The Post-WWII Television Stock Boom

And Correcting Recent Commentary on the Television Fund

David Sarnoff, the President of Radio Corporation of America, in 1930 wrote a full-page article for the New York Times in which he described the various evolutions of “electrical entertainment”. From printing press to phonograph, from radio to movies, and finally to the emergent and amazing potential of television.

At the time of Sarnoff’s article, about 10 million homes in the United States—out of a total of 29.9 million—were equipped with radio sets. But in regards to television, although the technology had been developed in 1927 by Phil Farnsworth, it wasn’t until May 1939 that television sets became commercially available to the public.

But even though TV sets became available just prior to the 40s, adoption of TV sets would be quite slow over the next decade, following the familiar S-curve that depicts Rogers’ theory of diffusion of innovations. One of the barriers to widespread adoption of nearly any technology is the cost and television was no different. RCA’s basic model at that time cost $385 (over $8,600 in 2024 dollars) and their top-of-the-line models more than $2,000. Compare this to the average annual salary in the United States of $1,368 in 1940.

By 1948 there were only 350,000 TV sets in homes. Stated differently, less than one percent of homes in the U.S. had a TV set. But adoption accelerated rapidly from there. The end of World War II was a turning point in consumer adoption. First, manufacturers could shift their focus away from producing war materiel and towards consumer goods. Second, consumers and returning soldiers could finally spend their forced savings on cars, homes, new clothing, and appliances. And TVs.

By 1952, there were over 15.3 million TVs in homes, or about 32% of all homes had a TV.

Prelude to the TV Stock Boom

Below we have some of the largest makers of TV sets in the 40s and 50s in alphabetical order:

Admiral Corp.

Emerson Radio & Phonograph Corp.

Motorola

Philco

Radio Corporation of America (RCA)

All the above manufacturers recognized the enormous potential TV offered for growth in sales and profits. Given that I mostly only have access to Motorola’s historical annual reports, I rely heavily on them.

AVAILABLE FOR DOWNLOAD

If you're really interested, I compiled Motorola's annual reports from 1943 to 2023 in a single zip file for your convenience.

Motorola’s 1947 annual report:

“The sudden increase in popularity of television during 1947 has been the most exciting event in the history of the radio industry. Television has moved rapidly in the past year and is now making great strides towards fulfilling its destiny as one of the most important factors in the entertainment, advertising and merchandising fields.…

Prospects of Motorola for 1948 are unusually bright in the field of television. Your Company made its entry in 1947 with a new and different type of television receiver which met immediately with enthusiastic acceptance. Prestige has been established, and your Company is now endeavoring to fill a substantial backlog of orders. Plans and preparation for following up this auspicious beginning have been made, and the future for Motorola in television is undoubtedly optimistic.”

The New York Times wrote about Motorola’s new television set on November 18, 1947: “Deliveries of the new Motorola table model television set, which lists at $179.95, began here today…. The receiver has a seven-inch direct view tube, weighs only twenty-six-and-a-half pounds and has facilities for reception of all thirteen television channels.”

The NYT wrote again about another new Motorola model on September 9, 1948: “The first new television receiver is a table model with a ten-inch direct-view cathode ray viewing tube and will list at $298.95. Mr. Cooper said that it was the lowest-priced ten-inch model market by any major manufacturer.”

From 7 inches to 10 inches in size in just a year!

In Motorola’s 1948 annual report, management comments on the fast growing market and says they essentially underestimated its growth:

“The importance and size of the television industry at the year end far surpassed expectations of a year ago. Sixteen stations located in eleven cities were in operation at the end of 1948. On January 1 of this year, there were fifty-one stations in twenty-nine cities on the air, with networks in the East and Mid-West. New advertisers quick to recognize the advantages of this new merchandising medium rapidly improved the quality of programs as larger viewing audiences were assured. Industry production of television sets approximated 900,000 during 1948, with production rale at the end of the year reaching well above that level. Hindering production throughout the year, the shortage of cathode ray picture tubes became more acute as manufacturing levels increased in the latter part of the year. The Company’s 1948 production exceeded 100,000 units with a dollar value of approximately $15,000,000.”

