TransDigm: The Early Years

Developing the Playbook and Applying it With Consistency

[W]hen you think of TransDigm, you want to think of a private equity-like model being run in the public market. This is somewhat unique for industrial companies in the New York Stock Exchange; … if you don't understand that, it’s difficult to understand how we operate.

—Nick Howley, TransDigm Founder and CEO, February 8, 2013

A driven management team that acquires good companies in a good industry is one thing. But the same management team consistently applying an unchanging, proven value-creation strategy, that allows them to turn those good businesses into exceptional businesses? That is nye an alchemical process. The financial and shareholder results are hard to comprehend, let alone believe.

With such a track record of performance, its easy to understand why this acquisitive aerospace parts company has been studied so much by investors. There’s not too much more to add to overall picture except for my thoughts and ramblings in this post on its early history and what stands out for me, which is this: a strategy that has not changed much over four decades.

In a world where corporate logos change every 10-15 years and where the front cover of glossy annual reports change every single year, TransDigm’s business and value creation strategy has a consistency that few others can brag about.

Thanks to William Thorndike generously sharing a variety of documents from 1993 to 2003, and thanks to SEC filings for TransDigm that started showing up between 1999 and 2003, a good seven years before its 2006 IPO, we get an interesting view of the early TransDigm, how and why it landed upon its value creation strategy, and why they’ve stuck with it for so long.

Imo Industries

TransDigm was born out of the management-led leveraged buyout of the aerospace division of Imo Industries in 1993. The Imo division included the well-known aerospace businesses of Wiggins Connectors (founded in 1925), Adel Fasteners (founded in 1938), Aeroproducts (founded 1935), and Controlex (founded 1945).

But to appreciate why TransDigm founders Nick Howley and Douglas Peacock got the opportunity to acquire Imo’s aerospace businesses in 1993, we need to study the history of Imo Industries.

Imo’s story begins in Stockholm, Sweden, in 1890, when Dr. Carl Gustaf Patrik de Laval, known as the “Thomas Edison of Sweden,” founded Gustaf de Laval Angturbin Fabrik to produce his innovative geared steam turbine. Recognizing the potential for industrial efficiency in the U.S., the De Laval Steam Turbine Company was incorporated in 1901 in New Jersey. By 1902, its Trenton plant was producing gears, centrifugal pumps, compressors, and steam turbines, becoming a major supplier for city waterworks pumping equipment. The company became a key supplier of power-generating equipment to the U.S. Navy during World War I and also supplied precision reduction gearing for naval vessels.

In 1962, Transamerica Corporation, near the beginning of its phase of diversification and conglomeration, acquired the De Laval Turbine Company. Transamerica integrated De Laval with its existing manufacturing subsidiaries and significantly increasing De Laval’s earnings. Corporate offices moved to Princeton, New Jersey, in 1971, and the company continued to grow and expand globally throughout the 1970s and early 1980s.

By the late 1980s, Transamerica was now starting to de-conglomerate. Transamerica spun off Imo Delaval in 1987 as an independent public company, which was subsequently renamed Imo Industries, Inc. in 1989.

Interestingly, as Imo’s former parent company Transamerica was in the process of divesting and spinning off unrelated businesses, newly independent Imo Industries took full advantage of the junk bond market to embark on an acquisition spree and turn into somewhat of a conglomerate of its own. Imo acquired companies like Baird (spectrometers, optical systems), Incom International Inc. (electronic controls, power transmission), and Varo (night vision equipment). Revenues grew from $330 million in 1987 to roughly $1 billion in 1991. However, this strategy of growth via acquisition led to substantial long-term debt.

When asbestos litigation came into full swing in the early 1990s, Imo was one of the many targets. Imo would face about 7,000 legal suits alleging “injury caused by asbestos.” With a heavy debt load from prior acquisitions and now facing serious legal liabilities, Imo had to sell some of its businesses. One of many divisions Imo decided to sell was its aerospace parts division in 1993. Four businesses comprised this division: Wiggins, Adel, Aeroproducts, and Controlex.

With Imo putting these aerospace businesses up for sale in 1993, this is when two executives of the Imo aerospace division stepped up to take advantage of the opportunity: Doug Peacock and Nick Howley.

Doug and Nick knew these Imo-owned businesses well and likely sensed the opportunity arising from Imo being a forced seller. They definitely could reduce costs and run these businesses better than Imo. Thus, Peacock and Howley raised capital with the help of Kelso & Company for a management-led leveraged buyout. They formed TransDigm, raised the capital, and acquired the aerospace businesses from Imo in September 1993 in a deal valued at $56 million.

