Q1 2025 Andvari Letter

Strength and Durability

Andvari Associates has allowed us to share its Q1 2025 letter. Please enjoy.

Dear Friends,

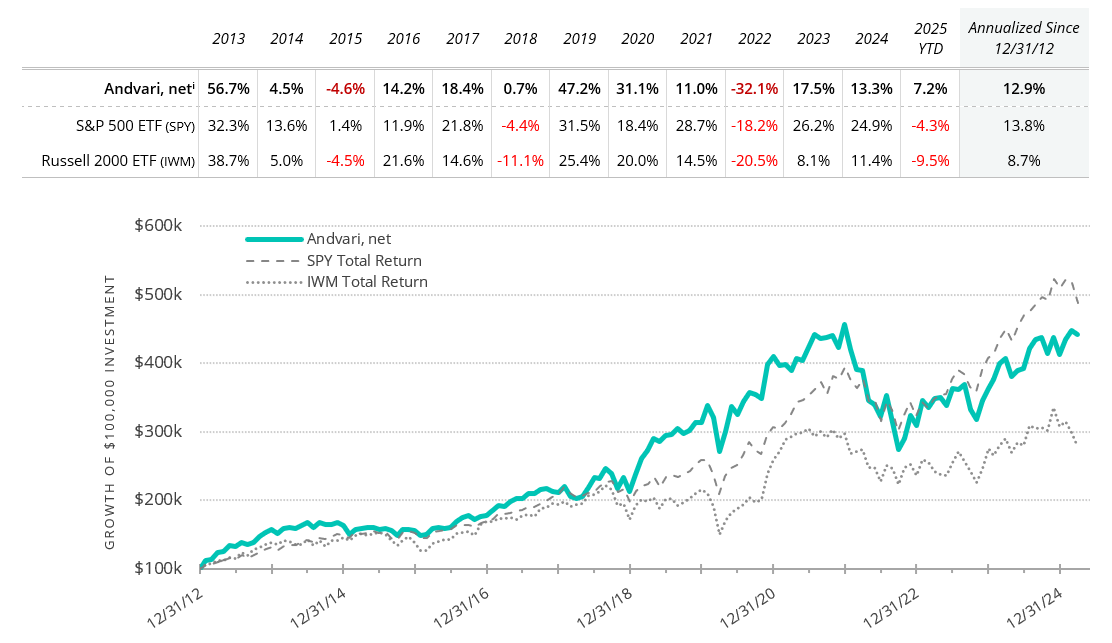

For the first three months of 2025, Andvari is up 7.2% net of fees while the SPDR S&P 500 ETF is down 4.3%.* Andvari clients, please refer to your reports for your specific performance and holdings. The table below shows Andvari’s composite performance while the chart shows the cumulative gains of a $100,000 investment.

This period of significant outperformance is welcome. Andvari has suffered—hopefully not for much longer—from a long bout of underperformance due to the absence of shares of the “Mag 7+” in client portfolios. The Mag 7+ list includes some of the largest and best performing companies in the S&P 500: Alphabet, Amazon, Apple, Meta Platforms, Microsoft, Nvidia, Tesla, and Netflix. The chart below from WisdomTree illustrates the stark difference in performance between just the Mag 7+ and the remaining 492 companies in the S&P 500:

From the start of this year to April 1, the “S&P 492” was up 0.89% while the Mag 7+ component was down 13.12%.

With money flowing out of the Mag 7+ during the past quarter, the money seems to have flowed into the shares of many of the businesses we own. Although our holdings vary in size of revenues, enterprise value, and the products and services they sell, they do not vary in three attributes. Andvari believes our holdings to be (1) high quality businesses, (2) run by able managers, and (3) capable of allocating capital to produce above average returns over a long period of time. Below is our update on many of them.

ANDVARI HOLDINGS

Life Sciences and Companion Animals

Andvari has investments in four businesses that serve the life sciences and companion animal industries—companion animals are primarily the cats and dogs that are the typical pets for us humans. Mettler-Toledo and Danaher sell essential equipment and consumables into the life sciences and pharma industries. IDEXX and Zoetis serve the companion animal market with equipment, consumables, software, and pharmaceutical products, all of which makes the lives of veterinarians easier and improves the quantity and quality of the lives of animals.