The company further noted that the potential for future growth was significant and becoming clearer. “Within a 40 mile radius of stations presently operating, is a potential viewing audience of more than seventeen and a half million families.” As more stations opened over the years, the total addressable would increase further.

Manufacturers would begin to expand their manufacturing capacity. The New York Times reported on July 11, 1949, on Motorola beginning construction on new facilities that would increase its television set production by 40% (emphasis mine):

“The new addition has a 600-foot conveyor lined scheduled to produce more than 500 television receivers per eight-hour day. The company expects to produce 250,000 television sets this year. The addition was made necessary by the production of a complete new line of television receivers to be introduced in the fall and the fact that sales of receivers during the first quarter of 1949 were three times greater than sales in the corresponding period of 1948.”

Demand for TV was robust, to say the least. The number of Motorola TV sets purchased in 1949 for 1950 delivery rose 115% over the same period the prior year. And the market continued to go gangbusters. NYT reported on October 12, 1949, “Dollar volume sales of its 1950 line of television receivers were up 424 per cent during September compared with a year ago…” (emphasis mine).

And then Motorola decided to expand its plant yet again in December 1949. They set out to double the capacity of its plant in Quincy, IL.

Video Issues Skyrocket

With TVs finally within reach of tens of millions of Americans, any publicly traded company that had an association with this new growth business easily caught the attention of the investing public. Share prices of “video issues” were going to the moon, to use the recent parlance of r/wallstreetbets.

The New York Times reported on April 15, 1950:

“Television issues skyrocketed yesterday on the stock market in the wildest dealings yet seen in securities of the nation’s newest industry. Despite the activity and unusual strength in the TV division, the rest of the list was dull and made a poor showing against the day’s leaders.…

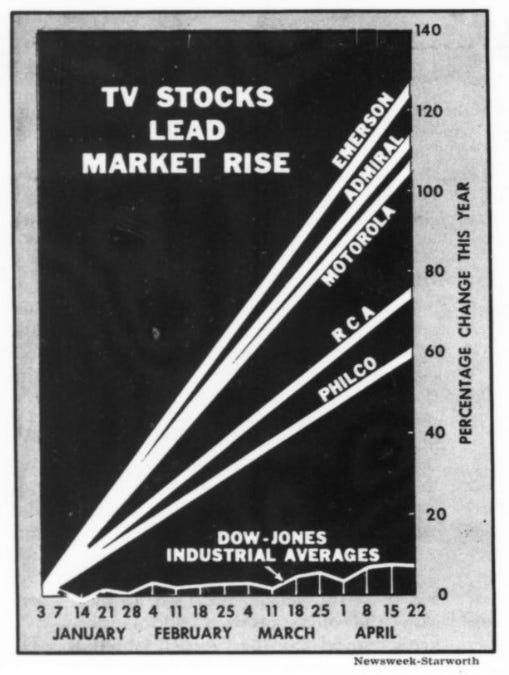

The almost-complete switch to the TV issues put them in the majority among the fifteen most active stocks. Radio Corporation, which led in business on 180,700 shares, rose 1¼ points to 21.… Motorola climbed 8⅜ to 50⅛, Magnavox 20⅜ to 20¼, Zenith 3½ to 70, Admiral 3⅜ to 38, Emerson 3¼ to 32 and Philco 3½ points to 49¾.”

Newsweek a few weeks later wrote about “the television boom” on May 1, 1950:

A wealthy Staten Island importer-exporter, after seeing television in bars, decided it was just a gadget. His wife, against his advice, bought a set. The businessman liked it and promptly bought 1,000 shares of RCA stock as an investment. This investor is typical, according to a partner in a large Wall Street brokerage house.

Since last July the price of television stocks has doubled. ‘The public has gone mad,’ one Wall Streeter said. Last week the stocks of seven leading set manufacturers accounted for nearly a tenth of the total volume of the New York Stock Exchange. Old-timers in the Street couldn’t remember anything like it since the radio boom of the ‘20s or the airline-share boom just after the war

Unlike the airline flurry, the TV industry had some solid statistics behind it. The number of sets turned out jumped from around 900,000 in 1948 to 2,600,000 last year. This year the industry confidently expects to turn out 5,000,000, nearly twice as many. Guesses beyond 1950 are even more optimistic.”

