Ingredion

A Low-Multiple, High Value-Added Business Near Inflection

Having recently embarked on a journey to reduce investment concentration and increase diversity, I’ve added a handful of names to my investment portfolio. One of the names is Ingredion (INGR), one of a few names to increase my exposure to the broad consumer staples sector.

I’ve kept tabs on the company since I became an investor over 15 years ago and when the company was still called Corn Products International (CPI). The name change to Ingredion came after CPI acquired National Starch from AkzoNobel in 2010. This was to reflect its broader focus on ingredient solutions rather than just corn-based products.

A full history of this business is a series of posts I’ll save for later, but I’ll say for now Ingredion is the longest listed food product company on the NYSE. Its predecessor company originally debuted on April 24, 1902, as the Corn Products Company.

The Business

Ingredion today is a global ingredient solutions company that turns corn and other plant-based raw materials (e.g., tapioca, potato, rice, stevia, peas) into starches, sweeteners, texturizers, and other specialty ingredients used across food, beverage, brewing, animal nutrition, and selected industrial markets. While the company still has meaningful exposure to more traditional starch and sweetener categories, its strategy has increasingly focused on higher-value, more differentiated applications such as clean-label texturizers, sugar reduction, texture systems, and protein fortification. That gives Ingredion a business model that sits between a commodity processor and a specialty ingredients supplier: raw materials and plant reliability still matter, but long-term value creation depends more on mix shift, customer formulation partnerships, and steady growth in specialty solutions than on pure agricultural cycles.

Ingredion reports three main operating segments plus an “All Other” category. Texture & Healthful Solutions is the company’s most differentiated business, serving global and regional customers with specialty starches, clean-label ingredients, hydrocolloids, and customized systems that generally carry higher margins and better growth prospects. Food & Industrial Ingredients LATAM and Food & Industrial Ingredients U.S./Canada are more locally focused businesses built around starches, sweeteners, and co-products, with a greater mix of commodity-linked products and stronger sensitivity to plant utilization, input-cost pass-through, and regional demand conditions. The All Other segment includes businesses such as PureCircle stevia, sugar reduction ingredients, pea protein, and the Pakistan operations.

For investors, the key segmentation point is that Texture & Healthful Solutions increasingly drives the quality of earnings, while the two Food & Industrial Ingredients segments still provide much of the company’s cash flow but carry more operational and cyclical variability.

The Cons?