All four companies are leaders in their respective markets and all benefit from solid growth tailwinds. Margins and returns are high, the businesses are not capital intensive, and revenue growth rates have generally ranged from mid- to high single digits.

However, as we’ve mentioned before in prior letters, due to the COVID era, a large amount of demand was pulled forward for these businesses. All four have been working through this overhang and their market valuations have declined as a result. Although it has taken longer than Andvari anticipated for growth to normalize for these businesses, when growth reverts to pre-COVID levels, we should see their share prices appreciate.

Nicotine and Tobacco

Last year, Andvari made its first investments in tobacco companies with the purchase of Philip Morris International and Altria. At the time of our purchase, Philip Morris and Altria had underperformed the S&P 500 over the prior 5- and 10-year periods. Both traded at low valuations and with high dividend yields. But thanks to following the industry off and on for 10+ years, and thanks to many discussions with long-time shareholders of the companies, Andvari felt the time was right to make the plunge. The timing could not have been much better for us as both companies have so far contributed positively to Andvari’s recent overall performance.

The problem—or the feature, depending on your perspective—with the tobacco industry has been a declining population of cigarette smokers in developed countries. Over the last four or five years, the decline in these smoking populations has accelerated, which in part explains the poor share performance of the tobacco companies between 2017 and 2023. Despite this, the tobacco companies have maintained, or slowly increased, their revenues and profits with regular price increases on cigarettes.

More importantly, over the last two decades the constituents of the tobacco industry have poured money into research and development efforts to create reduced risk products to satisfy the desires of their traditional customers more safely. As a result, the industry players have come out with vastly safer products that deliver nicotine without the combustion process. Note well, it is the chemicals that come from the burning of tobacco that cause cancers, not nicotine itself. As a result, greater and greater numbers of smokers have been switching over to vaping, heat-not-burn products, and nicotine pouches.

The country of Sweden is one of the most extraordinary examples of an entire populace switching from cigarettes to nicotine pouches or their local variant called snus. As a result, smoking rates in Sweden fell from 40% of the population in 1976 to 5.8% in 2022. Cancer rates related to cigarette use plummeted and Sweden will soon be the first country in Europe where the smoking population will be less than 5% of its total.

Reduced risk products from the tobacco companies are undeniably good for public health. And these products have only started to prove they will be good for the tobacco companies that are transitioning their customers away from cigarettes. The nicotine pouch category in particular has been growing rapidly. You may have heard of the ZYN brand. Philip Morris is the brand owner after its purchase of Swedish Match in late 2022. ZYN has been growing between 40%-80% and this is despite an ongoing shortage of the product. Altria has a brand called on! that has been growing between 32%-48% over the last two years.

Finally, there are 1.1 billion nicotine users in the world. One billion of them are cigarette users and only one hundred million are users of reduced risk products. There is a long way to go for nicotine pouches and other safer products to take even half of the share of the entire nicotine market. As the new products grow their market share, they will have the same financial qualities of the cigarette business (extraordinary margins, high returns, and highly predictable revenues) which will benefit shareholders. Governments will benefit by a significant source of tax revenues not disappearing with the demise of cigarettes, and society will benefit from a dramatic decline in smoking-related cancers.

Rates, REITS, and Real Estate

Our holdings that have been most sensitive to interest rates remain well-poised for outperformance. Our two cell tower REITs—American Tower and SBA Communications—have continued to reduce their debt and leverage ratios. Both have also recently increased their quarterly dividend payments to shareholders. American Tower is most notable in this regard as it paused dividend increases for a year.

CoStar Group continues their investments in the space of online residential property portals. They own fast-growing challenger brands in the U.S. and U.K. in the form of Homes.com and OnTheMarket, respectively. During the past quarter, CoStar also made a bid to acquire Domain Group, the owner of online portals for residential and commercial real estate listings in Australia. Andvari continues to root for CoStar’s success in the residential space, but we do not think success is necessary to achieve good shareholder returns going forward. We believe the market is slightly undervaluing CoStar’s commercial real estate business lines because heavy investments in the residential category have decreased overall margins. If CoStar can generate value from residential, that will be excellent. If not, the investments will end and company-wide margins will shoot up dramatically, and hopefully the share price as well.

