Kingsway: A Search Fund in Public Company Clothing

On the Hunt for Small Businesses

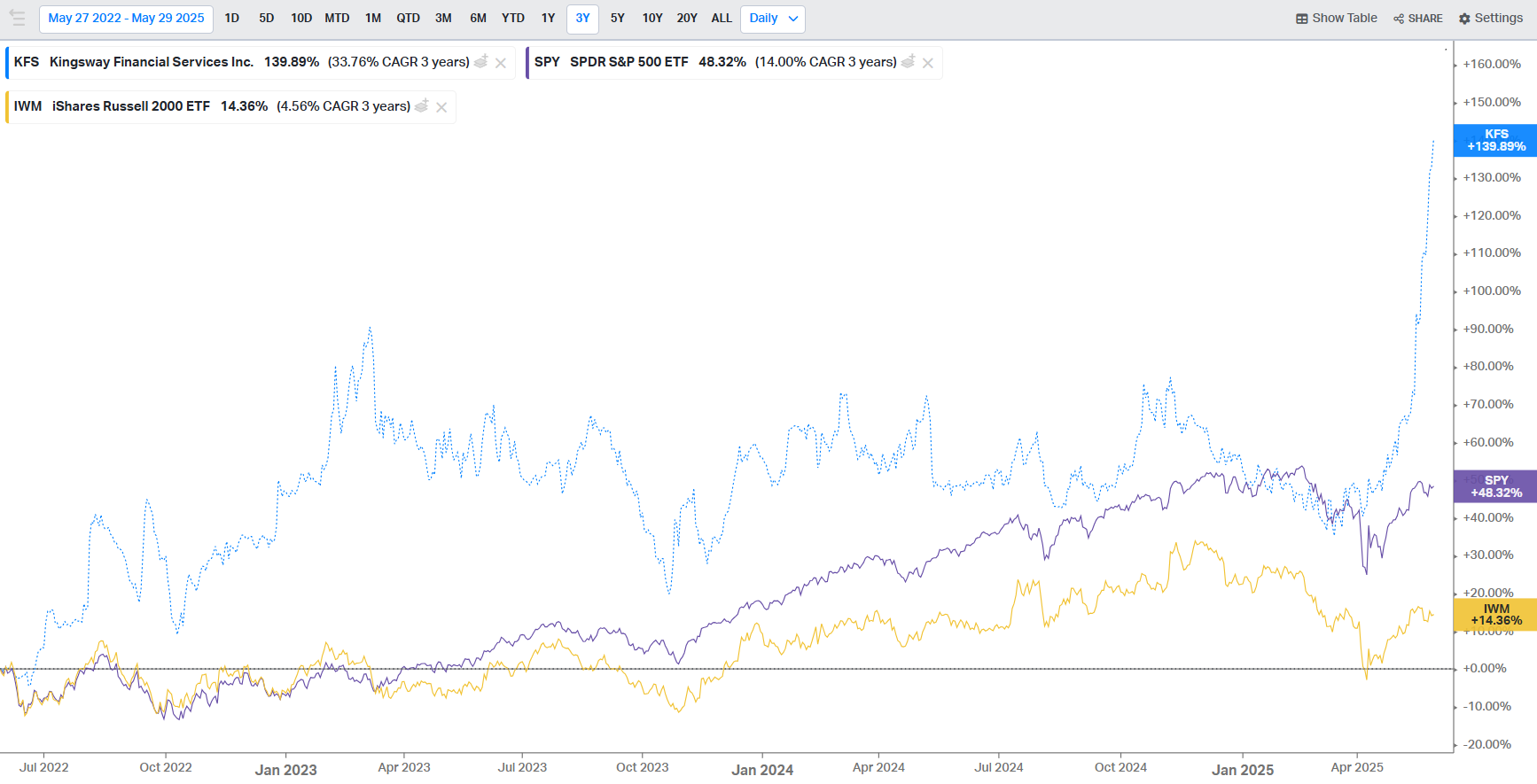

Kingsway Financial (KFS) is likely one of the most unique public companies out there. For many years, the company has been slowly shucking off legacy assets—and a legacy of poor investments by prior management—to a position where it will soon be focused solely on its search fund segment. In this post I’ll lay out the basic investment story as well as why I think the share price has recently gained so much in such a brief time.