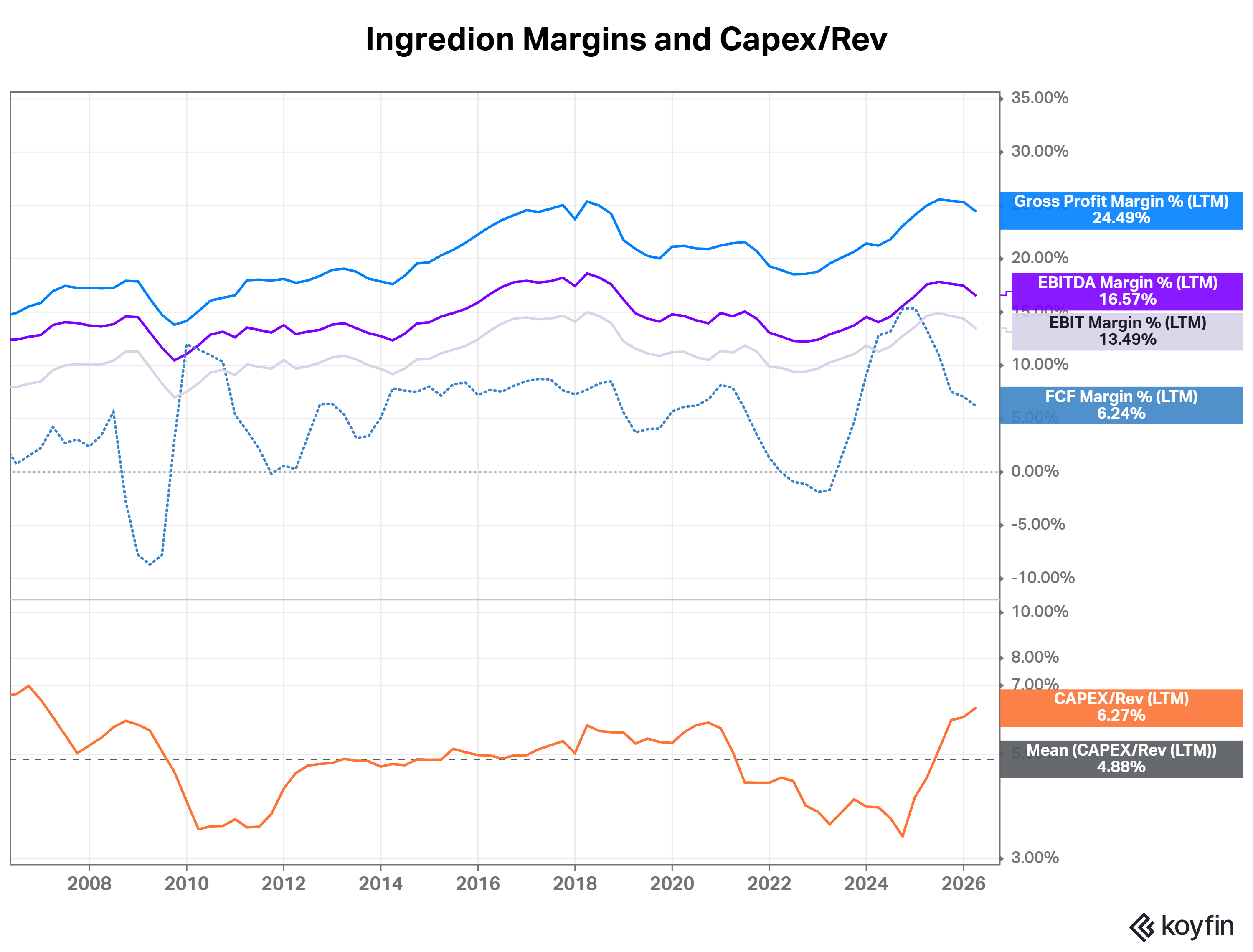

From a growth and margin/returns perspective, Ingredion is not an exciting business. First, it’s a low-growth business. Meaningful revenue growth has come through M&A. Ingredion also has relatively high capex requirements relative to sales—the average has been 4.9% over the last ten years. Ingredion’s business is also taking the most basic of raw agricultural materials and processing them into more useful end products. Margins—especially gross and free cash margins—are low and have a degree of occasional volatility, especially compared to all the other businesses that are available to an investor.

The Pros

There are positive offsets to most of the negative attributes I just mentioned. First, just because this might be a low-growth business does not mean it can’t produce good shareholder returns. The business is quite stable in terms of the demand for its products. Ingredion sells essential value-added inputs to customers who need it for their own branded food products. And although Ingredion might be at the whim of the commodity prices of its agricultural inputs, they offset most of this with hedging.

Further, although margins might be low, and capex requirements higher than some investors might find acceptable, Ingredion has low leverage, a low multiple, and a nice dividend yield, all of which can lead to good compounding over the long run. Ingredion currently trades at the lowest EV/EBITDA multiple since 2009-2010 despite having improved its margins meaningfully since then.

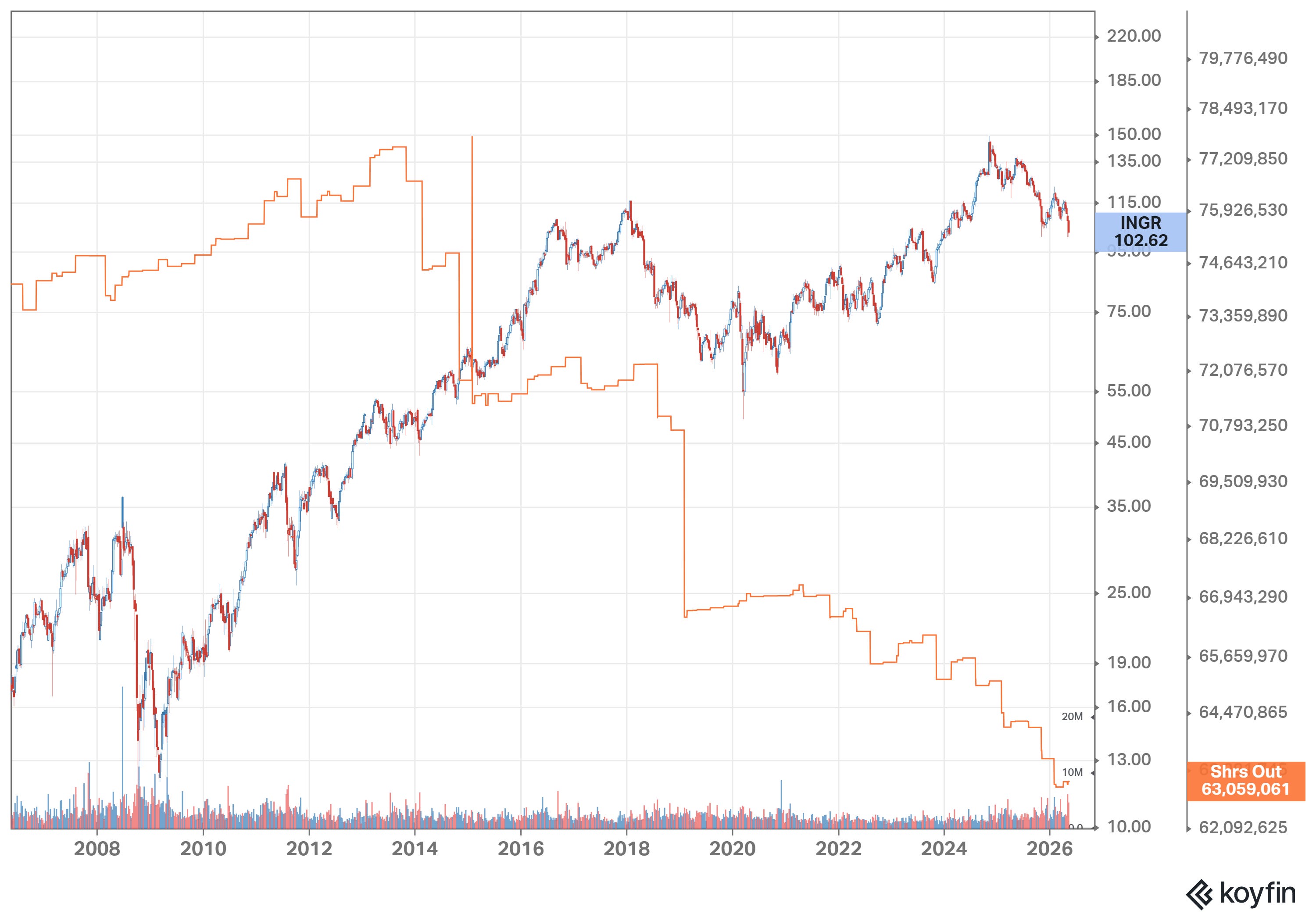

Ingredion has also been a good repurchaser of its shares. Since August 2013, the share count has declined from 77.5 million to 63.1 million.

