Zillow Ignores CoStar's Shade

Each Going After the Other's Core Business

Zillow had an interesting 2Q 2024 earnings call. They ignored some of the shade thrown at them a week earlier by Andy Florance, CEO of CoStar Group. Zillow co-founder, and on-again-off-again CEO, Rich Barton, passed the reins. Zillow’s stock price closed up 18% the day after. I snarkily asked on X/Twitter whether shares were up because Barton was stepping down.

A Recent Past Best Forgotten

During the many years of ultra-low interest rates, and then during the COVID years of forced savings and suburban/rural migration, the prices of homes seemed to have a manageable volatility. This turned out to be the perfect lure for galaxy-brain visionaries like Barton to conclude that what Zillow really needed to be doing was buying and flipping homes. The simple idea was for Zillow to be the one-stop shop for all services related to buying and selling a home. They would create the residential real estate super app to go after a TAM that was now in the trillions of dollars.

Realistically, I imagine Barton and other Zillow execs also felt some equal doses of envy and FOMO seeing the fast growth and apparent successes of VC-funded home flipping businesses like Opendoor and Offerpad.

I wrote four years ago—geez, it feels like yesterday—on “The Perils of Growth Seeking”. This blog was about Zillow’s entrance into home flipping (also known as “iBuying”) and CoStar’s Florance taking a skeptical view of Zillow’s odds of success. I sided with Florance back then.

After much bravado, some poor investor relations person wasting hundreds of hours on slide decks about Zillow’s greatly expanded TAM, and just a few short years into its venture, Zillow announced the end of its iBuying program in late 2021. Zillow laid off 25% of its workforce and had a write-down of more than $540 million on its gamble.

For now, let’s let bygones be bygones and move on to my thoughts about Zillow’s 2Q 2024 earnings call.

Zillow’s 2Q 2024 Call

I wrote down half a dozen points I thought were interesting, either for what they said or for what they failed to say.

Election Polls Versus Election Results

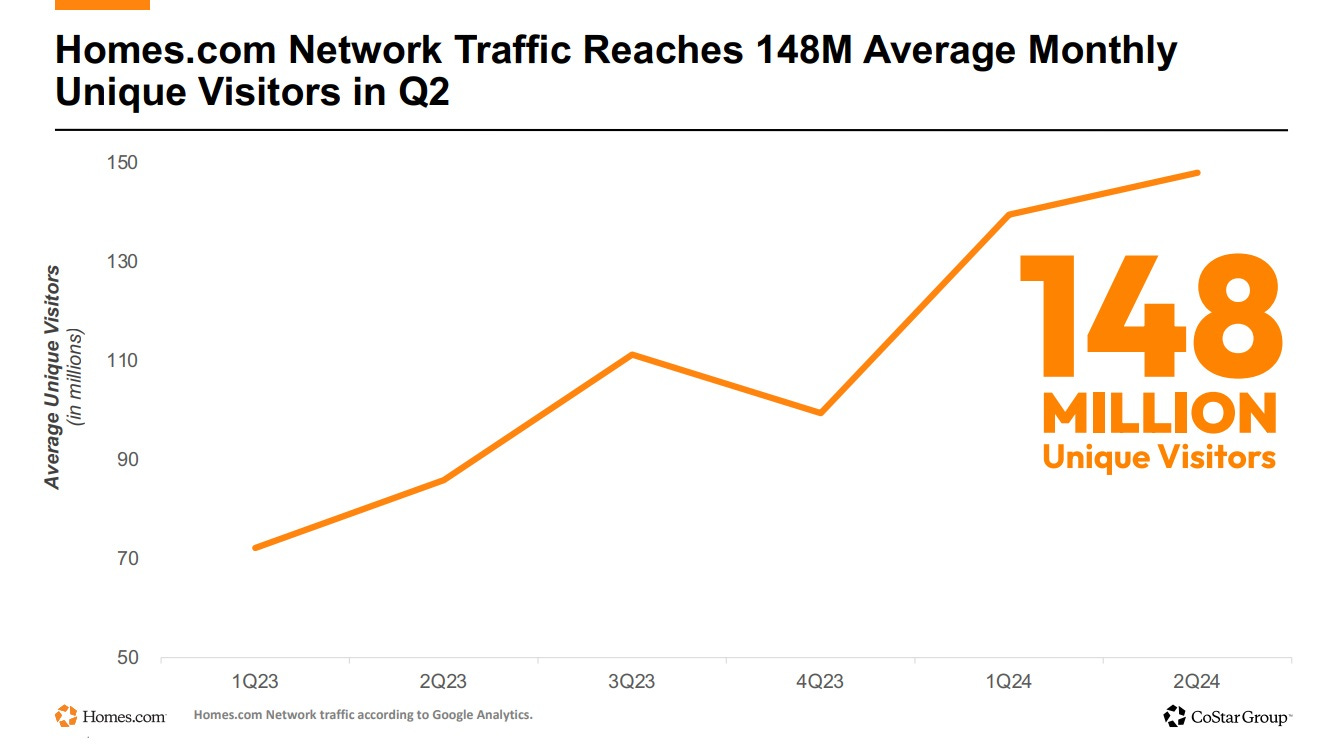

CoStar had its quarterly call the week before Zillow’s. Florance cited continued, impressive traffic growth: “The Homes.com network delivered 148 million average monthly unique visitors for the second quarter, according to Google Analytics, which was an increase of 73% over the same quarter last year.” Homes.com network traffic is quickly approaching Zillow’s quarterly traffic of 217 million average monthly unique visitors.

