Seeing Beyond Copart's Recent Weakness

Why Unit Volumes Have Declined

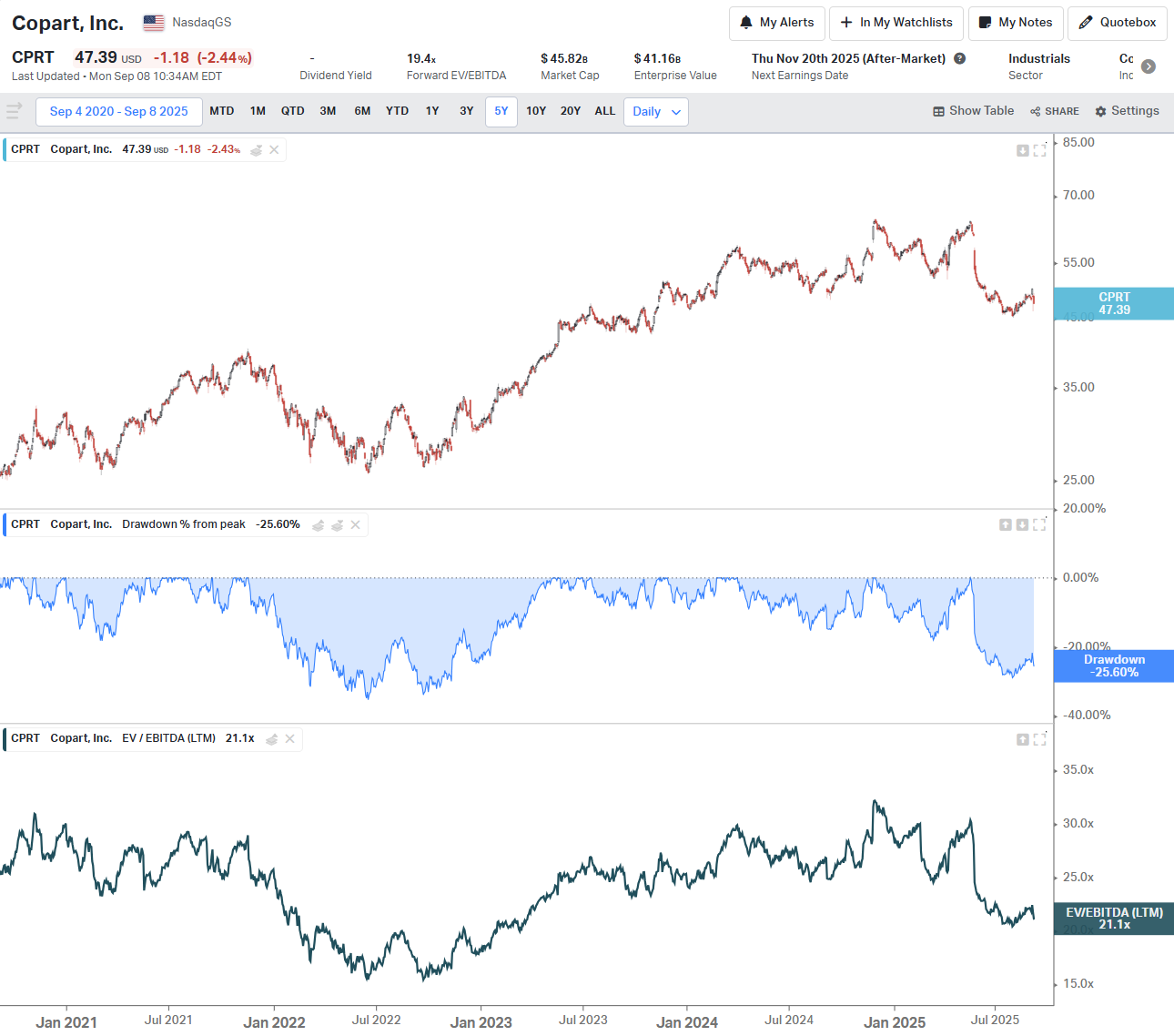

In recent quarters, Copart has experienced declines in unit volumes. While overall unit sales for fiscal year 2025 saw an increase of 4.8%, the fourth quarter of fiscal year 2025 experienced a 0.9% decline in global unit sales, with U.S. unit sales down 1.8%. This recent decline in unit sales follows the third quarter where Copart saw flat unit sales in the U.S. and where insurance volumes in the U.S. also decreased 1% year-over-year. The lack of growth in unit volumes in the U.S. has likely been just one factor weighing on the share price of Copart. Since late May, Copart’s share price declined from nearly $64 per share to $45 in the span of three months.