The level of actual growth and unbridled optimism could be seen in the enormous increases in share price for five of the leading TV companies. Emerson, Admiral, and Motorola had more than doubled in the first four months of 1950. RCA was up nearly 80% and Philco up 60%.

It’s hard not to think of the share prices of any company related to AI this year. From chipmaker NVIDIA, to power generation companies (Vistra, Constellation Energy), to the companies providing the building blocks of data centers (Vertiv and Emcor). The share performances of these businesses have far outperformed the market thus far in 2024.

Making Hay While the Sun Shines

In typical fashion, opportunistic buyside funds and sell side stock brokers piled into the TV trade, which brings us to an interesting article by James Mackintosh of the Wall Street Journal. Published on September 1, 2024, its titled “How to Lose Money on the World’s Most Popular Investment Theme”. And one of the theme funds Mackintosh highlighted was the Television Fund which got its start in the late 1940s. He uses the Fund as one of the earliest examples of a fund trying to capitalize on a specific industry theme.

Television Fund

The Television Fund was an open-end mutual fund that sold its first shares to the public in September of 1948. Given the optimism of the investing public about the field of TV, radio, and electronics, the Fund was able to sell shares at a premium to net asset value. The first offering was at $9.81 compared to a net asset value of $9 per share. Total assets of the Fund passed reached $55 million on Nov. 1, 1954, and then reached $100 million in April of 1955. The net asset value would reach $11.33 per share in June 1955.

Good performance continued. At July 31, 1957, the Fund reported assets reaching $156.7 million and net assets per share reaching $12.49.

Getting back to Mackintosh’s piece in the WSJ, he suggests that good long term performance from theme funds are hard to obtain. The three reasons are:

Defining a theme is hard and is also subject to change over the life of a fund;

Timing the theme is harder; and

Long-term investing in a theme fund is really hard.

Generally, these are all good reasons to be wary of theme funds. Most funds or investment products with a theme rarely performs well over the long term. The odds are stacked against investors earning a decent return when they choose to invest in themes. Recently hot industries or investment products designed to take advantage of psychological/emotional/political biases of investors should all be approached with heavy skepticism.

However, Mackintosh is both right and wrong on the Television Fund’s performance. Below is his chart of the performance of the Television Fund—now named the DWS Science and Technology Fund—compared to two different indexes going back to the beginning of 1973. Over this time period, the Television Fund noticeably underperformed.

However, if Mackintosh had dug deeper he would have learned the Television Fund actually outperformed many of the other longest-lived funds that still exist today, none of which have any specific theme (industry or otherwise). These include the Pioneer Fund, started February 13, 1928, by Phil Carret, and the Fidelity Fund, started on April 30, 1930, by Edward Johnson.

DWS on their website shows the annualized performance of the originally named Television Fund from inception in 9/7/1948 through 08/31/2024 as 11.97%, an exceptional long term track record. Below, I compare this to the returns of the Pioneer Fund, Fidelity Fund, Massachusetts Investor Trust, and Vanguard’s Wellington Fund.

Even thought the Television Fund might be an exception over the very long term, Mackintosh’s advice still stands. Investors must always be wary of investing in recently hot sectors and faddish “opportunities”.