Imo’s Aerospace Financials

Below is a snapshot of Imo’s financials from the private placement memorandum in 1993 as TransDigm was raising capital for its $56 million acquisition. TransDigm raised $36 million in debt and $25 million in equity (this totals to $61 million, but the $5 million on top of the $56 million was for commissions to the investment banks helping raise the capital). Total net debt at the end of 1993 was projected to be $34.7 million against $10 million of EBITDA, giving TransDigm a pro-forma leverage ratio of 3.47x.

Below is a chart I put together where you can more visually see the actual results in sales, EBITDA as defined, and EBITDA margins, from 1988 to 1996.

One might look at this and feel a bit disappointed… especially if your only experience with TransDigm has been their extraordinary results as a public company. Declining or flat revenue growth? Who wants that?

On the other hand, one would be be impressed with the high EBITDA margins during the early 1990s, especially given the revenue decline from 1989 to 1993. There are five reasons for the revenue decline during this period:

Defense-related new production programs declined, were completed or were canceled. Remember this time period is after the fall of the Berlin Wall, the disintegration of U.S.S.R., and the end of the Cold War. Defense spending declined and the U.S. government encouraged consolidation within the industry.

Commercial jet transport deliveries peaked in 1991 and declined thereafter.

Commercial aircraft manufacturers reduced their parts inventory in 1991 and kept their levels low.

The military also reduced its spare parts orders in response to budget pressures.

Imo and TransDigm voluntarily reduced its participation in certain lower margin supply orders in the early 90s.

Transition From Kelso to Odyssey

With Kelso as the first backer of TransDigm in 1993, it was just five years later that they flipped TransDigm to its second private equity owner, Odyssey. And it was under Odyssey’s ownership that Doug and Nick got really comfortable with their tri-partite value creation playbook of: (1) value based pricing, (2) generating profitable new business, and (3) continuous productivity and cost improvements.

Nick Howley spoke in 2022 on the 50X podcast about the Odyssey people and how they were helpful in pressing TransDigm to continue to employ their value creation strategy and to pursue more acquisitions (emphasis mine):

Nick: First, the Odyssey guys were good guys to work with too. They’re a little more high strung than the Kelso guys. They’re more of an old line private equity firm. They were great to work with, but Odyssey guys are more high strung. I liked them all.… We continued this very focused value creation concept, because it was just driven deep into the culture, but we started to step up. And this was their, some of it was their pressing, some of it was me, but some was theirs, clearly, the acquisition activity. They were very supportive of that, very helpful at and very much encouraging in it.

The first acquisition under ownership of Odyssey would be Adams Rite Aerospace in April 1999. Adams Rite was yet another aerospace business with a long history. Looking at this 1956 advertisement with the benefit of hindsight from 2025, the level of foreshadowing of TransDigm’s successful business model is off the charts.

The above ad by Adams-Rite in 1956 was an unheralded harbinger of how profitable an aerospace parts businesses could truly be under the right management. Hundreds or thousands of different parts used by every major aircraft company? Highly regulated by the Civil Aeronautics Board and then the Federal Aviation Administration? A business environment where OEMs sought to have the lowest initial purchase price of aircraft and who thought nothing about the extraordinary pricing power available to the aftermarket for replacement parts? And then TransDigm finally comes along in 1999 to acquire Adams-Rite and turbocharge it (and many other businesses over time) with its value creation strategy? Heaven.

It Became Apparent

Nick: I don’t remember … how many businesses we bought, but I would guess on [Odyssey’s] four or five-year hold, we maybe bought eight or nine businesses, something like that. It made me feel quite comfortable with our ability to scale and the fact that our thesis worked.

In other words, we didn’t just by dumb luck hit a place and it worked once. If we stuck with our criteria, which was fairly straightforward—proprietary aerospace businesses with significant aftermarket content, where we could see a clear path to private equity-like return, if the business hit the aerospace aftermarket and proprietary—we could run this play over and over again. During that [time], it started to become apparent to me.

—Nick Howley on the 50X podcast on July 14, 2022, talking about TransDigm under the ownership of Odyssey

It was only under the ownership of Odyssey, when EBITDA margins reached the mid-30s and stayed there. This is also when TransDigm began to make more frequent acquisitions and when the power of the value creation playbook finally became apparent to co-founder Nick Howley. A great part of the power came from its consistent application and running the playbook over and over and over again.

