In a recent episode of the Preferred Shares podcast, I gave an abbreviated history of Saturn Industries/Tyler Corporation, how it became Tyler Technologies in the late 1990s, as well as a breakdown of the current business and its prospects. I’ve owned shares of Tyler since late 2018.

One part of Tyler’s story we did not discuss fully to my satisfaction was the reasoning and catalysts behind the divestitures of all of its traditional, industrial operating businesses from the late 1980s until the final sale of its namesake, Tyler Pipe, on December 1, 1995.

The leveraged buyout and private equity frenzy that began in in the early 1980s is the backdrop for Tyler’s founder and long-time CEO, Joseph F. McKinney, to begin the process of undoing decades of acquisitive growth.

Private Equity and Leveraged Buyout Frenzy

“A man who thinks for himself”, Forbes, April 2, 1990:

In April 1985 Joseph McKinney, founder and chairman of Dallas-based Tyler Corp., was with one of Tyler’s directors attending the Michael Milken/Drexel Burnham Lambert Predators’ Ball in Beverly Hills. The director was charged by the financial energy Milken exuded. McKinney was scared. “I felt,” he recalls, “like I was scuba diving in a shark tank without a knife.”

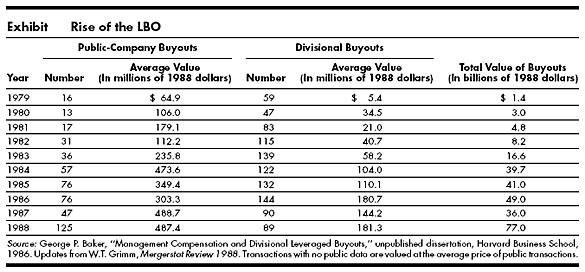

According to a 1993 Journal of Finance article, over 2,000 leveraged buyouts occurred between 1979 and 1989 for a cumulative value of over $250 billion. A new era of high-yielding junk bonds (thank you, Michael Milken and Drexel Burnham Lambert), along with many tantalizing stories of wealth creation, both contributed to this frenzied period of M&A.

For example, two incredible LBO deals were Gibson Greetings and Sterling Jewelers.

In 1982, a group of investors acquired Gibson Greetings for $80 million, of which only $1 million was equity from the investors. Just 16 months later, the investors took Gibson public in a $290 million IPO. The investors made about $66 million.

Sterling Jewelers was one of the earliest successes of private equity firm Thomas H. Lee Partners. The firm acquired Sterling for $28 million with just $3 million of equity. Two years later in 1987, Lee sold Sterling for $210 million. On that $3 million of initial equity, the firm earned $30 million.

These, and many other examples, contributed to the takeover fever becoming an “epidemic”. The fever culminated with KKR’s enormous $31.1 billion acquisition of RJR Nabisco in 1989 and the bankruptcy of Drexel Burnham Lambert in 1990.

The Reasoning Behind Tyler’s Divestitures

Further down in the 1990 Forbes article, McKinney shared another memory from that fateful 1985 Predators’ Ball conference:

McKinney still remembers the excited director at the Beverly Hills conference urging him to jump on the junk wagon and do more deals. He recalls the conversation:

“Joe,” argued the director, “the banks wouldn’t do these deals if they didn’t hold water.” Replied McKinney: “If you evaluate deals based on what the banks will lend on, you’re in trouble.”

Not long after his director tried to get him to buy more assets, McKinney decided it was time to sell.

McKinney’s decision to sell was both defensive and offensive. It was defensive in that it would prevent Tyler Corporation from becoming the target of an LBO. It was offensive in that McKinney could accrue the greatest value to Tyler shareholders rather than outsiders and interlopers taking it for themselves.

In 1987, when takeover fever had become epidemic, Tyler had operations in electronics distribution, specialty coatings, explosives and cast-iron pipe and fittings for the construction industry — just the kind of collection of salable assets the raiders were looking for. McKinney: “Our stock was at 9 to 10 and was worth 22. The thought of a raider popping a deal on us at 15 was to me very repugnant.”

And when Forbes asked McKinney why not lead a management buyout of Tyler, McKinney demonstrated high moral and ethical standards (emphasis mine):

Why not organize an insiders’ buyout and capture the value difference for management? McKinney, who owns 5% of Tyler’s equity, turns up his nose. “From the moment you make that decision, you put yourself on the other side of the table from the stockholder, and he’s the guy you’re working for.”

Instead, McKinney began selling Tyler Corp.’s pieces in the junk-bond-fueled asset market.

Tyler’s Divestitures

Tyler sold Hall-Mark Electronics, an electronics distribution business, in August 1988 to a firm controlled by Los Angeles-based merchant banker Riordan Freeman & Spogli. Tyler received $211 million in cash after expenses.

Tyler sold Reliance Universal to Akzo N.V. in Late August 1989 in a tax free transaction. Tyler shareholders received about one-seventh of an ADR of Akzo.