But all is not as bad as it seems. Offsetting weakness in the U.S. is a strengthening International business where Copart is finally seeing a real transition to its consignment business model.

Before we address all of the above, let’s review the big picture.

The Big Picture

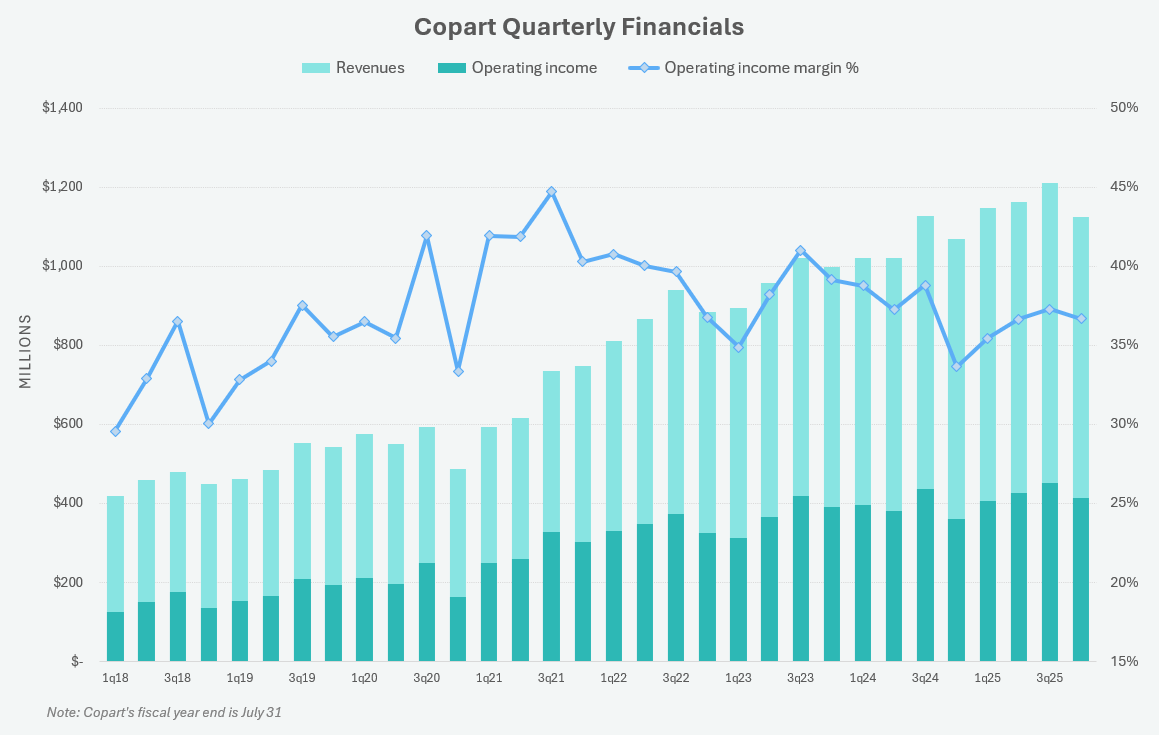

Revenues in the recent 4Q declined compared to 3Q per the seasonality of the business. Quarterly operating margins were 36.7% in 4Q 2025, which are above the 33.6% in the prior year’s quarter.

