“I don’t really have any new color to add on my confidence in new construction. There’s just so many factors at play, everything we discussed and then lay on top of that, the macro and how people are feeling about their disposable income, discretionary income, 401(k) values and then, of course, interest rates on those pools that will require some financing.”

—Peter Arvan, CEO of Pool Corp, April 24, 2025

Although Pool Corp management recently modified the design of their quarterly earnings presentations, I’m sure they wish they could have modified the results they’ve been presenting over the last two years.

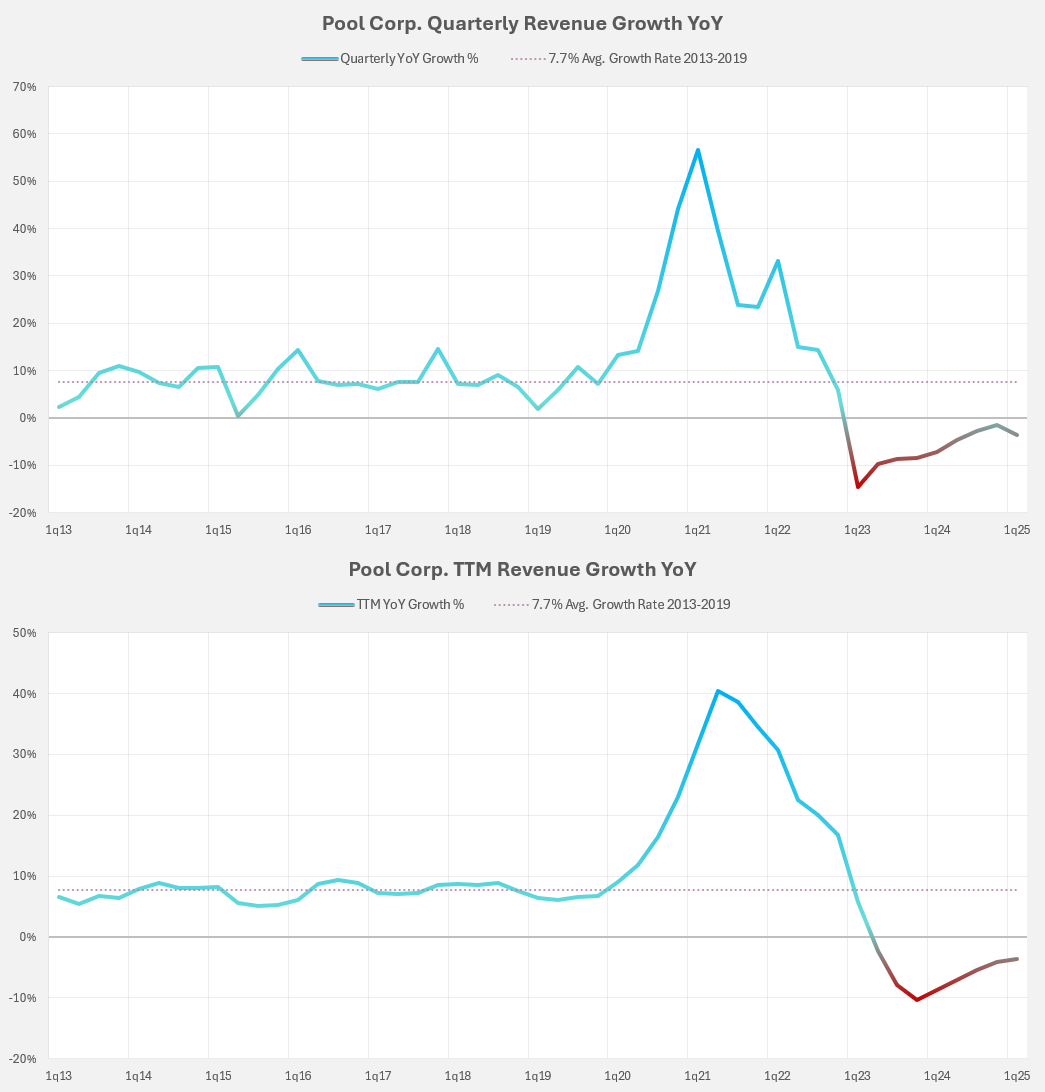

For its 1Q 2025 results, Pool Corp turned in yet another quarter of negative revenue growth: down 4.4% compared to the first quarter of last year. The company has now suffered nine quarters in a row of year-over-year revenue declines, both on a quarterly and a trailing-twelve month (TTM) basis.