The next to go was Atlas Powder. Imperial Chemical Industries PLC acquired Atlas in May 1990. This was another tax free transaction in which Tyler shareholders received ICI securities worth about $6.01 at the time.

From the third quarter of 1988 to the end of 1991, Tyler shareholders received a total of $21.96 per share of value from:

$0.445 per share in regular cash dividends;

a $10.00 special dividend after the sale of Hall-Mark Electronics;

$4.87 worth of Akzo securities for each share of Tyler ($4.86 of securities plus a $0.01 rights redemption payment) from the Reliance Universal transaction; and

$6.64 of ICI securities ($6.00 of securities, a $0.01 rights redemption payment, and $0.63 of Reserve Shares) from the Atlas Powder transaction.

Tyler’s highest share price in the quarter prior to the Hall-Mark sale was $15.50. At the end of 1991, Tyler’s share price traded at a high of $3.00. However, adjusting for the total value of dividends and distributions during this time, the adjusted price would be $24.96 ($3.00 + $21.96). This was a total return of about 61%. The Vanguard 500 Index Fund would produce a total return of about 70% in roughly the same time period (6/22/88-12/31/91). This comparison between Tyler and Vanguard’s fund is just my best estimate.

1991: A New Beginning

At the end of 1990, Tyler had sold Hall-Mark, Atlas Powder, and Reliance Universal. It had reduced its debt substantially and had a good amount of liquidity to pursue new acquisitions. Tyler Corp.’s last remaining industrial business was Tyler Pipe.

The first new business Tyler Corp. acquired was Forest City Auto Parts (“Forest City”) in February 1991. Tyler Corp. paid $26 million for Forest City, with potential future earnouts of up to $6.6 million. In 1991, Forest City had sales of $62.6 million and operating profits of $6.5 million. Tyler thus acquired the company at 4x operating profits on the low end and potentially 5x at the high end.

Tyler’s second acquisition in its next chapter was Institutional Financing Services (“IFS”), a company that assisted schools in fund raising by arranging for students to sell company-supplied gift items to family and friends. Tyler acquired IFS on January 6, 1994 for $50 million. IFS’s results for 1993 were sales of $68.2 million and operating profits (before amortization and interest expense) of $6.4 million. Tyler paid 7.8x operating profits for IFS.

The next transaction would be the sale of Tyler Pipe. In his letter to shareholders in 1995, Tyler CEO Joseph McKinney wrote this:

After receiving an unsolicited offer for Tyler Pipe, the Company pursued several ideas, and the agreement with an affiliate of McWane resulted. The decision to sell Tyler Pipe was a very difficult one given our 27-year relationship. We are motivated by what is good for our stockholders, however, and believe the transaction met that test.

Acquired in 1968, Tyler Pipe has been a critical factor in the overall success of Tyler Corporation. The collaboration between the two companies has been one of the finest business experiences of my lifetime. I have benefited and feel honored to have been associated with Tyler Pipe’s employees.

Tyler Corp. completed the sale of Tyler Pipe on December 1, 1995. McWane, Inc., located in Birmingham, AL, paid $85 million and Tyler received $66.1 million in net cash proceeds. This was the end of the final chapter in Tyler Corporation’s life as an industrial conglomerate.

1994-1996: Things Fall Apart

Meanwhile, the year of 1994 was the beginning of the end for McKinney’s decades-long leadership at Tyler. Its two new consumer-focused businesses were showing cracks in their operations. Forest City had grown revenues ~50% since acquisition in 1991 up until the end of 1994. However, operating profits fell from $7.1 million in 1993 to $5 million in 1994. Revenues and profits would decline again in 1995 and 1996. IFS, acquired at the beginning of 1994, would quickly produce terrible results. Sales for 1994 were down 10% relative to 1993. Sales would decline further in each of the next two years.

Results of Forest City Auto Parts and IFS

Forest City Results: 1994-1996

The reasons behind the worsening results for Forest City were several. First, Forest City had to lower prices in 1994 and again in 1995 to respond to the pressures from other auto-parts retailers. The increased competition was a result of aggressive consolidation within the industry from the likes of AutoZone, Advance Auto Parts, and CSK. Competition was also expanding into the Northern and Midwestern markets of Forest City.

Overall sales and profits would decline again in 1996 due to increasing competition.

IFS Results: 1994-1996

For IFS, sales were down 10% in 1994 due to poor international results. In particular, rules enacted by Mexico, Venezuela, and other Central American countries, “virtually eliminated fundraising involving students.” IFS discontinued its operations in these markets.

In 1995, revenues declined again, but profits increased increased a bit, thanks to price hikes and the discontinuation of its Central American businesses in 1994. Then in 1996, sales declined 18%. IFS lost significant market share due to competitive pressures on the profit percentages offered to school sponsors. IFS also had above average turnover in its established sales force, most likely a reflection of its declining prospects.

Throwing in the Towel

With several years in a row of diminishing results at Forest City and IFS, Tyler took a massive write-off of goodwill of both enterprises and also had to spend cash on restructuring charges. The cumulative goodwill write-off was $52.1 million and the cumulative restructuring and other charges were $9.9 million.

