The Long Road From Metro-Tel to EVI Industries

Back in 2015, a shareholder with a long-term vision began to acquire a controlling stake in a tiny company. The market cap was less than $40 million and it was in the business of distributing parts and equipment to owners of commercial and industrial laundry machines and dry cleaners. Five years later, this shareholder was now CEO and Chairman, had successfully started the company down the path of rolling up its industry, and the company had been renamed from EnviroStar to EVI Industries. The share price had also gone up 10x in just four years.

But this is just the latest chapter of the corporate history of EVI. The story actually begins in 1950 with the founding of Metropolitan Telephone Supply Corp. by Sheppard Beidler.

Metropolitan Telephone Supply Corp.

Sheppard Beidler, an entrepreneurial electrical engineer, founded Metropolitan Telephone Supply Corp. on June 20, 1950 in New York. The name would later change to Metropolitan Telecommunications Corp. By 1960, Metro was assembling communications equipment, transformers, filters, relays, disc capacitors, RF coils and other electronic components primarily from materials made by others. Its unclear when Metro went public, but it must have been in the mid- to late-1950s as that is the earliest financial data I can find in my 1962 Moody’s Manual. The snapshot below shows Metro’s financials from 1957 to 1961 which excludes the financials of Grow Solvent which they later acquired in 1961.

Beidler’s next most significant decision as founder of Metro was hiring a young 42-year-old by the name of Russell Banks in 1961 to help grow the business at a faster pace. Banks decided that the paint and coatings industry would be the vehicle for the company’s future growth.

Grow Group Inc.

We see in the below snippet from SEC News Digest on September 18, 1961, that Metro had filed a statement seeking registration of 240,000 shares of common stock in connection with their impending acquisition of Grow Solvent Co., Inc., a company that made lacquer thinners, petroleum solvents and specialty chemicals.

Thus, soon after Banks’ hiring, Metro acquired Grow Solvent Co. in November 1961. The purchase price for Grow Solvent was $2,783,333 million in cash and Metro shares worth $216,667 (32,500 shares). Furthermore, given that Grow Solvent revenues would make up two thirds of total revenues, they renamed the parent company to “Grow Corp.” and renamed its electric assembly business “Electric Systems, Inc.” It was just another two years later when Grow Corp. spun off Electric Systems, Inc. on June 28, 1963 to the public under the “new” name of “Metro-Tel Corporation”. Biedler went with Metro-Tel but remained a director at Grow until 1993.

Banks stayed on with Grow Corp.—later renamed Grow Chemical Corp. in 1964 and renamed again to Group Group Inc.—and continued to grow the business organically and via acquisition. Banks led the company until 1995 when the UK’s ICI bought Grow Group for $350 million, outbidding Sherwin-Williams.