TV Company Performance 1949–1956

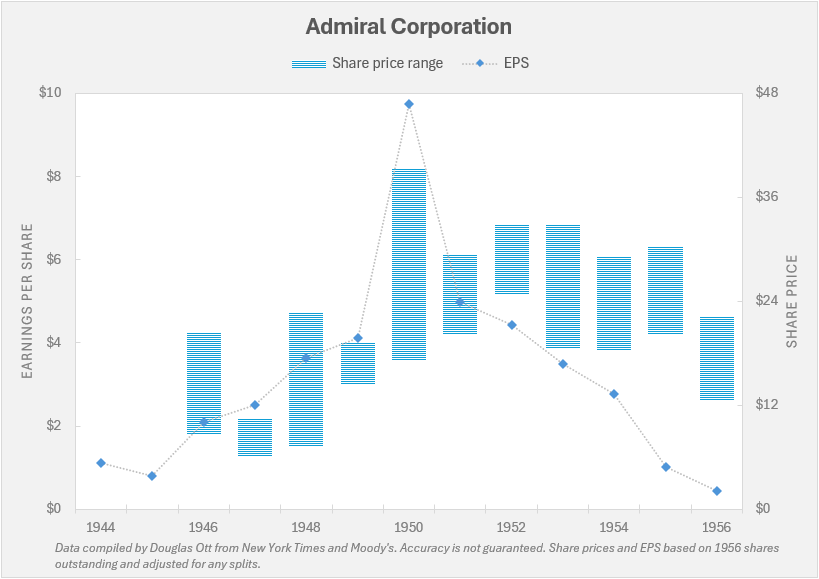

Let’s get back to the five companies mentioned in the 1950 Newsweek article. All experienced an extraordinary increase in demand for TVs after the end of WWII. All would perform more or less in line with each other in 1949 and 1950, both in terms of sales and earnings increases. However, by 1956, the share prices of all except Motorola and RCA fell back down to 1949 levels, erasing all gains from the superlative year of 1950.

Admiral Corporation

Emerson Radio & Phonograph

Motorola

Philco

RCA

Key Takeaways

It can take years or decades before a new technology is ready to be widely adopted.

Although television was identified early on by Sarnoff of RCA as a technology with revolutionary potential, it would take nearly two decades before it was within the budgets of the average household. And then we saw revenues of the manufacturers of the new technology doubling in three or four years. Motorola had revenues of $82 million in 1949 which grew to $169 million in 1952. RCA had revenues of $396 million in 1949 which grew to $849 million in 1953.

Stock picking is always hard.

A few years after the end of World War II, the TV manufacturing industry boomed in the U.S. and share prices of businesses associated with the industry skyrocketed in 1950. But share prices of some companies plummeted back to earth several years later, wiping out all the prior fast gains.

One must always be cautious of riding a hot sector. Trying to time when to get in and get out is always a fool’s game. It’s best to find the best companies regardless of industry, purchase at an appropriate price, and hold on for decades.

Volatility and long periods of underperformance are inevitable with theme funds.

Started in 1949, the Television Fund was one of the first funds with a theme hoping to take advantage of the boom in TVs and electronics. It did quite well in growing assets under management as well as growing net asset value per share. Then the 1970s rolled around and the fund started to underperform its benchmark by a significant amount. On the other hand, the shareholders that got in early with the fund did quite well over the next 76 years. The reality one must accept is that markets go up over the very long term and various industries become expensive and cheap and various fund managers will outperform and then underperform.

The best thing to do in almost all cases, whether as an individual shareholder or as a client of an investment advisor, is to sit as still as possible and let the power of long term compounding work its magic.

Please Subscribe

If you enjoyed this content, please share and subscribe.

Sources and Further Reading

Mackintosh, James. “How to Lose Money on the World’s Most Popular Investment Theme”, September 1, 2024, Wall Street Journal.

Sarnoff, David. “In Television Sarnoff Sees a New Culture”, July 13, 1930, New York Times.

Taylor, Bryan. “RCA and the Roaring Twenties”, Global Financial Data, November 13, 2023.

Disclaimers

The content of this publication is for entertainment and educational purposes only and should not be considered a recommendation to buy or sell any particular security. The opinions expressed herein are those of Douglas Ott in his personal capacity and are subject to change without notice. Consider the investment objectives, risks, and expenses before investing.

Investment strategies managed by Andvari Associates LLC, Doug’s employer, may have a position in the securities or assets discussed in any of its writings. Doug himself may have a position in the securities or assets discussed in any of his writings. Securities mentioned may not be representative of Andvari's or Doug’s current or future investments. Andvari or Doug may re-evaluate their holdings in any mentioned securities and may buy, sell or cover certain positions without notice.

Data sources for all charts come from SEC filings, Koyfin, and other publicly available information.