Expert Interview on the 180-Year-Old Business of Lindt & Sprüngli

How to View a Consumer Staples Business

The Preferred Shares podcast recently interviewed Mark Purdy, a veteran investment analyst who has focused on consumer brands over the last forty years, about Swiss chocolatier Lindt & Sprüngli.

Lindt is the embodiment of the phrase “consumer staple” as it was founded 180 years ago and has withstood the test of time. By no means did I have Purdy’s knowledge and experience, of Lindt in particular or consumer stapes in general, so this was an excellent and illuminating interview conducted by myself and my co-hosts Lawrence Hamtil and Devin LaSarre.

Here are a few key quotes and concepts that I thought were most important.

Separating the Wheat from Chaff

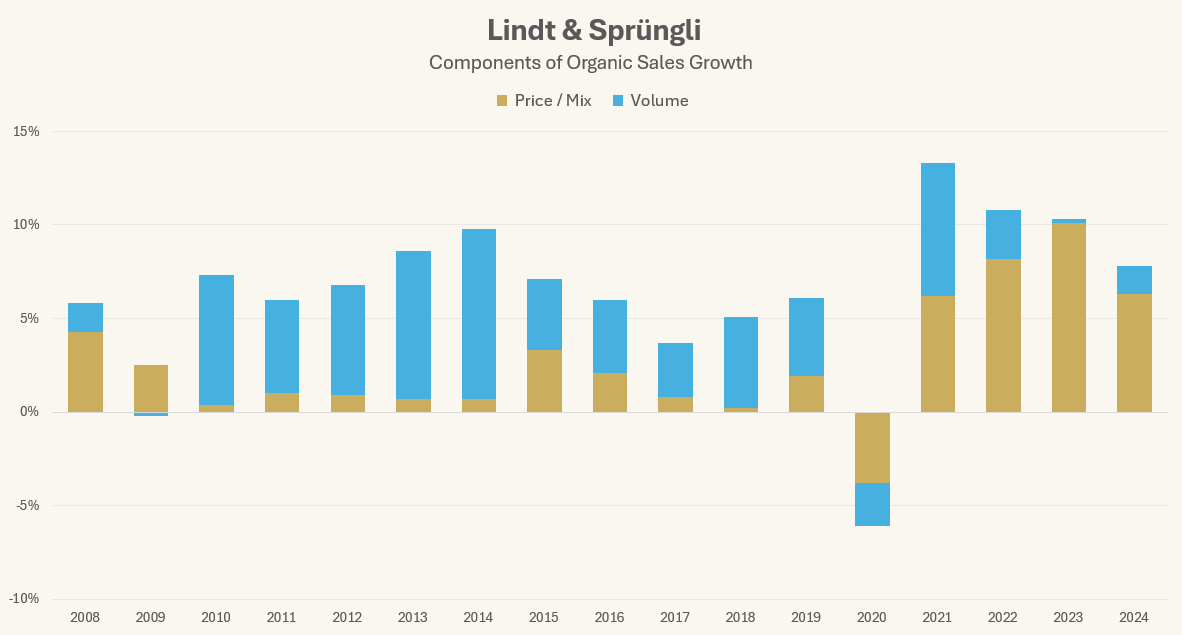

Mark’s prime criterium for identifying attractive consumer staples businesses is whether or not it is capable of growing its sales over a long period of time. He starts by looking at the prior decade’s growth (emphasis mine):

[F]or me, very much the starting point is, the company capable of growing its sales over an extended period of time? And that's not like for like or organic sales growth. This is very much dollar or in the case of Lindt & Sprüngli, Swiss franc sales growth. So done in a proper currency. And my starting point to looking at a company would always be start today, go back 10 years and look at the sales line. And if you've doubled sales in 10 years, which is a pretty tough metric, then it's definitely interesting. Even if the sales are at 50 % in 10 years, it's potentially quite interesting.

And then you dig deeper into: how have they been able to do it? Have they been able to buy other businesses? We generally think if you can add brands along the way, that's a good thing. And then you want an attractive, but not necessarily super high gross margin, and then a sensible, without being excessive, operating margin. And then you're into things like the culture and the people. But the starting point is always, has this business been able to grow its sales over an extended period of time? And if it has, we always think you've got a pretty good chance of that repeating in the future, rather than one that's gone nowhere for a decade and you'd have to say, “Well, why is it going to be any different in the next decade?”

Raising Prices Above Inflation is Not Sustainable

Another important insight, although it is obvious when you sit down and think about it, is that a consumer brand (with the exception of tobacco) can seemingly never raise prices on their products above inflation rates for a long period of time (emphasis mine):

We did a study back in our Deutsche Bank days where we showed … that in static terms, they have amazing pricing power, which is why you can make gross margins of 60% up to 80% depending on the category. But it needs to be backed by a healthy amount of advertising spend, which is effectively persuading consumers to pay two, three, four times what it costs you to make this product.