An Unfortunate History

Kingsway got its start in 1989 as a niche insurance company based in Canada. Over the next two decades, the company grew significantly. It was only until the Great Financial Crisis the company fell apart, with investors learning Kingsway had grown recklessly with little regard for conservative underwriting. From an all-time high share price of nearly $90 in 2006, the shares began a slow descent. The slow descent turned into a rapid descent in 2008 and 2009 and then kept falling until bottoming below $2 per share in the summer of 2012.

Having accumulated significant net operating losses (NOLs) in 2008 and 2009, the company attracted the attention of Joseph Stilwell, an activist investor best known for his often contentious campaigns in the niche world of small community banks. Stilwell gained control of Kingsway and installed Larry Swets as CEO to transform Kingsway into a Berkshire-like operation to make full use of the NOLs.

However, Swets ultimately did not work out. Under Swets, Kingsway acquired a variety of assets, most of which failed to produce results. There also apparently were conflicts of interest that came to light. However, perhaps the best investment Swets made was that of Argo Management Group in 2016, a search fund that came with J.T. Fitzgerald as its founder and leader. Stilwell replaced Swets with Fitzgerald in 2018.

Following the departure of Swets, nearly every other manager or executive at Kingsway also left. Fitzgerald hired a new team and began the long process of cleaning up the remaining mess at Kingsway. Since 2018, Kingsway has exited all extraneous investments, sold the money-losing insurance business, reincorporated Kingsway to the U.S. from Canada, and lowered debt dramatically. This has freed Fitzgerald to focus on the two gems of Kingsway, its warranty businesses and its nascent search fund segment, which would eventually be dubbed its “Kingsway Search Accelerator” (KSX) segment.

The Search Fund Model

The search fund concept has existed since the 1980s, being first propounded by Irving Grousbeck, an early pioneer in the cable TV industry who then became a professor at Stanford University’s Graduate School of Business. The idea behind search is its a vehicle whereby a young entrepreneur raises capital from investors to search for a small business ($1 to $3 million of EBITDA) to acquire and run. “Entrepreneurship through acquisition” (ETA) is another term for it.

Since the inception of the idea, the returns to investors have been fantastic. Research from Stanford’s GSB shows that search funds have delivered annual returns in the mid-30% range over decades, and this includes the performance of search funds that failed to make an acquisition and the funds that produced losses. Even when excluding the extremely positive returns of outlier search funds, the overall returns for the remainder of search funds falls by just a a few points.

The long-term results of the search fund asset class speaks for itself and is precisely why Kingsway is such a unique opportunity.

But not only does Kingsway hope to achieve similar results for itself, it also has many advantages over the traditional search fund model that in theory should improve the likelihood of such results:

Kingsway is a liquid, publicly traded vehicle that does not have a second layer of fees like a fund of search funds has;

Being publicly traded, Kingsway provides greater reporting and transparency than private search funds;

Kingsway has better and quicker access to capital at relatively better terms;

Kingsway has more robust infrastructure and support to accelerate the search process;

Kingsway has developed and implemented their own continuous improvement methodology, modeled after the best practices of companies like Danaher, to improve the odds of success pre- and post-acquisition;

They have an outstanding advisory board that includes the likes of Tom Joyce, former Danaher CEO, and William Thorndike, famed author of The Outsiders in addition to being a pioneer in the search fund space;

Kingsway has significant NOLs it can use to enhance the returns of its acquisitions; and

Kingsway has an extraordinarily selective funnel of future searchers looking for its backing, with 100 searchers interviewing for just two openings most recently.

The Pudding Already Has the Proof

Importantly, Kingsway already has evidence its search fund segment can work within a publicly-traded company. It’s already exited from one of its earliest search investments, PWSC, a home warranty business, for a 10x net return. Kingsway’s search platform also has several current businesses (Ravix, DDI, and SPI) that have quickly grown or greatly improved in profitably in a brief period of time:

“Many of the businesses in Kingsway’s current portfolio are demonstrating business momentum. Ravix has nearly doubled EBITDA in 3.5 years. DDI is on pace to more than double revenues within 4 years. SPI improved from Rule-of-10 to Rule-of-40 in under 2 years.”

—Kingsway’s 2025 Investor Day presentation, page 17

Catalysts

In just the last several months, Kingsway has had a spate of positive changes, as well as hints at a few other future catalysts, all of which has helped propel the share price.

First, Joseph Stilwell sold a large portion of his stake in Kingsway to funds managed by David Patinkin and Josh Horowitz. Patinkin, through his David Capital Partners, now owns 9.2% of KFS’s shares. Both Patinkin and Horowitz were appointed directors on KFS’s board as of March 31, 2025.