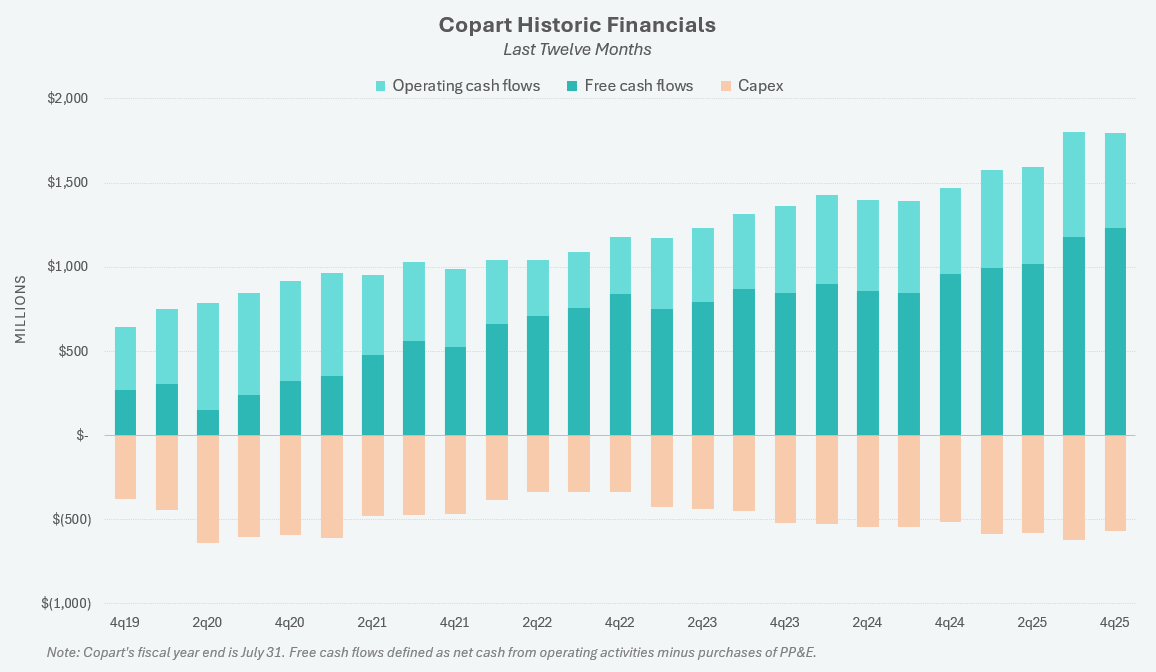

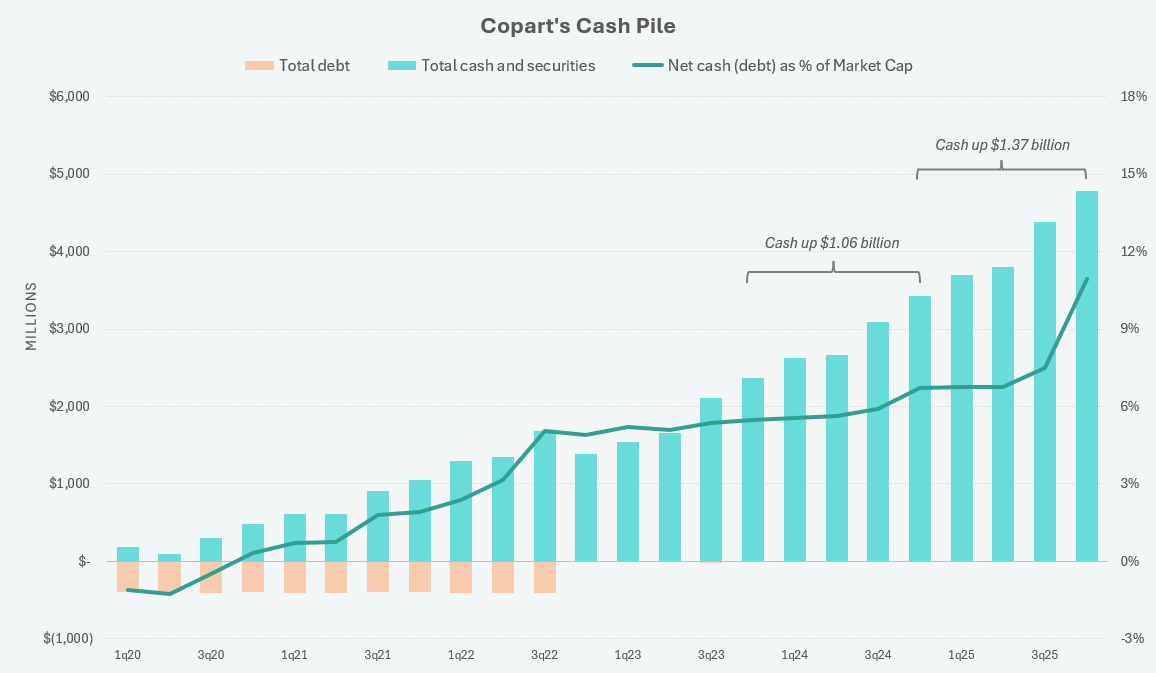

Cash continues to pile up despite trailing twelve month capex spend of >$500 million each quarter since 4Q 2023.