PowerPoint Themes Change, TransDigm Remains the Same

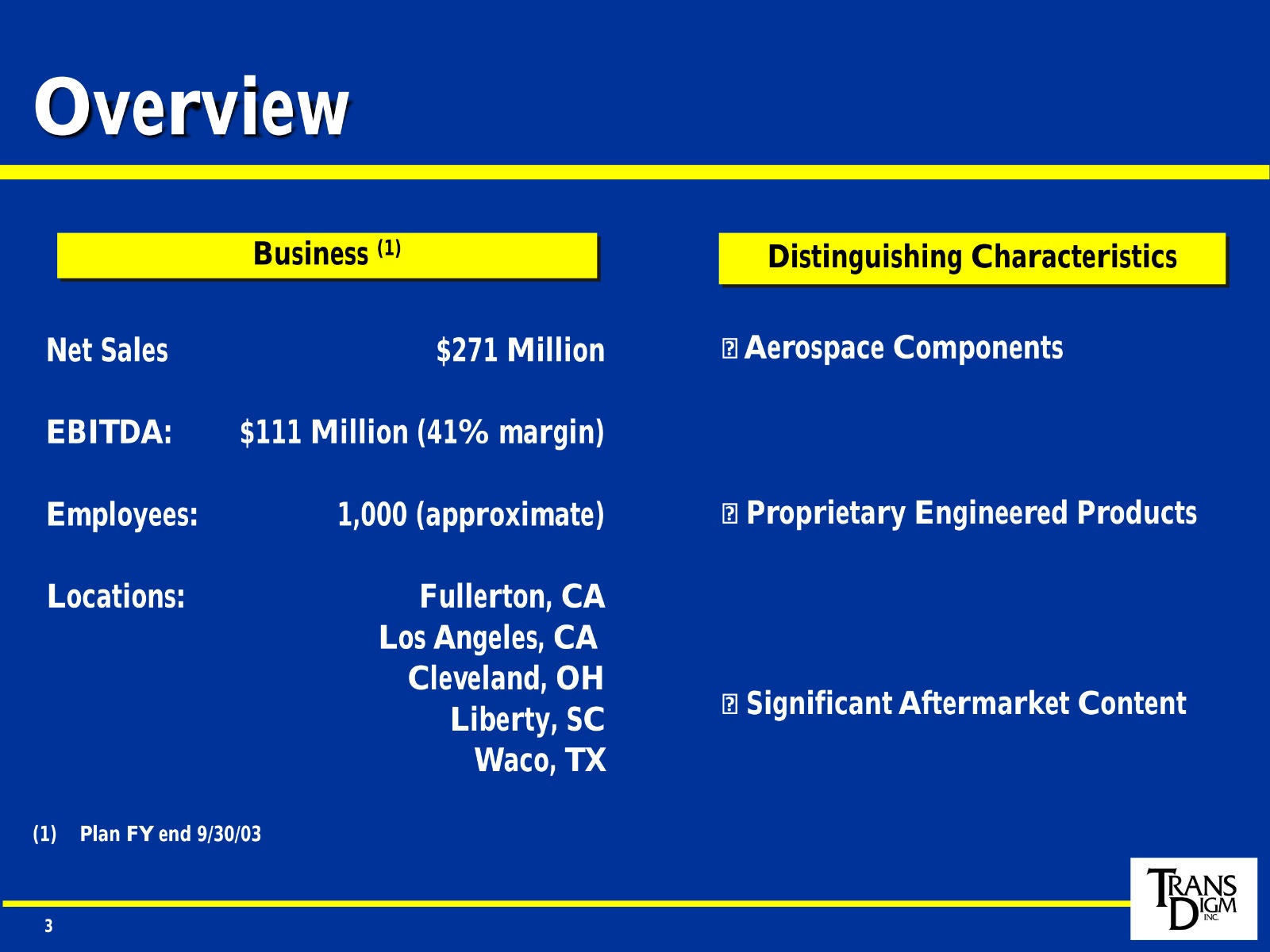

Below we’ll share a few slides that highlights the consistency of the company. First is the overview of the business. Since at least 2003, TransDigm has described its business as one that is focused on proprietary aerospace components with significant aftermarket content.

Twenty one year later, a few more details were been added, but the focus of the business remained the same…