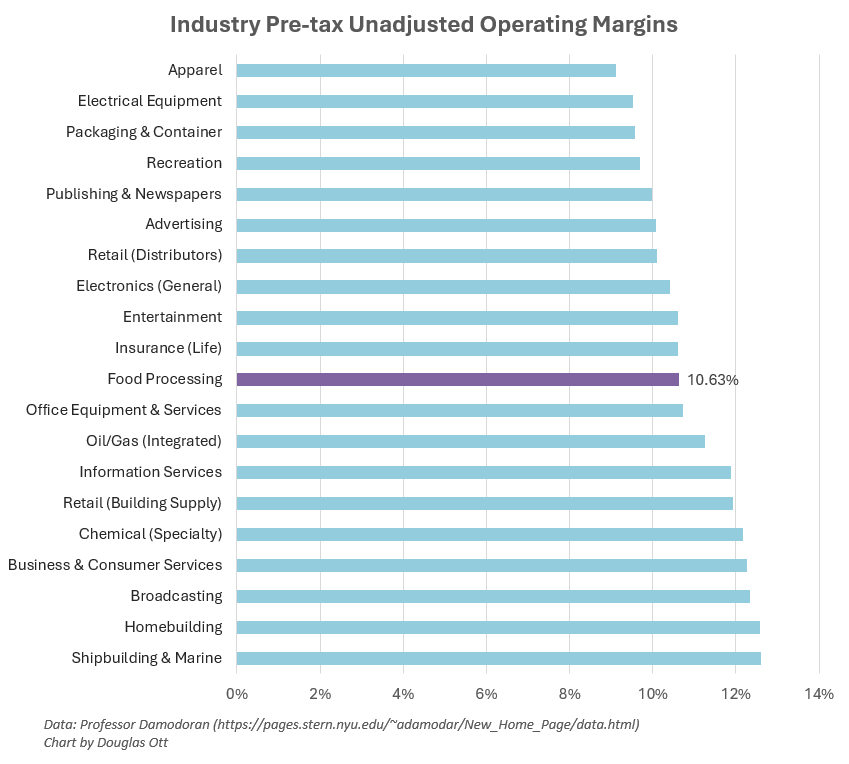

On the issue of margins, let’s add some context with Damodoran’s industry datasets. On pre-tax unadjusted operating margins (latest data as of January 2026), the chart below shows the Food Processing industry in relation to ten other industries above and below its 10.63% margin. The margin for the total market (excluding financials) is 13.14%. So the Food Processing industry is a bit below the market average here, while Ingredion’s operating margins have ranged from 11.9% and 14.4% since 2023.

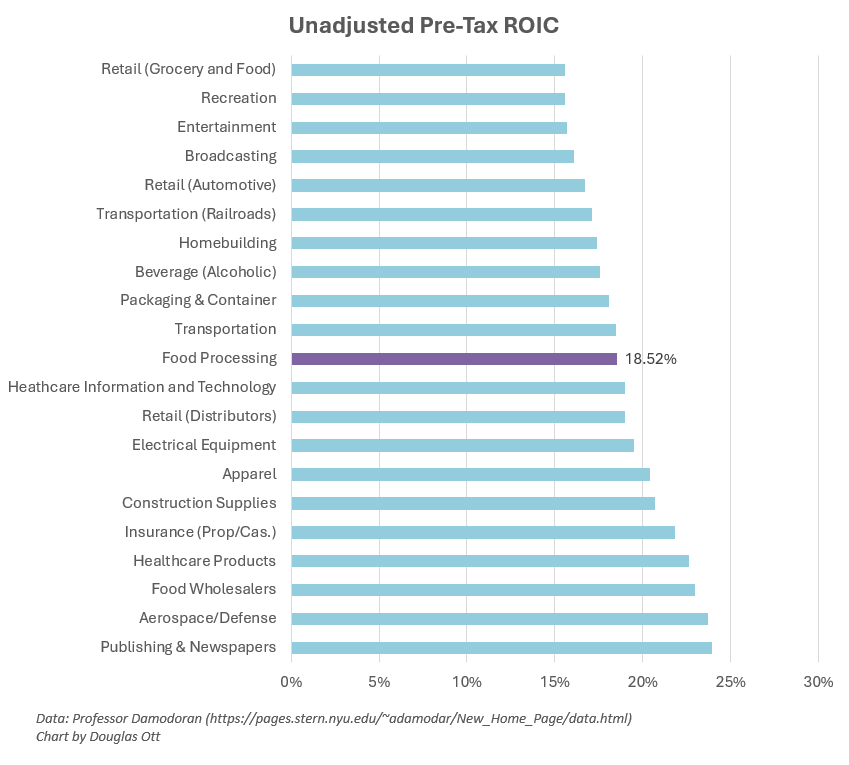

On unadjusted pre-tax ROIC, the Food Processing industry returns in relation to the immediate industries surrounding it. As of January 2026, the Food Processing industry had a pre-tax ROIC of 18.52% while the total market (ex financials) had a pre-tax ROIC of 20.37%. Again, this is slightly less than the market. However, perhaps this should be impressive given the market’s figure has been skewed upwards by the financials of industries like software, IT, and semiconductors. Again, not terrible results, but not the best of the best either.