The total cash on Copart’s balance sheet is up $1.37 billion over the prior year. Furthermore, given the decline of Copart’s share price, cash as a percent of market cap is now in the double-digits at 10.9%.

Now let’s delve into the specific reasons behind the observed declines in both fee units and purchased units.

The Dynamics of Fee Unit Declines

Fee units, which represent the vast majority of Copart’s U.S. unit volumes, include vehicles consigned by insurance companies to Copart. Recent trends indicate weaker performance in the company’s largest geographical segment.

Impact of Uninsured and Underinsured Motorists

A significant factor contributing to softer volumes, particularly in the second half of fiscal year 2025, is simply the “cyclical ebbs and flows of uninsured and underinsured motorist populations.” As Leah Stearns, Copart’s CFO, explained in Q4 FY25, “substantial increases in insurance premiums over the course of the past several years” have led policyholders to “downgrade from collision coverage to liability only or has elected to forego insurance coverage altogether.” These vehicles, if involved in an accident, “may bypass the traditional insurance total loss funnel altogether,” thus not becoming fee units for Copart.

Jeffrey Liaw, CEO of Copart, further noted that “earned car years for the first calendar quarter of 2025 declined by 4.3% versus that same quarter in 2024,” while the total vehicle population grew, suggesting a decrease in insured drivers.