Consequently, Stilwell’s ownership of Kingsway has now declined from 26.9% of in November 2023 to 21% as of the most recent filings and share count. This is important because it has reduced the frequent pressure experienced by Kingsway shares over the last few years due to Stilwell selling whenever he can. Given that Kingsway has been outside the ambit of Stilwell’s investment focus (small community banks), Stilwell gained some liquidity for his investors and at the same time the shares remain in the hands of well-respected long-term investors.

Second, Kingsway has started to signal changes in its extended warranty segment. On April 2, Kingsway appointed a new leader, Rob Humble, for two of its three warranty businesses. Kingsway has also communicated Humble has incentives that are very similar to the incentives enjoyed by the leaders of the businesses in its search segment. In addition to this, Kingsway leadership in their public comments have also hinted they want to realize as much value from the majority of their NOLs that expire in 2029.

I see two pathways here given the changes at the warranty businesses. One might be that Kingsway hired to Humble to accelerate growth and profitability with an idea towards selling these businesses at a premium prior to the expiration of Kingsway’s $385 million in NOLs in 2029. Another option is that the third warranty business not being led by Humble will eventually be sold and the remaining warranty businesses reclassified into the Kingsway search fund segment. Either of these options would create cleaner reporting and the ability for Kingsway to promote itself as a company focused solely on search. Being a “pure play” company is something for which they should receive a greater valuation by investors.

The third catalyst, albeit in its infancy, is related to Kingsway acquiring Bud’s Plumbing in Evansville, Indiana, via Rob Casper, one of Kingsway’s former entrepreneurs-in-residence and now new CEO.

Asked why he decided to partner with Kingsway to build a trade services platform, Rob responded:

“So I think it's a huge opportunity. And I didn't mention this, I should have, this is like maybe my third aggregator model. The first couple were reasonably successful, hit about $1 billion in valuation in about 4 years. And so I think it really depends how much we want to go for it.”

—Rob Casper, CEO of Bud’s Plumbing, Kingsway’s 2025 Investor Day

So, let’s get this straight. Rob already has experience in helping roll up two trade service businesses for private equity firms. One (or both) hit nearly $1 billion in valuation in just four years. If Rob, with the help of Kingsway, even reaches just one third of those prior $1 billion valuations he helped achieve, this alone would represent nearly all of Kingsway’s current market cap even after the recent run-up in share price from $7 to $12. This alone might be all the evidence needed to explain recent run in the share price of Kingsway.

The last catalyst for Kingsway is its belief it will soon be able to self-fund future acquisitions. With a sale (or several sales) of a business and having a larger number and variety of cash-flowing service businesses to up-stream excess capital to Kingsway, these two factors will contribute greatly to the goal of eliminating the need for raising additional capital. The attractiveness of the business model will be that much greater.

Summary

Change is afoot at at Kingsway, a search fund in public company clothing. Concentrated shareholder ownership is now a bit more dispersed. There are two new and highly reputable board members. All signs point to the company soon turning into a self-funded, pure-play concept. It shouldn’t be a surprise the share price has recently broken out of a long, two-plus-year range-bound trading pattern. The market is finally picking up what Kingsway has been putting down.

Further Reading & Listening

2024 - Kingsway Investor Day - includes a fireside chat with Will Thorndike at the end

2025 - Kingsway Investor Day - includes a fireside chat with former Danaher CEO, Tom Joyce

Please Share and Subscribe

If you enjoyed this content, please share and subscribe. Leave a comment as well if you have the time!

Disclaimers for this Substack

The content of this publication is for entertainment and educational purposes only and should not be considered a recommendation to buy or sell any particular security. The opinions expressed herein are those of Douglas Ott in his personal capacity and are subject to change without notice. Consider the investment objectives, risks, and expenses before investing.

Investment strategies managed by Andvari Associates LLC, Doug’s employer, may have a position in the securities or assets discussed in any of its writings. Doug himself may have a position in the securities or assets discussed in any of his writings. Securities mentioned may not be representative of Andvari’s or Doug’s current or future investments. Andvari or Doug may re-evaluate their holdings in any mentioned securities and may buy, sell or cover certain positions without notice.

Data sources for all charts come from SEC filings, Koyfin, and other publicly available information.

Huh. I just read about the company in Scott Miller's (Greenhaven Road) quarterly newsletter. It's a company with an interesting business model.