002, Visa earned a dominant position there:

“Pascarella’s smartest bet has been on debit cards. Banks resisted them at first, but Pascarella pressed on. Now Visa has almost 50% of U.S debit card business, about $200 billion a year in fees for its banks. Pascarella pushed into corporate cards, too, taking on American Express. Visa generated $65 billion in volume from the corporate card market.”

Visa then continued to innovate. It helped introduce technologies and features that lowered incidence of fraud and sped up time to process cards. It also continued to increase an already significant share in debit. It’s reward twenty years later? A Justice Department complaint (Complaint, U.S. v. Visa, 1:24-cv-7214, U.S. District Court for the Southern District of New York, filed September 24, 2024).

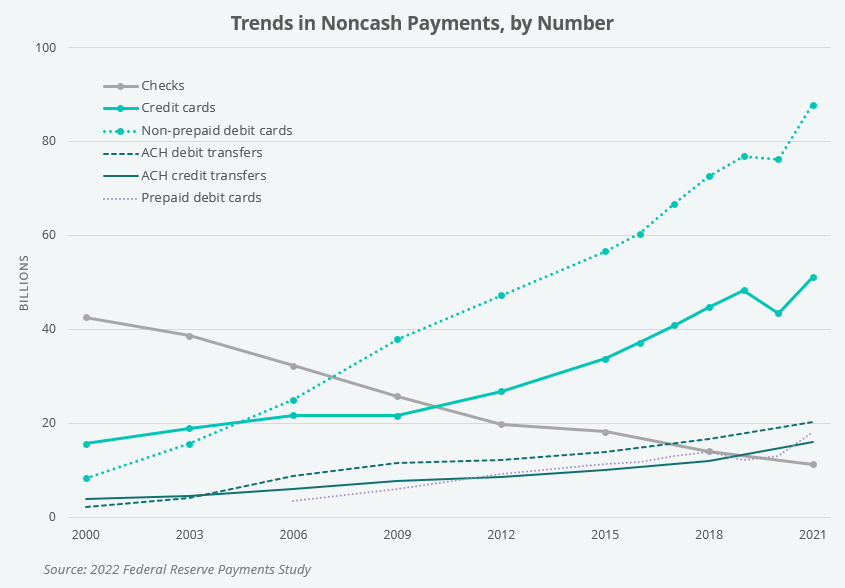

Firstly, the complaint states that many Americans use debit cards, and the numbers are increasing year after year. This is certainly true. In my post on Mastercard, I have a chart showing this fact.

However, it is only a few sentences later the DOJ warns us that a single nefarious actor, Visa, is out to get us all!

“Nor are they aware that one company, Visa, has for monopolized debit transactions; penalized industry participants that seek to use alternative debit networks; and coopted innovators, technology companies, and financial institutions to forestall or snuff out threats to Visa’s debit network dominance.”

In the next paragraph, we see evidence of dominance in market share as well as fat margins:

“In the United States, more than 60% of debit transactions run on Visa’s debit network, allowing it to charge over $7 billion in fees each year for processing those transactions. Visa earns more in revenue from its U.S. debit business than its credit business as of 2022. Visa debit is core to its North American business, where Visa enjoys operating margins of 83%.”

Mastercard is a “distant second” to Visa with just 25% share processing all U.S. debit transactions.

Problems with Scale

Businesses have forever given discounts based on volume. If you’re Walmart or Kroger, you’re probably going to get a better deal from P&G than if you’re a Schnucks based in the Midwest.

If you’re Visa and you’ve built a great network and a brand over the last several decades that provides extraordinary value, then why should you not be able to dictate terms to the issuers and acquiring banks or anyone else who wants to use your network and brand? Why should you not be able to give preferential treatment to those who promise to use your services exclusively? I don’t feel like this is super-blatant anti-competitive behavior, but then again, I’m not an expert on anti-trust.

For truly egregious anti-competitive behavior, just look at the case of Charlotte Pipe. Charlotte and one other company controlled more than 90% of the market for cast iron soil pipes. When a new competitor, Star Pipe, entered the market with cheaper products, Charlotte acquired Star. Charlotte then proceeded to destroy Star’s production equipment, pulled Star's products from the market, and forced Star executives to sign a non-compete for six years. This is the patently blatant behavior that is truly deserving of scrutiny and correction.And when it comes to competition in debit cards, I believe there already is competition in the form of Mastercard, Discover, and American Express. And don’t forget cash and check! But because we’re talking about a business that benefits from network effects, competitors will have to spend and invest way more than they would if they wanted to go up against an incumbent that lacks network effects. Well, why should competing against a business with network effects be easy?