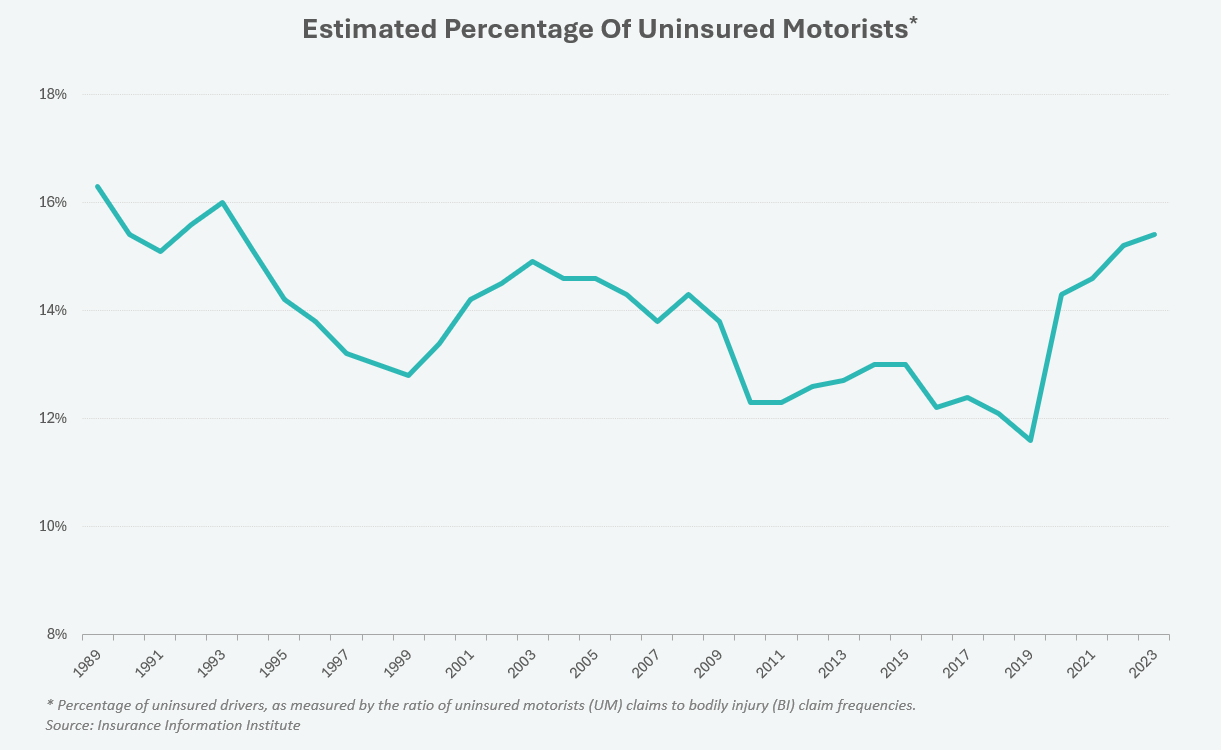

Indeed, the estimated number of uninsured motorists has increased since 2019. The chart below shows the estimated percentage of uninsured motorists was 11.6% in 2019 and has increased each year afterward, ultimately hitting 15.4% in 2023. Although I don’t have the data for 2024, I can only assume this figure increased again given the still elevated costs of insuring a vehicle.

Strategic Pruning of Low-Value Units

Copart also recently reduced its focus on certain low-value fee units. In Q1 FY25, Leah Stearns said, “low-value units, including charities and municipalities, declin[ed] 4%.” Then in Q4 FY25, Stearns mentioned Copart in the U.S. had shifted “a significant volume of low-value noninsurance units from our Copart direct channel—which are purchased units—to our direct buy channel.” The reason for this was to allow “Copart to more efficiently market lower ASP vehicles by directly connecting sellers and buyers and avoiding the unnecessary costs associated with transportation and storage at a Copart facility.”

This shift contributed to Copart’s recent negative growth in units sold. However, it is also part of Copart’s evergreen strategy to always optimize for long-term growth and profitability. Essentially, Copart is allocating its resources to higher-margin business lines, even if it means fewer units overall in the short-term.