But what also became clear … is that to raise prices above the rate of inflation on a sustained basis is simply not possible. I mean, if you took a very simple proposition like a can of Coke, if you priced it above inflation for 25 years in the US or any other developed market, it's clearly not going to work. I mean, eventually it become ridiculously priced. I know in the case of cigarettes, but tobacco being addictive is a very different area. But in every other consumer category, you are not going to be able to price above inflation. And if you do, what you find is that the volume starts to come under pressure. And our view is that at some point that will result in initially higher and higher margins, but ultimately a reset on margins where the company has to address the loss of share and/or the category decline.

So, in almost every consumer category outside of tobacco, it is typically unsustainable for a company to raise prices above inflation for many years. It will eventually bite the company in the ass and the outsized profits they earned in the short-term will evaporate as volumes decline when consumers find other substitutionary products that fit their needs and their budget.

The Great Misconception About Grocers

This next quote was a follow-on to the benefits of Lindt having its own specialty stores to sell its wares, but it is a bit of knowledge regarding the grocery business about which I was unaware: private label brands aren’t necessarily better for the bottom line of grocers and food retailers…

And one of the great misconceptions I think about grocers/food retailers relative to consumer goods businesses is that a lot of people think, well, the grocer will make more money out of a private label product than it will out of a branded product. That's not necessarily the case. They often make a bigger cash profit out of a Lindt chocolate bar or Nescafe or something like that than they do out of the private label. The percentage may be lower, but for the retailer, the key equation is your cash profit per square foot, which is also then a function of the stock turn. So products that turn quickly with good cash profits in absolute terms are more attractive than a high percentage, slower turning, potentially private label product.

Different Businesses Can Be Equally Great for Different Reasons

As I was quite sick and coughing quite a bit when Preferred Shares recorded the Purdy interview, I only managed a few questions of my own. One of my questions was about whether the business qualities possessed by Lindt—focus, quality, consistency—were the ideal qualities that should be sought after by all consumer staples companies. Or for any company in any industry for that matter.

Purdy’s answer was a slight surprise to me (again, I’m the neophyte in this business sector), but well considered with his 40 years of experience:

So focus and quality and consistency, absolutely. I totally agree in terms of Lindt. The one thing that Mondelēz has that Lindt doesn't have—and this is true also of where we think large FMCG companies have a role to play from an investment perspective— is that the better emerging market businesses tend to be owned by the major public companies. So Unilever 60% of its sales are from emerging markets. But Hindustan Unilever as a company has been around for 100 or so years. These are deeply embedded companies in places like India where the per capita consumption opportunity is enormous. So Unilever wouldn't qualify in terms of necessarily focus or consistency with its ten CEOs in 40 years, but it does have a footprint that most other companies can only envy.

And in fact, Mondelēz through Cadbury has a similar—nowhere near as good—but has a footprint to some of these emerging markets. And Proctor, which was quite a long way behind, has built a good business in a number of, not quite as many as Unilever, but a number of emerging markets as well. Nestle clearly has a deeply embedded presence in a lot of emerging markets.

So in a world where people are concerned around tariffs, the global consumer goods companies are frequently, yes, they're present around the world, but they're not trying to ship stuff from one country to another. They're by and large operating and producing locally for those local consumers, often because when it's food type businesses, it's local taste that drives where you can operate and how many different countries you can sell to. So the bigger you are, you clearly are not going to have the same focus, but you do end up with, hopefully, other strengths…

Thinking back on this particular question of mine, I can only think that is was both good and bad—or at least uninformed. It was good in that it unearthed the obvious distinction that good companies can be good for different reasons. My faux pas was thinking that there are a few immutable qualities that can lead a company towards the holy grail of greatness. But after listening to Mark, I think I am now am more open to the fact that different companies or industries—from a qualitative standpoint—can be great for different reasons.

The interview with Mark Purdy was outstanding and I learned a lot from a professional investor with multiple decades of experience. There’s lots more interesting stories and anecdotes from the interview and I highly recommend you give it a full listen!

Please Share and Subscribe

If you enjoyed this content, please share and subscribe.

Disclaimers for this Substack

The content of this publication is for entertainment and educational purposes only and should not be considered a recommendation to buy or sell any particular security. The opinions expressed herein are those of Douglas Ott in his personal capacity and are subject to change without notice. Consider the investment objectives, risks, and expenses before investing.

Investment strategies managed by Andvari Associates LLC, Doug’s employer, may have a position in the securities or assets discussed in any of its writings. Doug himself may have a position in the securities or assets discussed in any of his writings. Securities mentioned may not be representative of Andvari’s or Doug’s current or future investments. Andvari or Doug may re-evaluate their holdings in any mentioned securities and may buy, sell or cover certain positions without notice.

Data sources for all charts come from SEC filings, Koyfin, and other publicly available information.

Great interview! It’s been out a few days and already on my second replay. Lots of really good/important takeaways.