Anyways, when DOJ writes that, “Visa threatens punitive rack rates if merchants (or their acquirers) route a meaningful share of their transactions to Visa’s competitors”, I simply read this as “Visa doesn’t give favorable treatment to merchants or acquirers if they choose not to route most of their transactions on Visa’s network.”

I mean, this is the type of stuff that all businesses should do, right?

Good news from a shareholder’s point of view is that:

“Visa’s routing contracts cover more than 180 of its largest merchants and acquirers, and effectively insulates at least 75% of Visa’s debit volume from competition—which means that Visa has foreclosed nearly half of total U.S. debit volume. Internally, Visa touts the success of its routing deals in limiting competition. Visa renewed many of its routing agreements in 2022 to deepen its debit moat for years to come.”

Again, DOJ continues with its inflammatory tone. I read the above quotes as, “Most of the largest and most sophisticated retailers have found such enormous value in all the services that Visa provides, that they’re willing to sign legal contracts to secure that value for a period of time.”

DOJ spells out what I think is normal business behavior here as well (emphasis mine):

“Merchants and acquirers are willing to accept de facto exclusive deals with Visa because they have a substantial number of debit transactions that they cannot route to any other network—these are non-contestable transactions. The merchant has only two choices: either (1) agree to exclusivity with Visa or (2) pay Visa’s supracompetitive rack rates for noncontestable transactions and try to route its contestable transactions to Visa’s competitors. Visa’s rack rates are frequently higher than the PIN networks’ rack rates. Yet if merchants want to secure better rates from Visa, they typically need to route all or almost all their Visa-eligible debit volume over Visa rails. Most of Visa’s volume commitments are significant, with a minimum threshold of 90–100% of the merchant’s or acquirer’s eligible Visa volume.”

Partnering

Several large digital payment platforms have emerged over the years. These include Apple Pay, PayPal, Cash App, and others. The complaint correctly states, “Visa feared that these digital platforms may have ‘network ambitions,’ and might seek to eliminate Visa and other debit networks as links between consumers and merchants for debit transactions.” Thus, Visa’s strategy has been to “partner with emerging players before they become competitors.” Visa has used both carrot and stick in many cases, offering lucrative incentives and occasionally threatening extra fees to potential competitors to use its products and services.

This again sounds kinda bad? But these are all rational businesses involved in these deals. There are already several well functioning payment networks that exist. Why would PayPal or Klarna or Plaid or any other company focused on their unique niches in the payments space want to reinvent the wheel (the payment network) at such an extraordinarily high cost?

Visa and Mastercard today have a combined market value of ~$970 billion. Given this fact, the government’s argument just doesn’t make sense. Apparently, all it takes to dissuade some of these potential new competitors are incentives of either tens of millions of dollars—or a hundred million at the high end. If someone was actually a true potential competitor, with runway to invest in a product that could take even just 1% of the combined market value of Visa and Mastercard for themselves, why would they accept a paltry incentive to not directly compete?

Visa’s North America Margins

The complaint states several times that Visa’s operating margins in North America are 83%. Just an incredible number and shows how great a business this is.

Key Takeaways

Again, I’m not an expert in anti-trust law. I just mainly have a feeling that if a person or a business builds something that people love, they should be able to do almost anything they want with it.

The DOJ complaint is a good read that provides a few new insights into the dominant business Visa has built over the decades. In North America, Visa has over 60% share of all debit transactions and 80%+ operating margin. This margin far exceeds the margins it has in other parts of the world.

I highly recommend reading the full complaint. You’ll get a good basic understanding of how the business works and how Visa has used its position as owner of one of the world’s most important networks.

Please Subscribe

If you enjoyed this content, please share and subscribe.

Disclaimers

The content of this publication is for entertainment and educational purposes only and should not be considered a recommendation to buy or sell any particular security. The opinions expressed herein are those of Douglas Ott in his personal capacity and are subject to change without notice. Consider the investment objectives, risks, and expenses before investing.

Investment strategies managed by Andvari Associates LLC, Doug’s employer, may have a position in the securities or assets discussed in any of its writings. Doug himself may have a position in the securities or assets discussed in any of his writings. Securities mentioned may not be representative of Andvari's or Doug’s current or future investments. Andvari or Doug may re-evaluate their holdings in any mentioned securities and may buy, sell or cover certain positions without notice.

Data sources for all charts come from SEC filings, Koyfin, and other publicly available sources.