European Inflection

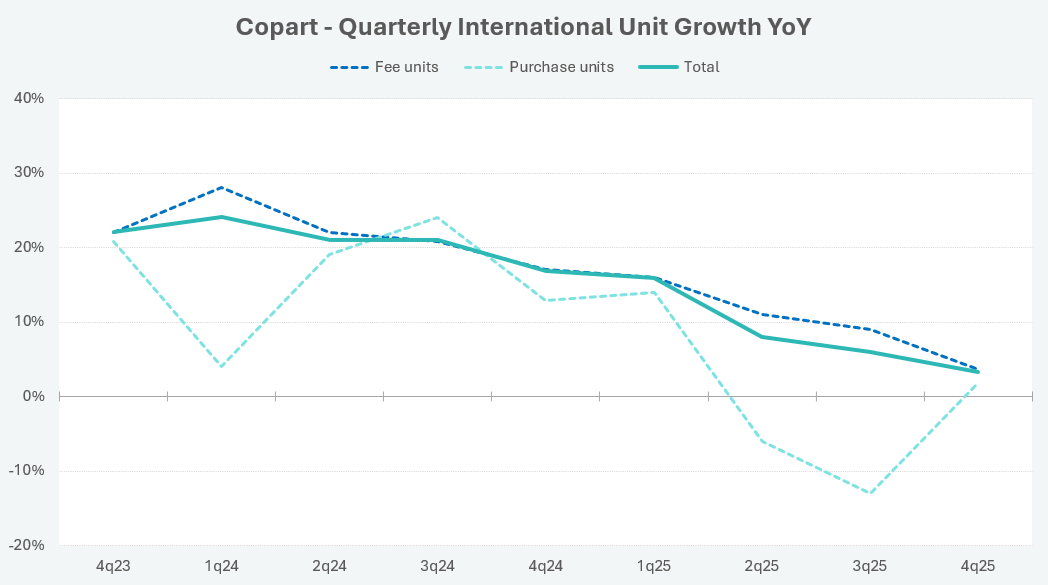

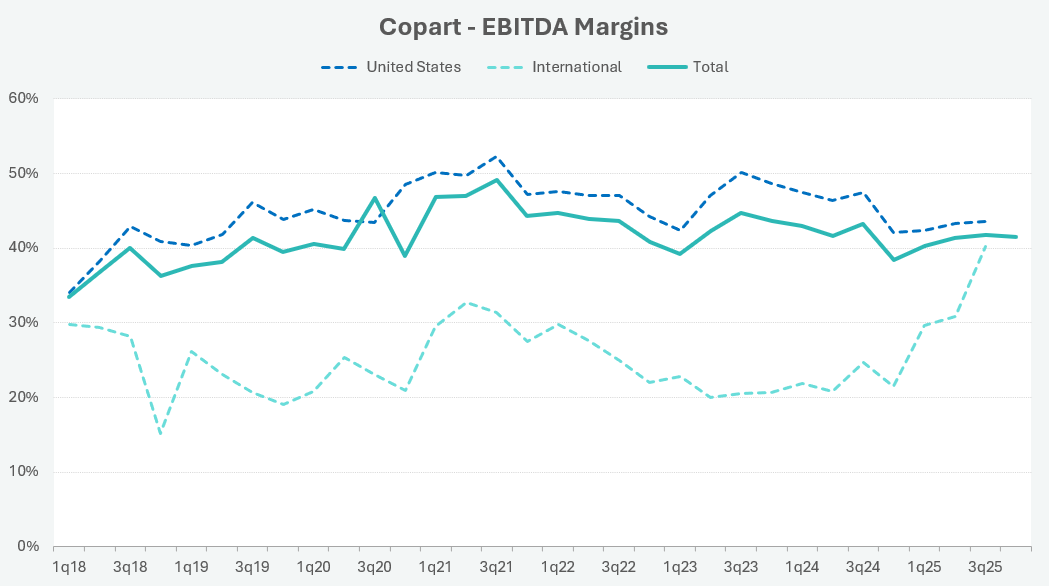

The transition to a consignment model in continental Europe seems to be accelerating. I see the evidence in two places: (1) the fact that growth in fee units sold continues to be greater than growth in purchase units sold; and (2) the significant uplift in EBITDA margins for Copart’s International business over the last several quarters.

Internationally, purchased unit declines over the last several quarters are largely a result of a “shift of insurance units primarily in Germany, transitioning from purchase contracts to consignment.” Leah Stearns explained this move impacts reported revenues, shifting it from gross vehicle sales to service fees. While this reduces purchased unit revenue and volume, it benefits fee unit growth and aligns Copart’s interests with its insurance customers, a long-term strategic goal. CEO Jeff Liaw noted this progression is “gradual” but is the desired direction for the business.

Copart entered Germany in 2012 and has slowly and persistently attempted to persuade the insurance carriers in that market to shift to a more profitable way of dealing with damaged vehicles. Historically, policyholders in Germany have retained the salvage vehicle after an accident, rather than the insurance company. Changing a historical way of doing business, especially in the world of insurance, can be, and has been, an enormous undertaking.

In the U.S., Copart’s EBITDA margins are north of 40% due to two differences relative to a country like Germany. First, insurance carriers in the U.S. retain the salvage vehicle after the accident, which enables faster and more efficient decision-making on whether to repair or total a car. Second, Copart primarily operates as an agent for the insurance carrier in the U.S., selling vehicles on consignment for fees rather than purchasing them outright. This model significantly reduces inventory risk and aligns Copart’s financial incentives with those of its sellers, as Copart earns a percentage of the sale price.