Inflation Protection

Another interesting thing for a business like Ingredion is its inflation protection potential. Horizon Kinetics has written extensively about inflation and have even put their thoughts into practice with their Inflation Beneficiaries ETF (INFL). Outside of the asset-light royalty companies and financial exchange businesses, Horizon has written about how they also like large-scale grain and seed processing companies like Archer Daniels Midland (ADM) and Bunge (BG).

First, ADM and BG enjoy long-term secular demand for their products. Over time, more people are eating more calories from a wider variety of foods (and increasingly snacks). As Horizon Kinetics writes, ADM and BG are “defensible businesses and earn a spread on throughput that tends to widen as prices increase.”1 In general, it is fair to say this industry does act like a tollbooth on global food supply. For ADM and BG in particular, they are also exchange-like businesses where they earn a spread. In the case of securities and futures exchanges that earn revenues and profits by facilitating transactions and earn the difference between the bid/ask spread on those transactions, ADM and BG earn their keep based on the difference between the value of the input and the processed output. And when prices increase, the spread that ADM and BG can capture widens.

Ingredion sits somewhere adjacent to ADM and BG. Ingredion is the higher quality company relative to ADM and BG because it focuses on higher margin products, attempts to neutralize commodity volatility, and attempts to pass on costs to customers. On the other hand, Ingredion is also a business that provides less inflation protection compared to ADM and BG. These two large businesses are capturers of spread and benefit much more when their spread widens due to ag price volatility (i.e., what it costs to buy a crop vs. what they can earn processing or merchandising it). But still, with Ingredion’s greater stability and predictability, higher margins and returns, and its faster growing Texture & Healthful Solutions segment, it ought to be considered the superior business over a long period of time relative to ADM and BG.

Ingredion Comps

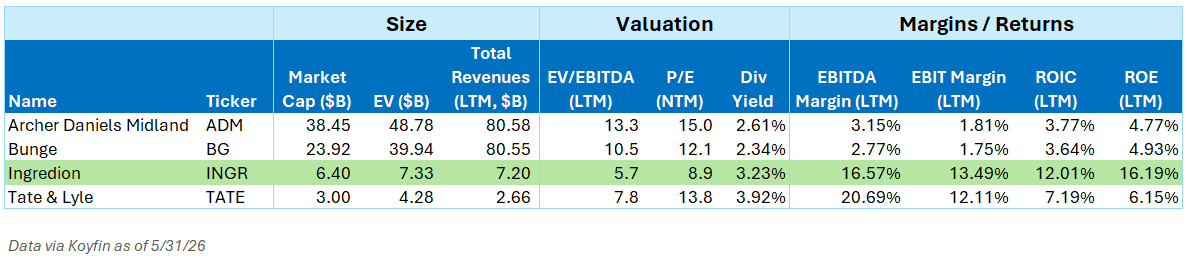

By comparing Ingredion against its two much larger competitors, Ingredion’s valuation, margins and returns stand out. It has both superior margins and returns combined with a very low valuation.

Despite looking superior on paper, Ingredion’s total returns to shareholders have lagged ADM and BG over the last 5 years thanks to both ADM and BG being up 40% YTD in 2026 and Ingredion’s total return being -6.6% YTD in 2026.

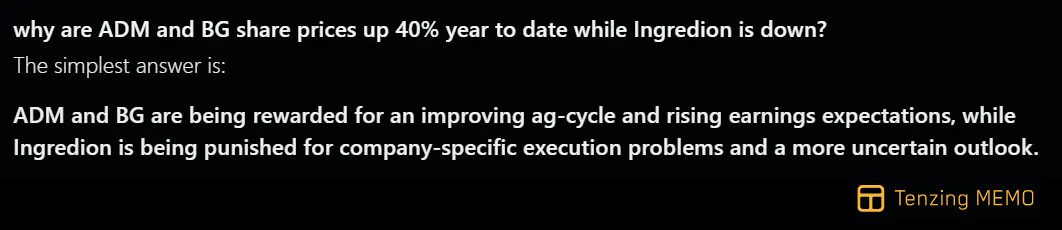

Using Tenzing MEMO, an “AI-first” research assistant I continue to evaluate, I basically asked, “What is going on here?”