TARIFF TIME

With tariffs dominating news headlines, we must first confess we cannot predict what exactly the impact will be upon our holdings. However, it is still worth discussing the degree to which tariffs may or may not affect the companies in which we are invested. For several reasons, our companies are prepared to manage through this new paradigm.

First, tariffs in most historical cases have been applied to physical goods and commodities. Because Andvari owns many businesses that sell intangibles like software or services, we are well positioned. Our software businesses include Constellation Software, Topicus.com, Tyler Technologies, and Chapters Group. We also own many businesses we think of as primarily service-based, such as:

Mastercard. The company enables the transfer of value using technology and provides other value added services to financial institutions and merchants.

Rollins. One of the largest pest control services in the U.S.

Arthur J. Gallagher. They provide insurance and reinsurance broking all around the world.

S&P Global. Provides credit ratings and data services to businesses and financial institutions.

Kelly Partners. Provides accounting services to small and medium sized businesses primarily in Australia, but increasingly in the U.S. and U.K.

Booz Allen Hamilton. Provides management and technology consulting services primarily to the U.S. government. This is a small, new investment for Andvari that we started after the share price fell significantly due to negative news about DOGE and aggressive government efficiency efforts.

Again, it is unlikely that any of the above businesses will directly feel the effects of tariffs to the same extent as those who manufacture physical goods in lower-cost countries and then import them to the United States.

Second, for the handful of companies in Andvari portfolios that do make physical goods, they all share a mitigating factor: they all have above average pricing power. The source of their pricing power stems from selling products that are critical to the end user and yet are a small proportion of the customers’ total costs. They also often benefit from high switching costs. Danaher, Mettler-Toledo, Zoetis, and IDEXX fall into this camp, as well as TransDigm.

More specifically about Danaher, their customers design its equipment and consumables into pharma and biologic production lines. If a research lab has made the significant investment to standardize on Danaher equipment, it must continue to buy the appropriate consumables and receive regular maintenance services from Danaher. Thus, if a lab needs to grow, there is little chance a lab would stop buying from Danaher. If a pharmaceutical or biologic manufacturer needs to grow, there is virtually no chance they will switch to similar equipment unaffected by tariffs. It is just too costly and risky to be recertified by the FDA or its European equivalent, the EMA. Danaher can raise prices on its customers given the value provided by its products and the switching costs involved.

TransDigm is a business with extreme pricing power. They make hundreds of different parts that go into commercial and military aircraft. Because TransDigm owns the intellectual property or is the sole source provider of nearly all its products, it can easily raise price increases when there is inflation or when its costs rise.

Andvari also owns two companies that are distributors of physical goods: O’Reilly Auto Parts and Pool Corporation. Out of all the businesses we own, these two might face the greatest risks of rising costs due to tariffs, but we shall see. O’Reilly is one of the largest distributors of auto parts in the United States and they do most of their business in this country. However, they do source many of their products from countries like China, Mexico, and India. Back during COVID and President Trump’s first tariffs, the company started diversifying it supplier base to create a more resilient supply chain and to minimize as best they could the effects of tariffs. But even with tariffs on products that they could only source from China (like suspension components), O’Reilly and its competitors were still able to pass on 20%-25% price increases directly to their customers.

Regarding Pool Corporation, they are the largest distributor of pool-related products and supplies in North America. We like that the company has never competed solely on price. They sell based on value and providing the best customer experience. They have also historically been able to pass on inflationary price increases to their customers.

ANDVARI TAKEAWAY

We own a collection of excellent and highly resilient businesses. Several were started over one hundred years ago and have survived wars, depressions, pandemics, and everything else in between. Philip Morris was founded in 1847; Standard & Poor’s was founded in 1860; Orkin, the core brand of Rollins’ pest service business, was founded in 1901; Booz Allen was founded in 1914; for Mettler-Toledo, the Toledo Computing Scale and Cash Register Company was founded in 1901 while Mettler Instruments AG was founded in 1945; Arthur J. Gallagher was founded in 1927; O’Reilly Auto Parts was founded in 1957. Although we cannot brag about the founding dates of our software businesses to the same extent, they also are highly durable businesses due to the mission critical products they sell into niche markets. Although the next year or two might be unpleasant for shareholders, our businesses will prove their resiliency yet again.