From my perspective, the story remains pretty much the same. This company continues to suffer from a COVID hangover where an enormous amount of demand was pulled forward in a brief two year period from 2020 to 2022. One can see from the charts above the enormous divergence the company experienced from its stable average revenue growth of about 7.7% per year. The fact that a pool supply distributor—operating in an industry that sees growth of just 4%-6% annually—experienced 50%+ revenue growth in any year (without an acquisition) is just bonkers. This likely will never be repeated in anyone’s lifetime going forward.

A New Narrative Appears!

Although last year I thought the effects of COVID on supply/demand dynamics would be starting to reverse at this point, there is now a new and overlapping narrative for Pool’s near-term prospects. Management provided color on the new reasons for subdued growth in their recent call.

First are the idiosyncrasies of regional dynamics. In Texas, one of Pool’s top states, revenues were down 11% while revenues in the other top states of Florida, California and Arizona, were essentially flat. Management had no explanation for poor performance in Texas aside from bad weather, interest rates, and economic fears contributing to less new builds than expected. Revenues from maintenance products remain stable in Texas and are not a concern for Pool Corp.

Regarding Florida, although revenues were down 1% this quarter, it remains the best state for Pool:

“Florida is performing well. Florida is an amazing market for us, and Florida is performing well…. I don’t really have any new color to add on my confidence in new construction. There’s just so many factors at play, everything we discussed and then lay on top of that, the macro and how people are feeling about their disposable income, discretionary income, 401(k) values and then, of course, interest rates on those pools that will require some financing.”

—Peter Arvan, CEO of Pool Corp, April 24, 2025

The second reason for continued soft performance across the board is again the combo of interest rates and new pool costs that are far higher than in recent memory. These directly diminish the willingness of consumers to pursue new construction or remodeling of pools.

Finally, there are the recent policies of the U.S. government that are increasing hesitancy of consumers. Tariffs are already increasing the total cost of constructing or remodeling pools. Tariffs are certainly inducing a recent bout of volatility in the markets. Given the boomer demographics of Pool’s ultimate end customer, more volatile investment portfolios are understandably preventing future pool owners from pulling the trigger on an expensive project.

Passing on Rising Costs

Pool Corp, as one of the largest distributors in the U.S. that leads with their value proposition to professional builders and servicers of pools, is in a good position to pass on all price increases from their suppliers that might result from inflation or tariffs.

First, 84% of their total revenues come from products and supplies that are non-discretionary. Homeowners must maintain their pools and replace broken equipment. If they don’t, bad things will happen. Second, when someone wants to build or remodel a pool, the price of materials is not a roadblock because it is the labor that is the much larger cost. Pool Corp estimates that materials make up about 25% of the costs of a pool.

Here’s what CEO Peter Arvan said in 2022 about material costs (emphasis mine):

If you have a pump, are our variable speed pumps now more than they were a couple of years ago? You bet. But if the water stops moving in your pool, you don’t have a choice to say, well, wow, that pump is an extra $200 now; I don’t want to buy it. You have no choice. You have to replace that pump. Because unless you have that water moving, it’s going to turn green. And then you’re going to end up with mosquitoes and frogs and an unsightly mess in your yard.

And let’s face it, you’re using a pool every day whether you’re in it or not, right? Whether you’re in it or not, you’re using that pool because it’s part of your yard. It’s part of your landscape. So you have to maintain that pool. You have to maintain that pool. And … on the material side, when you consider that on the price of a pool, material makes up 25%. The vast majority of that is labor.

So even with the increase on the cost of the material that we would sell, that’s not the deterrent that says, ‘Hey, you know what? I’m not going to do that project.’ So inflation is real.… We all feel it as consumers. We see it as the bridge between the suppliers and our customers and how that … flows all the way through.

However, we’ve been fortunate that it passes through the channel. So it’s not materially affected demand.

—Peter Arvan, CEO of Pool Corp, March 8, 2022

And on the recent quarterly call, Arvan provided more details on the cost breakdown of a pool and why he thinks higher material prices are not the primary factor in a decision to build a new pool:

“I think that the price increases … [are] going to pass through the market because, again, the vast majority of that product is sold for maintenance and repair, nondiscretionary, the pumps stop working, the filter is leaking, the heater is leaking, I have to replace that, I can’t operate the pool without it. So I think that’s one way to think about it. And then in terms of an overall pool project, given the escalating cost of a pool and an in-ground pool $80,000 to $100,000 depending on where you are now on the type of pool that you build, if you told me that the equipment and the equipment pad is, let’s call it, $15,000, if you told me that it was going to be 3% higher, I don’t know that, that’s going to cause people to say, okay, 3% of the $15,000 is up, so I’m out.