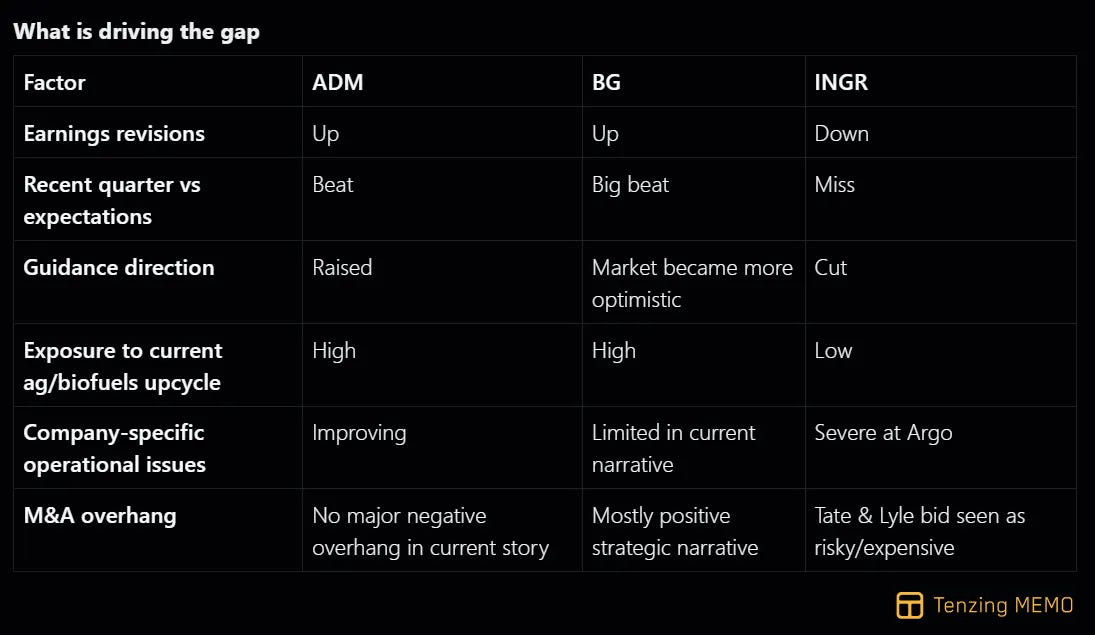

The simple answer was ADM and BG have been rewarded this year for “improving ag-cycle and rising earnings expectations, while Ingredion is being punished for company-specific execution problems and a more uncertain outlook.” Tenzing went into many more details behind this and also provided a nice summary chart showing what has likely driven the gap in recent share performance:

Ultimately, ADM and BG have simply beaten expectations over the last five months while Ingredion has missed expectations. So, what are the specific reasons Ingredion has missed expectations? One reason is the operational issues at its Argo plant.

Argo: Don’t You Want to Know How We Keep Starting Fires?

The big reason for Ingredion missing expectations is the ongoing issues at its Argo plant in Bedford Park, IL, south west of Chicago. Towards the end of Q2 2025, a fire happened at the plant and halted the entire production. Argo is one of Ingredion’s largest plants in their network and accounts for more than 40% of the net sales of its Food & Industrial Ingredients segment. Management first addressed the fire in its Q3 2025 call and they estimated the negative impact to operating income would be $22 million for 2025. In Q4 2025, management then said the impact for FY 2025 was much larger: approximately $40 million rather than $22 million. They also estimated an additional $10 to $15 million of costs would affect the upcoming Q1 2026.

During the Q1 2026 call this May, Ingredion again had to report ongoing difficulty with fixing the plant. Rather than $10-$15 million of costs, it was $40 million of costs, comprised of higher maintenance spending and costs related to rework. Finally, on April 10, 2026, there was a separate “thermal event” at Argo’s corn germ processing unit which knocked that part of the facility’s crude oil production offline…

The problems at Argo have been real and have gone on far too long for the short-lived patience of most investors.

Aside…

The title to this subsection is a reference to the lyrics of the song “Danger! High Voltage” by American rock band Electric Six.