After three decades of leading Tyler Corporation, CEO Joseph McKinney announced his retirement on October 7, 1996.

A Tribute & Lessons Learned

“He steadfastly encouraged executives and other employees to own large personal stakes in the Company to ensure that both management and shareholder interests were one and the same. He never wavered from this principle.”

If only there were more executives like McKinney.

Shareholders First

The most important takeaway is McKinney’s steadfast belief that he worked for Tyler shareholders and it was his objective and duty to grow the per share value over the long-term. He had an enviable track record of performance—even withstanding the unfortunate results at the end of his career—of delivering a 100x return from 1966 to 1996.

But the track record for which McKinney should be most lauded is his commitment to shareholders. McKinney chose to do the difficult, but right, thing in the 1980s by shrinking the company instead of growing it during the M&A frenzy. By doing this, he prevented the sharks from capturing the large gap between the market value and fair value of Tyler. Shareholders were the beneficiaries, not some PE firm that might have laden the company with a dangerous amount of debt.

Circle of Competence

There are two other lessons from this period of Tyler’s corporate history. One is the importance of staying within one’s circle of competence. When McKinney acquired Forest City in 1991 and IFS in 1994, there are probably a handful of factors behind this ultimately dismal allocation of capital. Perhaps McKinney was attracted by the low multiples at which he could buy Forest City and IFS—and maybe the multiples were low for a reason for these businesses. Maybe it was just terrible luck these two acquisitions turned out awful.

But I think the most important factor was McKinney ventured into retailing and consumer-oriented businesses after three decades of owning industrial companies that sold to other businesses. There likely was some level of underestimation of the attractiveness of these new businesses relative to what lay within McKinney’s circle of competence.

Control Your Destiny

The second lesson is the importance of voting control. Without control of the founder of the business or a collection of long-term minded and beneficent shareholders, a management team always has the risk of barbarians banging at their gates if there is ever a disconnect between the market value and fair value of the business.

At the end of 1988, McKinney owned 5.97% of Tyler shares and the remainder of all other directors and executives owned 4.81% of Tyler. This totaled to 10.78% of shares outstanding—insufficient to protect the company from private equity buyers who might quickly extract most of the latent value for themselves only. If McKinney had had super-voting shares like Warren Buffett with Berkshire Hathaway, he likely would not have sold Tyler’s good industrial businesses. Instead, McKinney could have waited patiently during the LBO frenzy. He could have paid down debt and let cash build up to acquire companies on the cheap after the frenzy had passed.

But this was not to be. McKinney, a man of principles, was stuck between a rock and a hard place. He decided the best—and only—thing to do was take advantage of the LBO frenzy and capture value for Tyler shareholders. It is just truly unfortunate this correct course of action led to: (1) the two dreadful acquisitions of Forest City and IFS; and (2) McKinney’s likely early retirement. Having control means a CEO or founder will not be forced to make potentially sub-optimal decisions. Control means the power to think and plan for the long-term whether times are good or bad, ebullient or depressive.

Silver Linings

As painful as the mid-90s were for Tyler Corporation and McKinney, there is a silver lining. It did directly lead to the next great chapter in Tyler’s life. Louis Waters acquired a 10% stake in Tyler and then advocated for the company to pursue a roll-up of the many niche software businesses serving local and municipal governments. Tyler Corporation changed its name to Tyler Technologies and embarked on yet another—perhaps the most fruitful—chapter of its corporate life.

Please Subscribe

If you enjoyed this content, please share and subscribe.

Further Reading & Listening

Bork, Robert H., Jr. “The Survivor”, Forbes, February 27, 1984.

Taylor, Alexander L. “Buyout Binge”, TIME magazine, July 16, 1984. <https://time.com/vault/issue/1984-07-16/page/56/>

Jensen, Michael C. “Eclipse of the Public Corporation”, Harvard Business Review, September-October 1989. <https://hbr.org/1989/09/eclipse-of-the-public-corporation>

Mack, Toni. “A man who thinks for himself”, Forbes, April 2, 1990.

Berman, Phyllis. “Tom Lee is on a roll”, Forbes, November 17, 1997. <https://web.archive.org/web/20160327074541/http://www.forbes.com/forbes/1997/1117/6011126a.html>

Disclaimers

The content of this publication is for entertainment and educational purposes only and should not be considered a recommendation to buy or sell any particular security. The opinions expressed herein are those of Douglas Ott in his personal capacity and are subject to change without notice. Consider the investment objectives, risks, and expenses before investing.

Investment strategies managed by Andvari Associates LLC, Doug’s employer, may have a position in the securities or assets discussed in any of its writings. Doug himself may have a position in the securities or assets discussed in any of his writings. Securities mentioned may not be representative of Andvari’s or Doug’s current or future investments. Andvari or Doug may re-evaluate their holdings in any mentioned securities and may buy, sell or cover certain positions without notice.

Data sources for all charts come from SEC filings, Koyfin, and other publicly available information.