So I don’t really think it’s going to have a material demand destruction impact on the new pool construction. What I do think people look at is the overall market. So if … tariffs were to get worse and 401(k)s and equity values would continue to drop, I think that’s far more meaningful to new pool construction than a 3% increase.”

—Peter Arvan, CEO of Pool Corp, April 24, 2025

Pool Corp remains well positioned to pass on price increases to its customers. In fact, since their 4Q 2024 earnings call, Pool Corp’s largest equipment vendors implemented in-season price increases that ranged from 3%-4% that took effect in April to address the March tariff announcements. Pool increased their selling prices accordingly. Additionally, last Tuesday, Pentair announced 4% price increases for their pool-related products. Pool Corp will be raising prices for these products as well.

Getting Back to Growth

Pushing on a String

Taking a step back from the recent results, I want to reemphasize why Pool Corp has had a long string of negative quarterly growth. The chart below show’s Pool’s trailing-twelve month revenues from 1Q 2013 through 1q2025 in the bright blue line. The dashed line is the average annual revenue growth of 7.7% projected from 1Q 2020.

If COVID hadn’t happened and Pool Corp was able to maintain its 7.7% revenue growth, they would have hit $6 billion in annual revenues in 2028. Instead, thanks to COVID, government stimulus, and super low interest rates, Pool Corp hit $6 billion in annual revenues in just two years instead of eight!