Metro-Tel in the 1990s

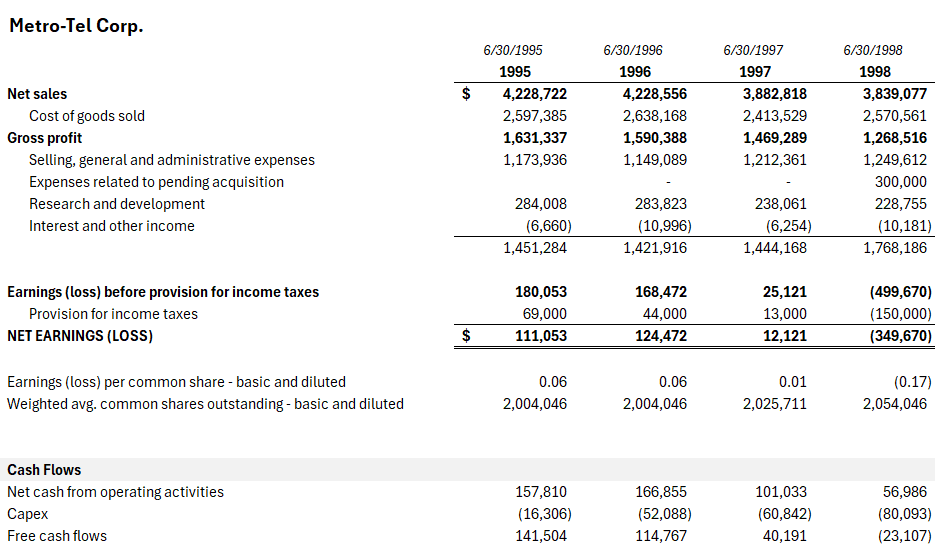

Let’s now go back to Metro-Tel. In the 1990s, Metro-Tel was engaged in the manufacture and sale of telephone test and customer premise equipment utilized by telephone and interconnect companies in the installation and maintenance of telephone equipment. However, the business had not grown much at all. Metro-Tel had sales of $2.3 million in 1960 which had grown to $4.2 million of sales in 1995. That’s a CAGR of just 1.8% over those 35 years—most certainly far below the rate of inflation over that time.

More seriously, and in spite of the ongoing tech and telecom boom, Metro-Tel revenues had shrunk from 1995 to 1998 while free cash flows had declined even faster. Metro-Tel explained these poor results in a September 1998 SEC filing:

“The downsizing of the Regional Bell Operating Companies (“RBOCs”) during the past several years has reduced the number of Telecom craft personnel who are potential users of the Company’s test equipment and, accordingly, the Company’s sales. To reduce the impact that has occurred as a result of the downsizing of the RBOCs, through research and development, the Company has begun introducing new products aimed at reducing its dependence on the RBOCs and is entering into new markets, principally the public utility and data industry, for its existing and new products.”

In the same SEC filing, the company also reported details on a proposed reverse merger with Steiner-Atlantic Corp. This transaction was truly a head-scratcher as Steiner-Atlantic was a privately held Florida company in the business of distributing dry cleaning equipment, industrial laundry equipment and steam boilers. Perhaps it was further evidence of the dim prospects of the core Metro-Tel business.

Background on Steiner-Atlantic...

The following is from Metro-Tel’s 10-K filing in 2000:

Steiner was founded in 1960 by William K. Steiner, initially operating as a distributor of dry cleaning systems and boilers, and as a rebuilder of laundry, dry cleaning and boiler equipment. Steiner expanded in 1972, when it began distributing institutional laundry equipment to hotels, motels and hospitals. In 1980, Steiner began importing dry cleaning systems from an English manufacturer and, four years later, Steiner replaced this manufacturer with a relationship with an Italian manufacturer of dry cleaning systems. In 1990, Steiner established its own branded product line with the introduction of an updated dry cleaning system under the Aero-Tech label, substantially all of which is currently manufactured exclusively for Steiner in Italy. In fiscal 2000, Steiner's Aero-Tech division entered into a license agreement with Green Earth Solutions to use the Great Earth cleaning system in Steiner's Green Jet(TM) dry cleaning machines.Whatever the actual reason for the merger might have been, it seems the two parties each got something they likely wanted. Metro-Tel had a second business with likely better prospects and the owners of Steiner-Atlantic now had the benefit of their business being publicly traded.

The two parties signed an agreement on July 6, 1998, and the two businesses merged on November 1, 1998. Steiner’s shareholders would own 69% of the newly combined company and the old Metro-Tel shareholders would own 30%. The remaining 1% of shares were reserved for the investment bankers as compensation for their services in the transaction.

The share price of the company responded positively from late 1998 to early 2000. However, it could not escape the bursting of the tech bubble. Annual revenues declined from $20 million at the end of calendar year 2000 to $12.2 million to $12.2 million for the trailing twelve months at March 31, 2002. The share price followed suit and fell to an all-time low in 2003. It also probably didn’t help that the shares were now trading over the counter. This is because after the merger with Steiner, the company no longer met the NASDAQ listing criteria, and voila, it was delisted after the merger.

Metro-Tel ➡️ DRYCLEAN USA ➡️ EnviroStar

After the acquisition of certain assets of DRYCLEAN USA Franchise Company in July 1999, Metro-Tel changed its name to DRYCLEAN USA, Inc. in November 1999. At the time, DRYCLEAN USA was one of the largest franchise and license operations in the dry cleaning industry, with over 400 franchised and licensed locations in the United States, the Caribbean and Latin America. After the acquisition of DRYCLEAN, the goal was to increase the number of franchisees and licensees.