As always, I love to hear from clients and anyone else. Please contact me with your thoughts, comments, or questions.

Sincerely,

DEO

Disclaimers for this Substack

The content of this publication is for entertainment and educational purposes only and should not be considered a recommendation to buy or sell any particular security. The opinions expressed herein are those of Douglas Ott in his personal capacity and are subject to change without notice. Consider the investment objectives, risks, and expenses before investing.

Investment strategies managed by Andvari Associates LLC, Doug’s employer, may have a position in the securities or assets discussed in any of its writings. Doug himself may have a position in the securities or assets discussed in any of his writings. Securities mentioned may not be representative of Andvari’s or Doug’s current or future investments. Andvari or Doug may re-evaluate their holdings in any mentioned securities and may buy, sell or cover certain positions without notice.

Data sources for all charts come from SEC filings, Koyfin, and other publicly available information.

Please Share and Subscribe

If you enjoyed this content, please share and subscribe.

* Andvari performance represents actual trading performance of all, actual clients beginning on 4/12/13. Performance from 12/31/12 to 4/12/13 is actual performance of proprietary accounts, namely the accounts of Andvari’s principal, Douglas Ott. Andvari believes including Ott’s performance figures for the first 4 months and 12 days of 2013 is fair as he managed those accounts similarly to Andvari’s first clients. All performance, including the initial proprietary period, are net of management fees—assumed to be 1.25% per annum, paid quarterly, as currently advertised—net of brokerage commissions and expenses, time-weighted, and includes all cash and other securities. Performance includes realized and unrealized returns and excludes the effects of taxes on incurred gains or losses. Andvari does not certify the accuracy of these numbers. Performance data quoted represents past performance and does not guarantee future results.

The exchange traded funds (ETFs) are listed as benchmarks and are total return figures and assumes dividends are reinvested. The SPY ETF is based on the S&P 500 Index, which is a float-adjusted, capitalization-weighted index of 500 U.S. large-capitalization stocks representing all major industries. The IWM ETF is based on the Russell 2000 Index, an index of 2,000 U.S. small-cap stocks. It is not possible to invest directly in an index. Because Andvari client portfolios are non-diversified, the performance of each holding will have a greater impact on results and may make them more volatile than a more diversified index. Andvari also engages or may engage in strategies not employed by the S&P 500 or the Russell 2000 including, without limitation, the use of leverage.

One may request a list of all securities mentioned or recommended for the preceding year as of the date of this letter. You may contact Andvari using the information below. Actual client results may differ from results depicted in this letter. Any investment involves substantial risks, including, but not limited to, pricing volatility, inadequate liquidity, and the loss of principal. Investment strategies managed by Andvari Associates LLC may have a position in the securities or assets discussed in this article. Securities mentioned may not be representative of the Andvari's current or future investments. Andvari may re-evaluate its holdings in any mentioned securities and may buy, sell or cover certain positions without notice.

The discussion of Andvari’s investments and investment strategy (including, but not limited to, current investment themes, the portfolio managers’ research and investment process, and portfolio characteristics) represents the views and opinions of Andvari’s portfolio managers and Andvari Associates LLC, the investment adviser, at the time of this report, and can change without notice.

This document does not in any way constitute an offer or solicitation of an offer to buy or sell any investment, security, or commodity discussed herein or of any of the affiliates of Andvari.

The information contained in this document may include, or incorporate by reference, forward-looking statements, which would include any statements that are not statements of historical fact. Any or all of Andvari’s forward-looking assumptions, expectations, projections, intentions or beliefs about future events may turn out to be wrong. These forward-looking statements can be affected by inaccurate assumptions or by known or unknown risks, uncertainties, and other factors, most of which are beyond Andvari’s control. Investors should conduct independent due diligence, with assistance from professional financial, legal and tax experts, on all securities, companies, and commodities discussed in this document and develop a stand-alone judgment of the relevant markets prior to making any investment decision.