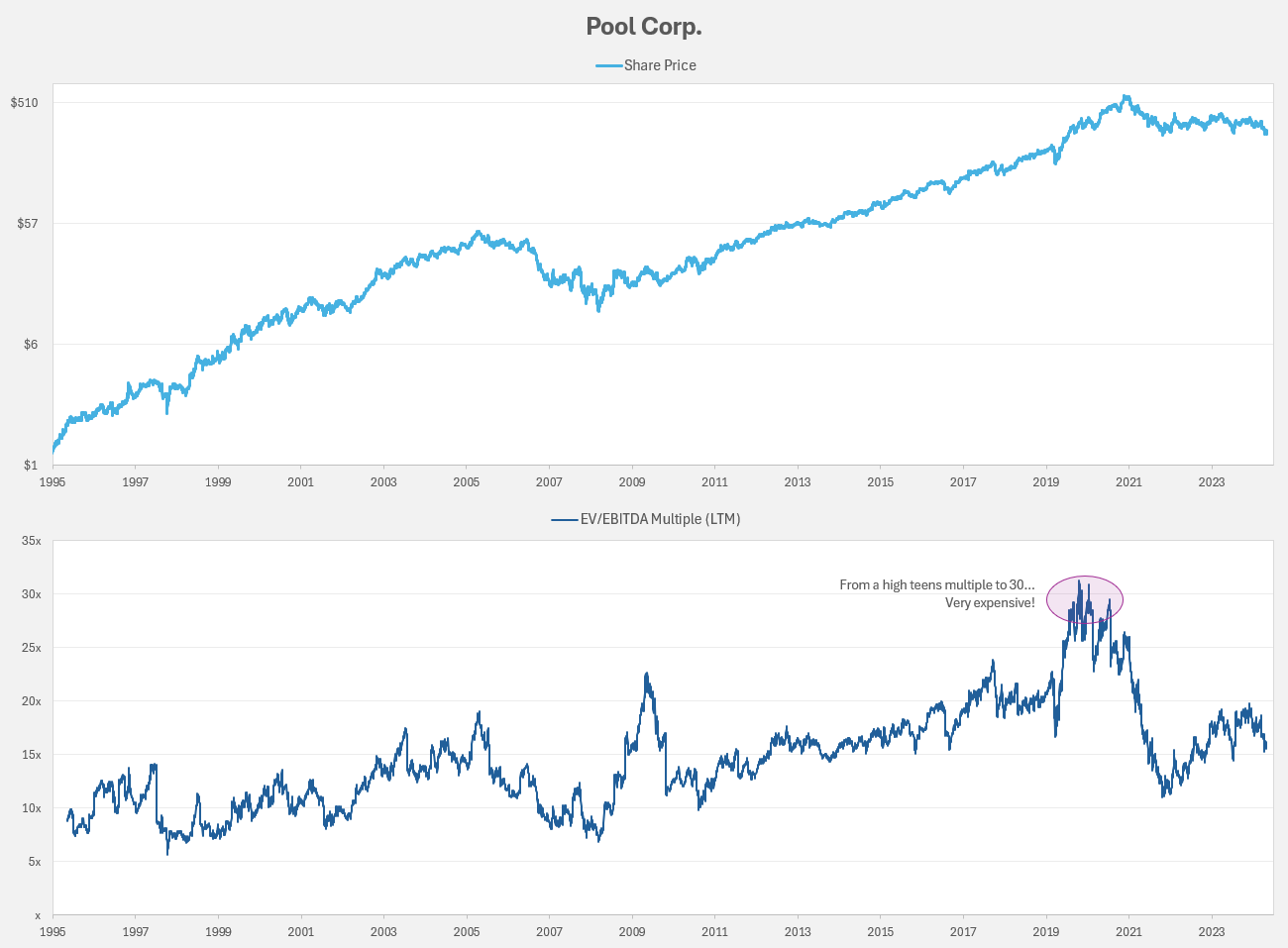

With so much demand pulled forward in such a short time, investors unwisely projected elevated growth to continue and bid up the share price of the company to levels never seen before. In a few years, the EV/EBITDA went from the high teens to 30 times. This in turn made the shares a much riskier investment relative to almost any other time in its history.

The Installed Base

The one good thing about the huge pull-forward of new pools during COVID is now there is a much larger installed base that must be serviced for several decades. The installed base of pools now sits at above 5.4 million in the United States.

The bad thing of course is that growth of new pool construction has been pressured for some time which has contributed to Pool’s negative revenue growth for the last nine quarters. Regardless, I believe Pool Corp will eventually get back on the track of its average annual revenue growth of 7%-8%. Below is my estimated path for Pool’s revenues going forward (the purple line). I assume Pool Corp will see positive growth in 4Q 2025 after which quarterly revenue growth will slowly ramp towards its historical average growth.

In addition to seeing more new pools being built, another way of tracking Pool’s progress towards returning to more robust topline growth is assessing what % of total sales is coming from pool and spa chemicals. These are the products that are absolutely necessary and cannot be deferred without detrimental outcomes.

Chemicals become a greater part of total revenues when people build fewer pools. Conversely, chemicals become a lesser part of total sales people are building more pools. From this perspective, this current period is almost as bad as the recession caused by the GFC.

In Summary

“[O]verall, what gives me great confidence in the business and the industry is that most of our business comes from the maintenance and repair of a growing installed base. So the installed base next year is going to be bigger than it is this year.

So there will be more pools to service. The demand for newer product with automation— connected pools, if you will—is going to continue to grow. There’s still an extremely large number of pools that are in place that have old technology.”

—Peter Arvan, CEO of Pool Corp, April 24, 2025

Despite two years of challenges to revenue growth and margins, Pool’s balance sheet is in good shape. Leverage currently stands at 1.47x even after the recent seasonal buildup of inventory. Given the low capital intensity of their business coupled with predictable revenues tied to pool maintenance, management has historically been an opportunistic repurchaser of shares—since the summer of 2022, Pool’s share count has declined from 40 million to now 37.7 million, a reduction of 5.8% in less than three years. With $291 million left on their current share repurchase authorization, management is going to the board with a request to increase its authorization (the current market cap is $11 billion).

In the end, I believe Pool’s goal of 6% to 9% revenue growth is still achievable. It’s just going to take a bit longer than expected to get back to normal. But in the meantime, management has the opportunity to repurchase shares at more reasonable multiples before results return to normal and the market revalues the shares.

Please Share and Subscribe

If you enjoyed this content, please share and subscribe.

Disclaimers for this Substack

The content of this publication is for entertainment and educational purposes only and should not be considered a recommendation to buy or sell any particular security. The opinions expressed herein are those of Douglas Ott in his personal capacity and are subject to change without notice. Consider the investment objectives, risks, and expenses before investing.

Investment strategies managed by Andvari Associates LLC, Doug’s employer, may have a position in the securities or assets discussed in any of its writings. Doug himself may have a position in the securities or assets discussed in any of his writings. Securities mentioned may not be representative of Andvari’s or Doug’s current or future investments. Andvari or Doug may re-evaluate their holdings in any mentioned securities and may buy, sell or cover certain positions without notice.

Data sources for all charts come from SEC filings, Koyfin, and other publicly available information.

best time to get into pool is when everyone is out of pool! love the business but some rough times