Bid For Tate & Lyle

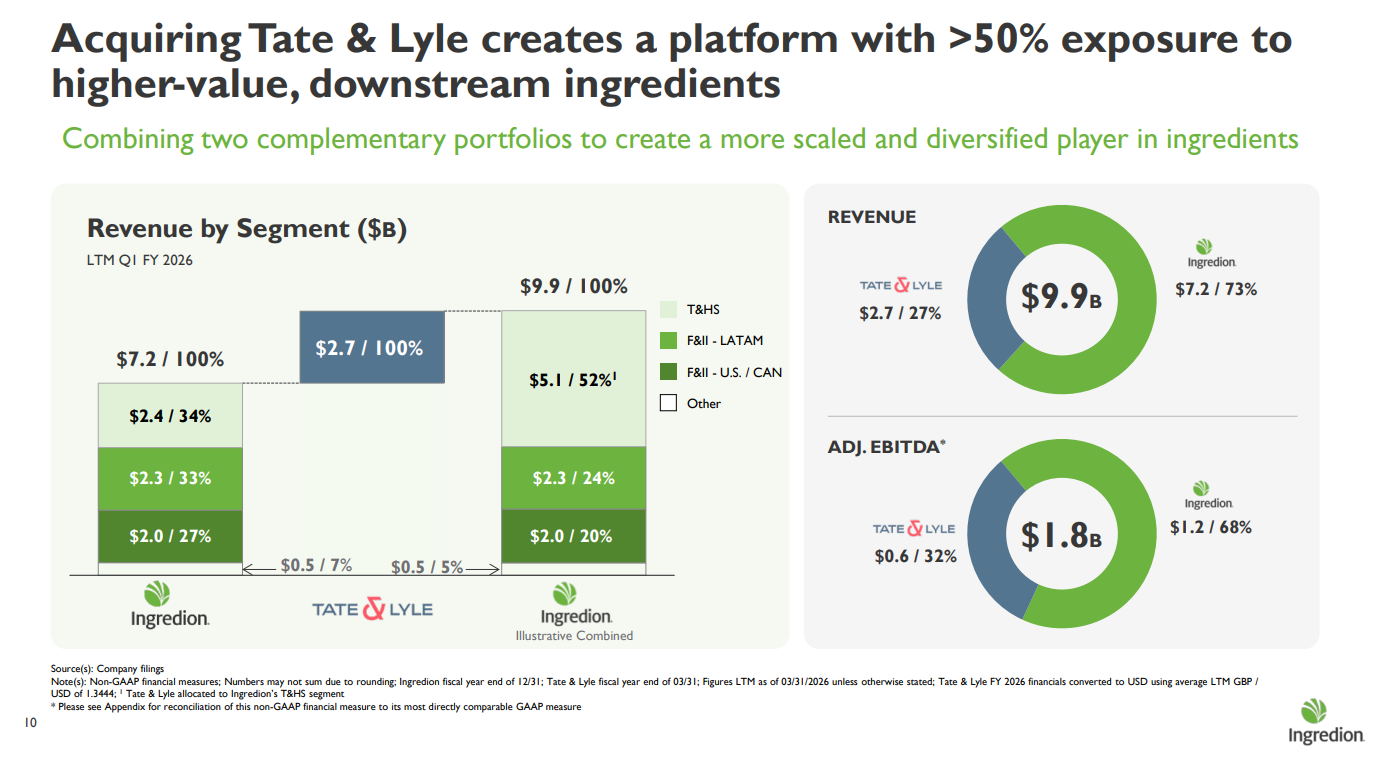

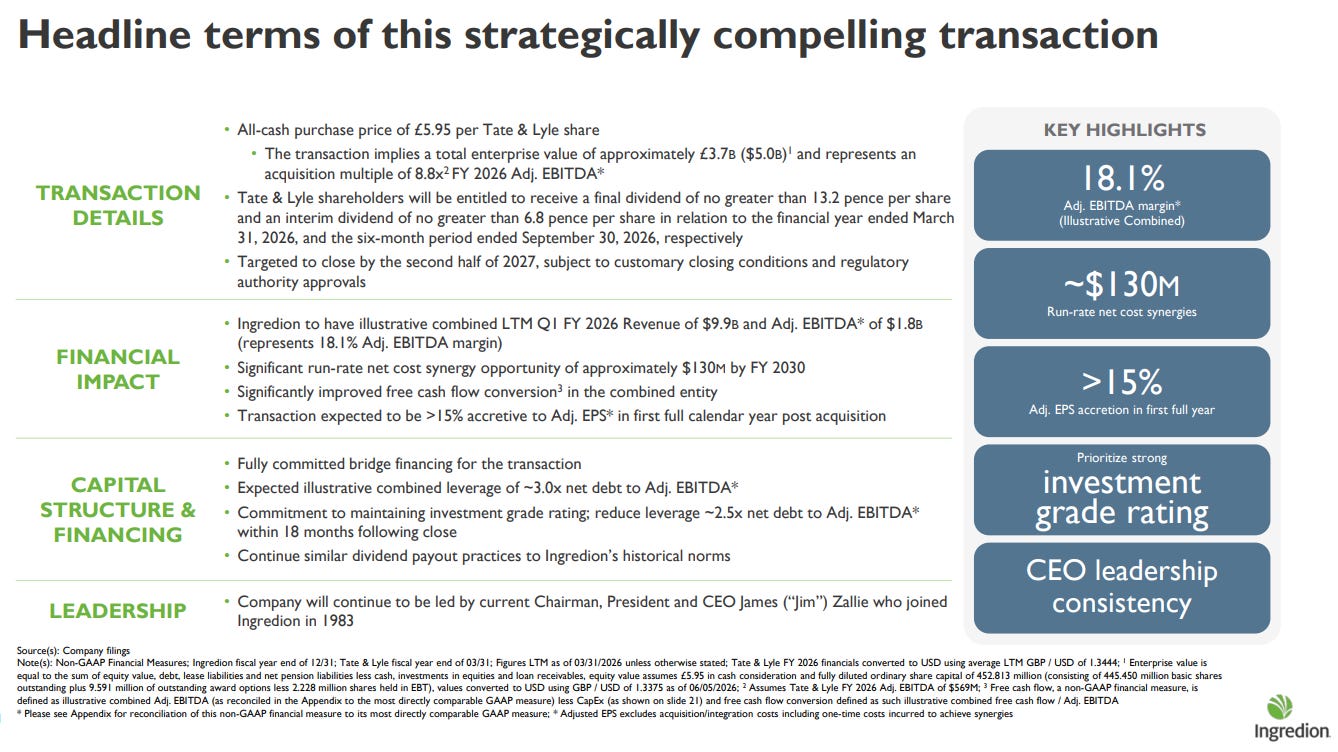

The second item affecting INGR’s share price is their bid for UK-based competitor Tate & Lyle which was first reported on May 14, 2026. The acquisition of T&L is an opportunity to grow Ingredion’s higher-margin and faster-growing Texture & Healthful Solutions segment. Initially, the news reported the bid valued T&L at $3.7 billion (£6.15) or about 8.9x EBITDA, and that Ingredion had until June 11 to make a firm offer.

Ingredion did indeed make a firm offer on June 8: an all-cash purchase price of £5.95 per share for an acquisition multiple of 8.8x EBITDA.

As with any significant acquisition, there are risks when it comes to integration and leverage. First, T&L would be a large acquisition, but not enormous. In terms of revenues, T&L is currently 36% the size of Ingredion. Second, with T&L’s higher leverage ratio (2.3x net debt to EBITDA), Ingredion’s own leverage would necessarily increase from 0.7x to ~3.0x. After the deal closes in the second half of 2027, Ingredion says they will be able to reduce leverage to 2.5x within 18 months. This leverage does not seem that great for a steady and dependable business.

The deal makes sense from a strategic perspective, but I don’t yet have a good sense of whether Ingredion would be paying a fair price or an expensive one. Ingredion’s pro forma growth and margins will be better when more than 50% of its revenues coming from its Taste & Healthful Solutions segment. There is also room to improve T&L’s much lower returns on equity and invested capital suggest—ROE for Ingredion is 16.2% vs. 6.2% for T&L. Ingredion also states it can achieve $130 million of synergies by 2030.