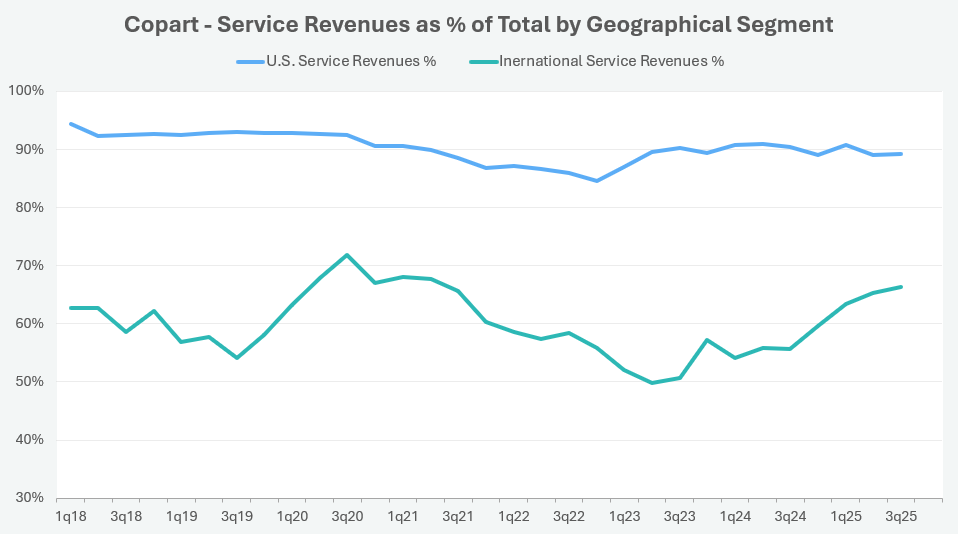

The stark difference between Copart’s U.S. and International segments are also evident in the mix of service revenues vs. revenues from vehicle sales. Copart’s U.S. segment receives about 90% of its revenues from service fees while the International segment has historically received just 50%-60% of its total revenues from fees.

However, given the shift in Germany and Europe towards the U.S. operating model of Copart, margins for the International segment have increased to an all-time high of 40.2% as of last 3Q 2025.

Summary

There is nothing to suggest from the past two quarters any permanent shift in the quality of Copart’s business. Copart since its founding has experienced growth in all economic and regulatory environments. Although the frequency of auto accidents has declined over time, the growth in severity of accidents has outpaced those declines.