The next corporate event was the sale of the Metro-Tel business on July 31, 2002. The sale price was a measly $800,000, of which $250,000 was paid in cash and the remainder was financed via the purchaser’s promissory note. We now have a pure-play distributor of commercial and industrial dry cleaning equipment with a market cap of less than $5 million… Oh what fun!

Business did pick up from 2002 to 2006. Revenues increased from $14.3 million to $20.4 million. The market cap increased to a little over $21 million at its next peak in early 2005, but it then stalled out and slowly declined to $6 million at the depths of the Great Financial Crisis in 2009. The company also changed its name, yet again, in during its FY2010 to EnviroStar, Inc. The reason for the change was ostensibly to “emphasize the Company’s green environmentally safe products.”

Business slowly picks up from 2009 through 2012. And then we have the banner year of 2013. During FY2013, EnviroStar’s total revenues grew 61.3%, increasing from $22.5 million to $36.2 million. Equipment sales grew 90.1% while spare parts sales growth of 5.4%. Incredibly, acquisitions were not a part of this growth. It just seems that EnviroStar’s customers had reached the point where they could no longer delay equipment upgrades and the economy was now safely past the depths of the financial crisis.

Henry Nahmad, Nephew of Watsco’s Founder Albert Nahmad

The next chapter in this story begins in 2015 when Henry Nahmad acquires a 40% stake in EnviroStar. A few years later, Nahmad gains control of over 50% of the company and is appointed Chairman and CEO. From there, Nahmad begins to implement the “buy and build” strategy to grow EnviroStar and consolidate its market. He would change EnviroStar’s name in 2018 to EVI Industries.

There are two important things to know about Henry Nahmad.

One: he is a nephew to Albert Nahmad, the founder of HVAC distributor Watsco (WSO). Albert used his own “buy and build” strategy with Watsco in 1972 and subsequently generated over a 100x return for shareholders since then. If genes can’t transmit shareholder returns, then the next best thing is having a leader who has learned from, and has support from, one of the best.

Two: Henry does have actual experience doing this. He worked at Watsco from 2001 to 2009, eventually becoming their head of M&A.

EVI’s Strategy

Henry Nahmad outlined the long-term strategy guiding EVI in 2019:

Before we get started, you should know four things: one, we are focused and committed to long-term growth; two, the foundation of our company is our entrepreneurial culture; three, we are aggressive in our pursuit of growth yet conservative in our plans to finance it; and four, we are deeply invested in EVI, meaning that 70% of EVI is owned by EVI executives and the original owners of our acquired businesses. With that, let us begin by sharing with you our long-term growth strategy. What is EVI's buy-and-build growth strategy?

Candidly, buying and building businesses is not an original idea. But what makes EVI different is the way we execute both buying and building, the EVI way, which requires a long-term perspective and is conducive to achieving significant shareholder value creation over the long term. The “buy” component of our strategy includes the pursuit of acquisitions … that complement our existing businesses or that might otherwise offer growth opportunities for our company. We are disciplined and conservative in our consideration of acquisitions, and we generally seek to identify opportunities that fit certain financial and strategic criteria. The “build” component of our strategy principally involves encouraging growth at our acquired businesses by adding products, hiring sales professionals, expanding service operations implementing scalable technologies and promoting the exchange of ideas and business concepts between the management teams of our businesses. Our acquired businesses have access to the full extent of our capital resources, functional support specialists and established vendor relationships … from which to achieve growth and increase profitability.

—Henry Nahmad, Chairman and CEO of EVI Industries, September 12, 2019

Petering Out

After the share price of EVI went on an amazing run from $2 per share in 2015 to $45 per share in 2018, the valuation multiple has spent the last 7-8 years letting off steam. The EV/EBITDA multiple reached 70x in December 2018 and is now down to 9.3x. Furthermore, EVI completed its largest acquisition yet (of Girbau North America) this past April, to which there was barely any reaction by the market. EVI paid $43 million for Girbau, a company which had $75 million of revenues and an EBIT margin of 9.5% in 2024.

The low EV/EBITDA multiple and the market’s lack of reaction after the Girbau acquisition are the two reasons why I am now very interested in this business after following it over the last decade.

Further Exploration

We’ve seen incredible financial results since 2016 with a new, driven leader at EVI implementing a “buy and build” strategy to grow the company and create shareholder value over the long-term. Although EVI has taken on debt and issued shares to fund its acquisition program, the trade-off has been worth it.