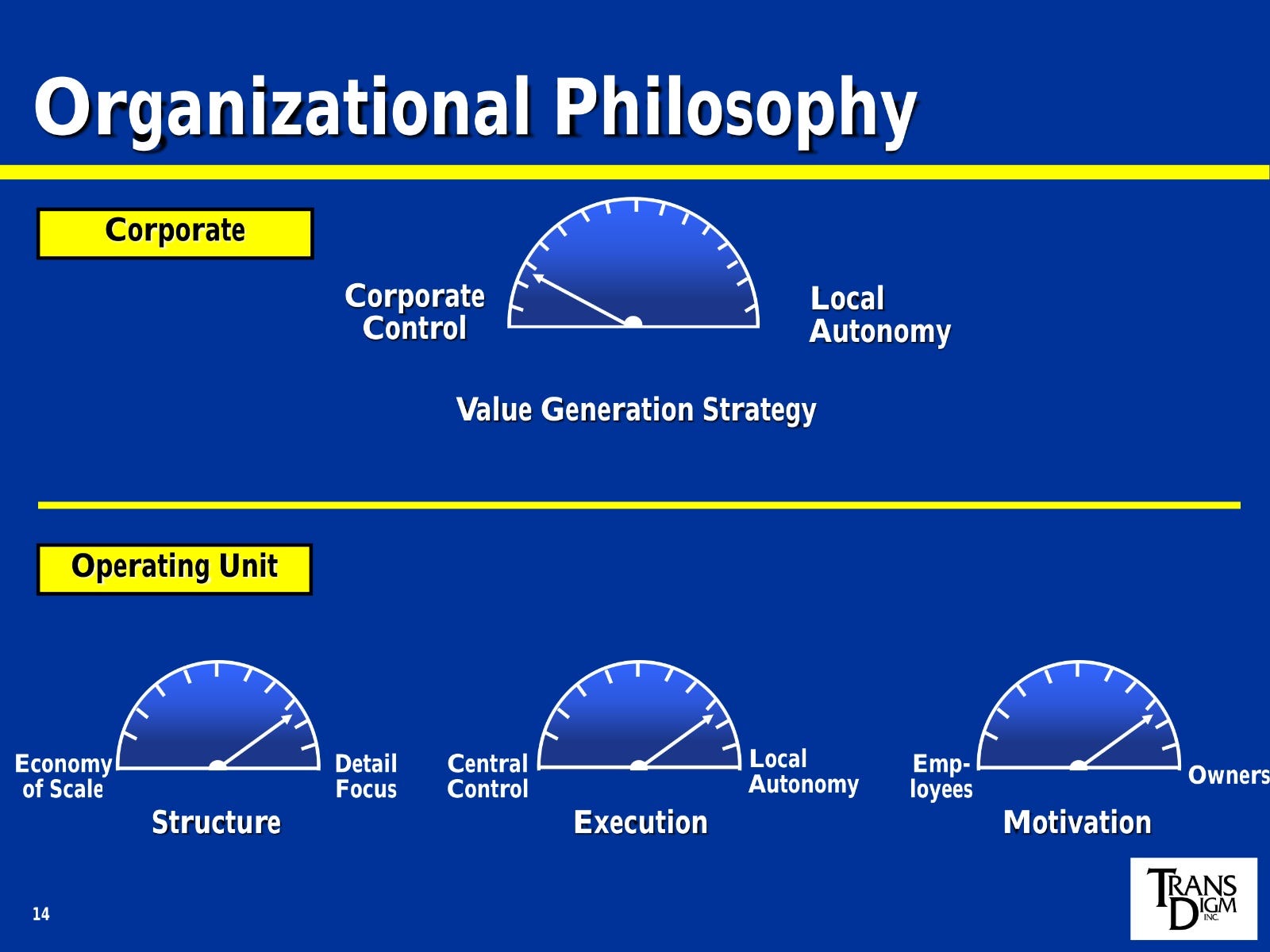

We find another example of consistency in the slides regarding TransDigm’s organizational philosophy from 2003, 2014, and 2024.

Again, what stood out to me from reviewing TransDigm’s history is the remarkable consistency over such a long stretch of time, a rarity in the world of publicly traded companies over any time frame.

Summary

We follow a consistent long-term strategy, specifically. First, we own and operate proprietary aerospace businesses with significant aftermarket content. Second, we utilize a simple, well-proven, value-based operating methodology. Third, we have a decentralized organizational structure and a unique compensation system closely aligned with shareholders. Fourth, we acquire businesses that fit the strategy where we see a clear path to PE-like returns.

—Kevin Stein, TransDigm’s third CEO, May 6, 2025

TransDigm, a manufacturer of aerospace parts, has produced some of the most incredible returns for shareholders since its founding in 1993. After going public in 2006, the company continued to produce private equity-like returns (30% annualized from 2006-2021) with the liquidity of a public company.

Playing in the right industry and consistently applying the right strategy over a long period of time is what has produced these results.

Sources and Further Reading

“Imo Appoints New Chief And Hires a New President”, New York Times, May 6, 1992.

“TransDigm: Foundations with Nick Howley”, 50X podcast, July 14, 2022.

Please Share and Subscribe

If you enjoyed this content, please share and subscribe. Leave a comment as well if you have the time!

Disclaimers for this Substack

The content of this publication is for entertainment and educational purposes only and should not be considered a recommendation to buy or sell any particular security. The opinions expressed herein are those of Douglas Ott in his personal capacity and are subject to change without notice. Consider the investment objectives, risks, and expenses before investing.

Investment strategies managed by Andvari Associates LLC, Doug’s employer, may have a position in the securities or assets discussed in any of its writings. Doug himself may have a position in the securities or assets discussed in any of his writings. Securities mentioned may not be representative of Andvari’s or Doug’s current or future investments. Andvari or Doug may re-evaluate their holdings in any mentioned securities and may buy, sell or cover certain positions without notice.

Data sources for all charts come from SEC filings, Koyfin, and other publicly available information.