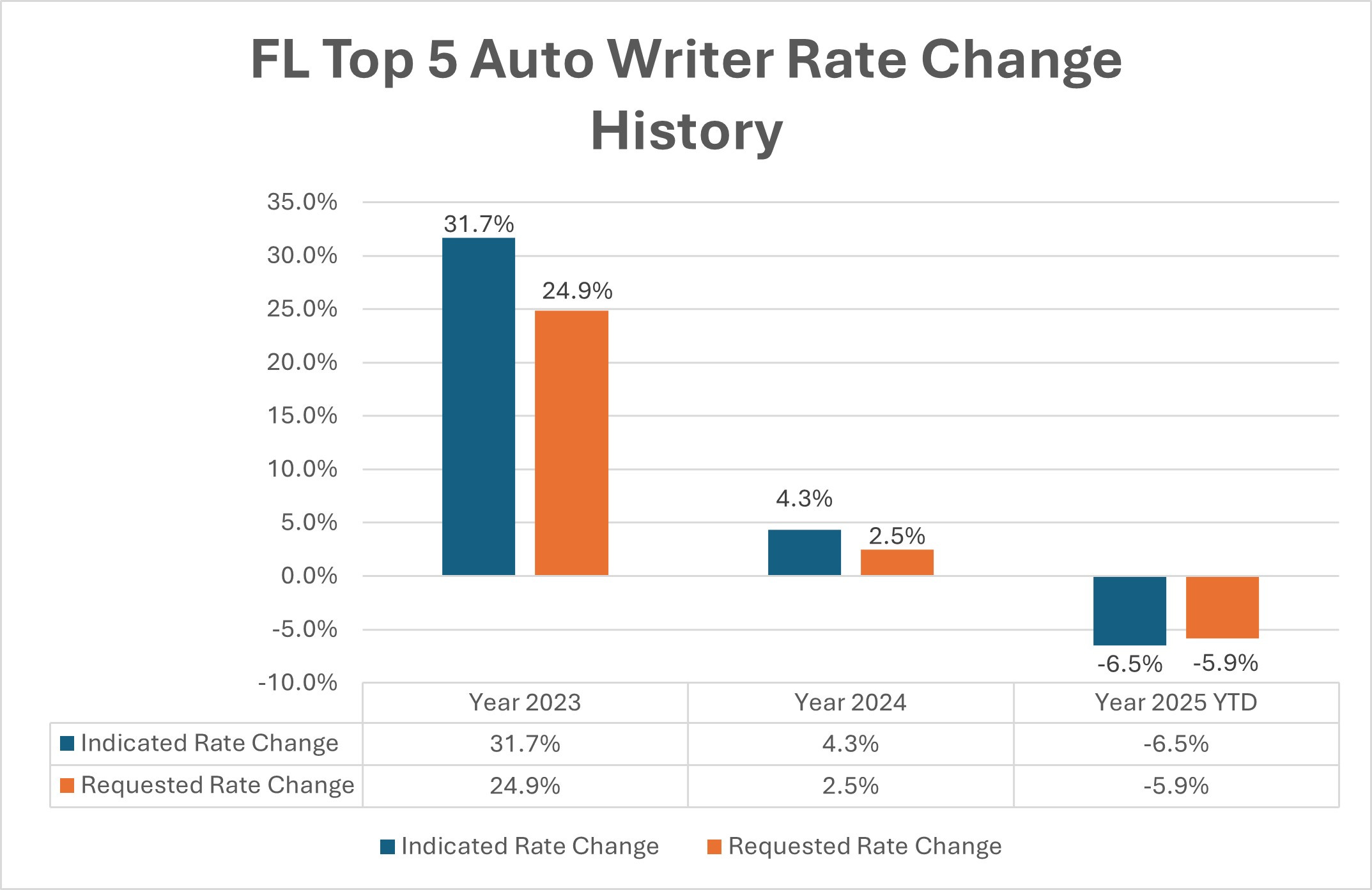

Copart’s unit volume figures are likely not a reflection of a market downturn or Copart losing significant business to IAA, its primary competitor. Instead, the lackluster volume is tied to inflation in auto insurance rates, which in turn has caused more people to forgo insurance. This trend will eventually ameliorate, either due to improvements in macroeconomic factors like reduced inflation or a more robust economy. At the very least, a state insurance commissioner has every incentive to ensure affordability of insurance for their citizens so that all are protected and made whole in the event of accidents. One example of a large state starting to roll back rates is Florida.

Despite this temporary ebb in unit volume growth, Copart management remains confident in the “secular trends in favor of rising total loss frequency,” which continues its long-term upward trajectory. Copart’s International business is finally reaching the profitability of its U.S. segment. The ever increasing frequency of total losses, coupled with Copart’s strategic investments in its global network, technology, and service offerings, will continue to fuel Copart’s long-term growth by providing unmatched auction liquidity and superior returns for sellers.

Further Reading

Copart Q1 2025 Update

“[A]s we look forward on a 5-, 10- and 20-year horizon, our baseline expectation continues to be of ongoing organic industry growth as population and vehicle miles traveled trends—plus total loss frequency most importantly of all—more than offset declining accident frequency, as safety technologies penetrates new vehicle …

Recession Resiliency: The Auto Repair Ecosystem

CCC Intelligent Solutions (CCCS) is a business that is central to the auto repair ecosystem. Its software helps coordinate the collective efforts of: auto insurers like GEICO and Progressive; salvage and auction companies like Copart and IAA; and repair shops such as those under the wing of

Copart's Cash Continues to Grow

“The one afterthought I'd offer is that our capitalization with our clients is a distinctive competitive advantage. Our conservative balance sheet, our net cash balance, equips us such that we can be patient even through a crisis. So in the midst of a pandemic, when nobody knew for how long dr…

Please Share and Subscribe

If you enjoyed this content, please share and subscribe. Leave a comment as well if you have the time!

Disclaimers for this Substack

The content of this publication is for entertainment and educational purposes only and should not be considered a recommendation to buy or sell any particular security. The opinions expressed herein are those of Douglas Ott in his personal capacity and are subject to change without notice. Consider the investment objectives, risks, and expenses before investing.

Investment strategies managed by Andvari Associates LLC, Doug’s employer, may have a position in the securities or assets discussed in any of its writings. Doug himself may have a position in the securities or assets discussed in any of his writings. Securities mentioned may not be representative of Andvari’s or Doug’s current or future investments. Andvari or Doug may re-evaluate their holdings in any mentioned securities and may buy, sell or cover certain positions without notice.

Data sources for all charts come from SEC filings, Koyfin, and other publicly available information.

Good post!

I appreciated Jeff's comments about how he and Leah approach M&A deals as if they're writing a personal check. However, if applied to share repurchases, I have to wonder if the same logic indicates he and Leah don't think the stock is cheap today. They aren't repurchasing and they aren't buying stock themselves.

What do you think?