I must say that Tenzing MEMO was extremely useful in this situation of getting back up to speed on a company on which I had only basic knowledge. I saved at least a dozen hours of time playing catch-up with Tenzing’s help. Tenzing provided not just the basic facts, but created an intelligently structured narrative with additional context that I would have naturally asked for in follow-up queries.

I wrote about Tenzing MEMO last year and it has only continued to improve. Even more interesting is their recent announcement about how they’ve introduced coverage of hundreds of Canadian equities from the Toronto Stock Exchange…

An AI Journey to Improve My Investment Process

The life sciences industry is one I’ve followed over the years since Danaher’s acquisition of Beckman Coulter back in 2011. I keep tabs on Danaher and most of the other companies in the industry: Thermo Fisher, Sartorius, Agilent, Repligen, Revvity (formerly Perkin Elmer), Bruker, Waters, Bio-Techne, and Waters. Needless to say, it takes a lot of time t…

Ingredion’s Future

Ingredion has been on a long and steady journey to improve margins, returns, and its growth profile. It’s done this by becoming a business that does more than just process corn and commodities. Rather than chase the size and business models of Archer Daniels Midland, Bunge, and Cargill (still private), Ingredion has focused on the smaller niches where customers are willing to pay a premium.

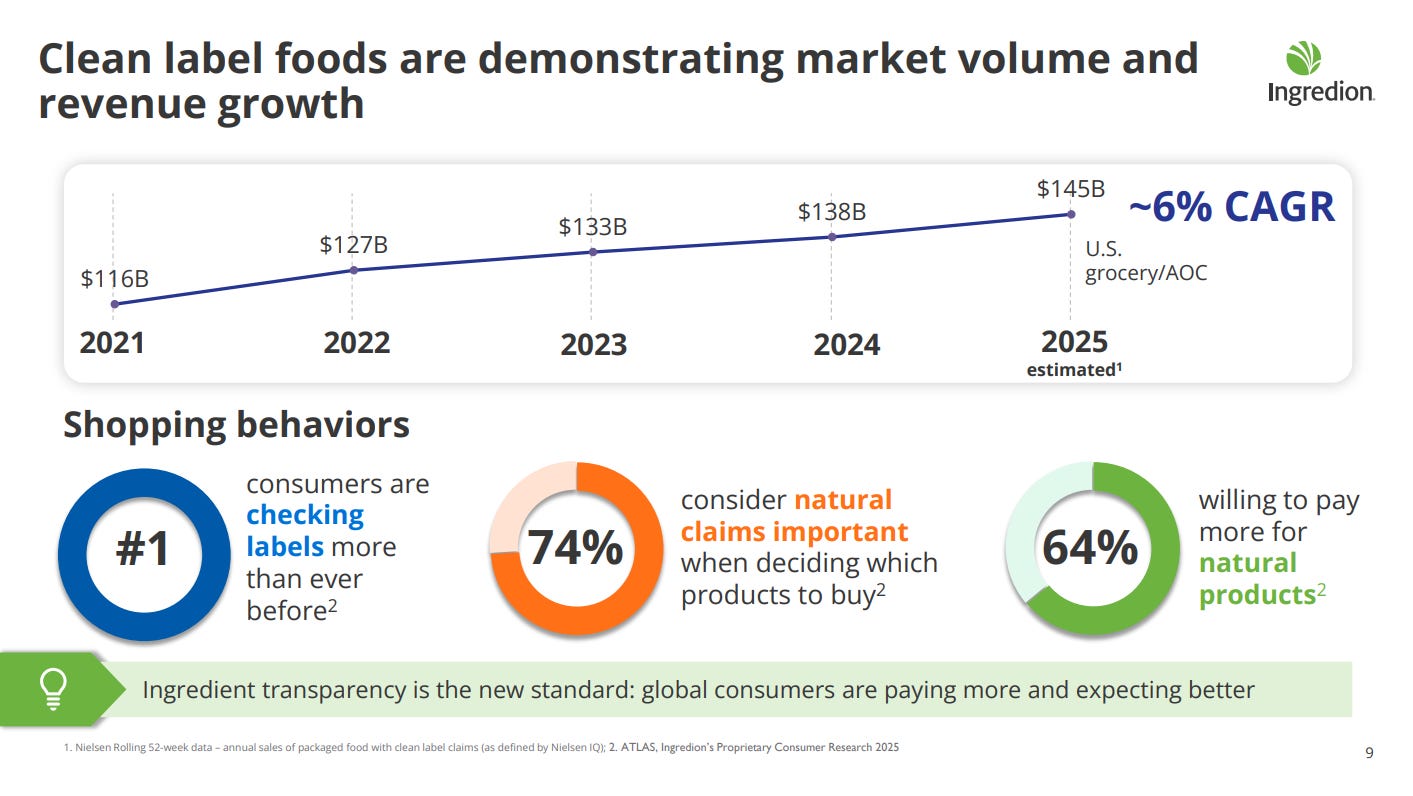

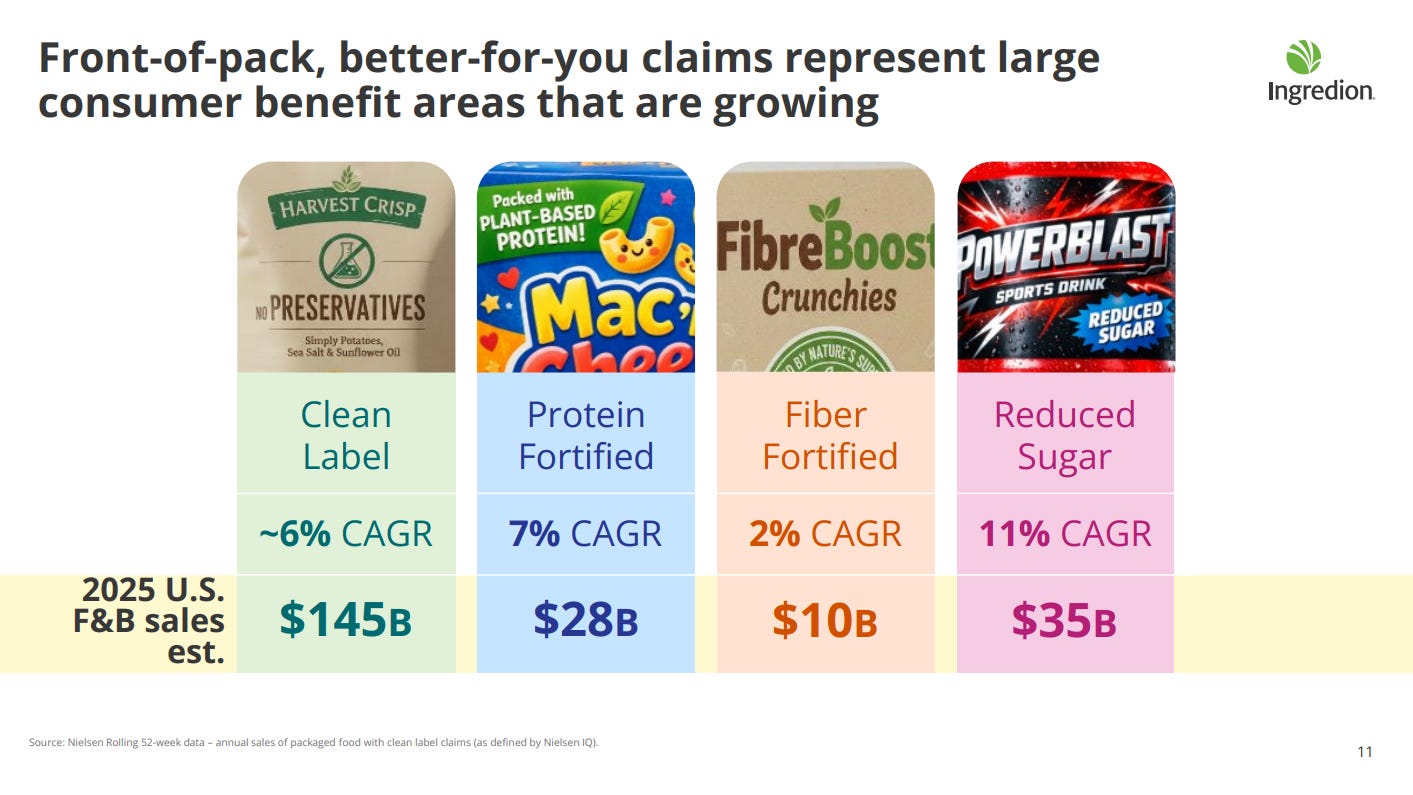

For example, many of Ingredion’s products can help its customer make “Clean Label” claims. A food with a Clean Label claim means it uses a short list of simple, recognizable, and wholesome ingredients while avoiding artificial additives and synthetic chemicals. Ingredion’s products can also aid with sugar reduction, mouthfeel and texture, and protein and fiber fortification. These are all trends that a growing number of consumers care about.

Summary