Furthermore, Florance decided to make an interesting distinction on the validity and accuracy of different site traffic reporting tools. He said:

“We believe that complete site-centric census style tool, like Google Analytics is more accurate than user-centric panel estimate counts generated by firms such as comScore or Semrush. I believe tools like Google Analytics are like an election result, whereas a tool like Semrush or comScore is more like an election poll. If I have the election results, I choose to report those rather than the sample poll result.”

Fair enough. However, on Zillow’s quarterly call, for some reason they continued to cite their traffic numbers, specifically calling out their use of comScore.

According to new Zillow CEO, Jeremy Wacksman:

“Another way to measure traffic and brand strength is through Comscore, which is widely viewed among Internet brands as a reliable, transparent third-party source because it aims to capture the number of unique visitors while deduping cookies. According to Comscore, Zillow Group’s apps and sites had 116 million average monthly unique visitors in Q2.”

Despite having surely heard Florance, I think the Zillow team could have better addressed Florance’s claim.

Zillow’s Profitless Business Model

While Andy Florance has praised other successful online real estate portal businesses multiple times over the years—Rightmove of the U.K. and REA Group of Australia—Zillow seems incapable of learning a lesson or two from these exemplars.

Florance even added a page in CoStar’s slide deck to hammer in this point. The chart below shows the cumulative net profits over a ten year period of Zillow compared to other leading online real estate portals.

That Zillow, despite having had the dominant position in the U.S. for many years, has cumulatively lost money during the entire 2014-2023 period is mind-boggling. But Zillow is certainly aware of how REA Group and Rightmove do things. The last and only time Zillow has ever spoken about REA was in 2013 during its Investor Day and during a November 2013 quarterly earnings call. But this was mostly just to illustrate the potential for Zillow to take market share in the U.S. and what that might mean for its enterprise value. No mention of profits or cash flows.

“Challenging” Real Estate Environment

I laughed out loud at the description of the current residential real estate market as “challenging”. Based on Zillow’s historic financial results, the environment seems to have been challenging throughout its entire history as a public company.

Zillow Going After Rentals

One of Zillow’s “exciting growth businesses” is the rentals category, which Zillow has historically left mostly untapped. This recent quarter, revenues from rental listings grew 29% year-over-year to $117 million. These are great results. And yet it is still amazing its taken them this long to focus on the opportunity. However, they are going up against the dominant Apartments.com, owned by CoStar. In the recent quarter, Apartments.com grew revenues 18% to reach $264 million.

Summary

Zillow’s share price has gone nowhere for the last decade. During the COVID years, they went on a wild tangent with their home flipping idea. It only took a few years to dispel them of the credibility of that notion. Now, twenty years after its founding, Zillow is finally engaging in a “march to GAAP profitability.” Perhaps they’re finally getting religion because they have a merciless competitor starting to breathe down their neck?

To me, it just seems like Zillow has been a publicly-traded VC unicorn taking full advantage of public liquidity. All growth, no profits, and just continual shareholder dilution. Over the prior decade, Zillow’s share count has ballooned from 98 million to 242 million.

Given the full court press Andy Florance is executing against Zillow’s core business, it sounds a touch silly for Zillow to be so positive given who they’re up against in rentals. But of course, one can also say that CoStar and Florance may have been touched by a little madness thinking they can go after Zillow who has had the dominant online residential real estate portal in the U.S. for such a long time!

It undoubtedly will be a while before anyone can declare victory or defeat in this battle between Zillow and CoStar, but this is a spectacle I will eagerly watch over the coming years.

Please Subscribe

If you enjoyed this content, please share and subscribe.

Disclaimers and Notes

The content of this publication is for entertainment and educational purposes only and should not be considered a recommendation to buy or sell any particular security. The opinions expressed herein are those of Douglas Ott in his personal capacity and are subject to change without notice. Consider the investment objectives, risks, and expenses before investing.

Investment strategies managed by Andvari Associates LLC, Doug’s employer, may have a position in the securities or assets discussed in any of its writings. Doug himself may have a position in the securities or assets discussed in any of his writings. Securities mentioned may not be representative of Andvari's or Doug’s current or future investments. Andvari or Doug may re-evaluate their holdings in any mentioned securities and may buy, sell or cover certain positions without notice.

Data sources for all charts come from SEC filings, Koyfin, and other publicly available information.