From 2016 to 2024, shares outstanding have increased 88%. In exchange for this dilution, EVI has increased per share results by multiples of that: revenue per share increased 422%, gross profits per share increased 582%, EBIT per share increased 122%, and free cash flow per share by 927%.

However, there must be further exploration and due diligence. Here are some of the questions I have (and please let me know in the comments if there are other aspects I should be exploring):

Gross margins have expanded since 2016 while EBIT margins have declined? What gives?

Given that EBIT margins have declined over time, is there any operating leverage in this business? What can we expect from operating margins going forward? Why would margins stay the same? Why might they increase?

Is there a reasonable case for EVI to target other related industry verticals or product lines for M&A?

What are the competitive dynamics in this business? Do manufacturers of the equipment control the majority of distribution? How much room is there for independent distributors to take on this role from manufacturers?

Summary

The long history of Micro-Tel offers two important lessons:

A business can exist for an extraordinarily long time even despite below-average results. Founded in the 1950s, Micro-Tel grew revenues at less than the rate of inflation over the next fifty years. Then it was eventually sold for just $800,000 in 2002, a purchase price that was less than its annual revenues during 1956! The opportunity for more robust growth was undoubtedly present between 1950 and 2000, but management never seized it.

Even with the starting point of a no-growth or money-losing business, it can still be an opportunity for someone else. Whether its a cash shell with significant NOLs, or a tiny publicly-traded company whose primary use is in a reverse merger by which a a larger and more viable private business can go public, these situations can be the catalyst for extreme value creation when more driven business people arrive at the scene.

Getting back to modern times… the situation with EVI in 2015 was unique when Henry Nahmad got involved. By 2020, the situation became unattractive as the market assigned an unrealistic multiple to the share price. Now, with the benefit of many years of multiple compression, things are interesting yet again, especially with EVI having recently closed on its largest acquisition yet.

If you’re an individual investor with a personal account and the temperament to own an illiquid stock for the long-term, I think it’s time to sharpen your pencils.

Please Share and Subscribe

If you enjoyed this content, please share and subscribe. Leave a comment as well if you have the time!

Sources and Further Reading

Metro-Tel

Obituary of Sheppard Beidler, New York Times, May 29, 1995.

Grow Group

“Institutions Vex Company Head”, New York Times, Nov. 4, 1972

Paul, Ronald N. The 101 Best Performing Companies in America. Chicago, Ill. : Probus Pub. Co. 1986.

“Sheppard Beidler, An Executive, 76”, New York Times, May 29, 1995.

DRYCLEAN USA / EVI Industries

“Steiner-Atlantic Celebrates 50th Anniversary”, Textile Care Allied Trades Association, 2009.

Obituary of William Kalman “Bill” Steiner, December 27, 2012.

“EnviroStar: History Doesn’t Repeat Itself, But it Often Rhymes”, ADW Capital Management, October 2018.

Value Investors Club, shorting EVI Industries, published February 28, 2019.

Disclaimers for this Substack

The content of this publication is for entertainment and educational purposes only and should not be considered a recommendation to buy or sell any particular security. The opinions expressed herein are those of Douglas Ott in his personal capacity and are subject to change without notice. Consider the investment objectives, risks, and expenses before investing.

Investment strategies managed by Andvari Associates LLC, Doug’s employer, may have a position in the securities or assets discussed in any of its writings. Doug himself may have a position in the securities or assets discussed in any of his writings. Securities mentioned may not be representative of Andvari’s or Doug’s current or future investments. Andvari or Doug may re-evaluate their holdings in any mentioned securities and may buy, sell or cover certain positions without notice.

Data sources for all charts come from SEC filings, Koyfin, and other publicly available information.

What you say is reasonable. He's definitely the key person behind the whole operation. So you could be right. But there's a slight possibility that the controlling shareholder could be using the company as his personal ATM. Maybe I'm being unfair.

To me, Nahmad's compensation package of $6m (including stock awards) in the context of the company's net income of $5.6m explains a good part of the low EV/EBITDA multiple and the market’s lack of reaction after the Girbau acquisition.

Incidentally, thank you for your thoughtful and interesting posts.