Ingredion is a boring, stable business that provides the increasingly specialized ingredients needed to make our food taste better and to be healthier. As a public company, Ingredion trades at a multiple so low it hasn’t been seen since 2009/2010. The problems at the Argo plant will eventually be fixed. The bid for Tate & Lyle might be a bit expensive, but it does make sense. It seems to me there is much too pessimism surrounding the company.

At a 5.7x EV/EBITDA multiple and a 3.3% dividend yield, Ingredion seems like a stock that can produce good forward returns. To boot, it has a definite catalyst for multiple expansion: its Argo plant is a problem that will eventually be remedied, and Tate & Lyle could turn into a great acquisition.

Please Subscribe and Share

Please share if you have found this post interesting and illuminating. Make sure to subscribe so all future posts find their way to your inbox.

Disclaimers for this Substack

The content of this publication is for entertainment and educational purposes only and should not be considered a recommendation to buy or sell any particular security. The opinions expressed herein are those of Douglas Ott in his personal capacity and are subject to change without notice. Consider the investment objectives, risks, and expenses before investing.

Investment strategies managed by Andvari Associates LLC, Doug’s employer, may have a position in the securities or assets discussed in any of its writings. Doug himself may have a position in the securities or assets discussed in any of his writings. Securities mentioned may not be representative of Andvari’s or Doug’s current or future investments. Andvari or Doug may re-evaluate their holdings in any mentioned securities and may buy, sell or cover certain positions without notice.

Data sources for all charts come from SEC filings, Koyfin, and other publicly available information.

“Right Place, Right Time”, Value Investor Insight, April 30, 2022. <https://horizonkinetics.com/app/uploads/Davolos-VII-Reprint-FINAL-APPROVED-05-11-22-KINE2022050083.pdf>