How to Sell Zithers to the Mormons

Arthur J. Gallagher's Sales Culture and its Next Big Acquisition

Culture can trickle or filter down—or whatever metaphor you want to use—from the top of a group to the bottom. This symbolic language is entirely inappropriate when it comes to Arthur J. Gallagher & Co. (AJG), one of the largest insurance brokers in this country. The tone of management at Gallagher consistently exudes excitement and passion for helping their customers deal with risk. The culture is undeniably sales-centric and customer-focused.

In fact, Gallagher’s culture is enshrined in a list of 25 shared values. And the first on the list is this:

“We are a sales and marketing company dedicated to providing excellence in risk management services to our clients.”

This is an ethos that pours down from the top managers and fully washes over every one of the 52,000+ Gallagher team members around the world.

Whatever it Takes

Arguably, the culture began even before Arthur Gallagher started his insurance broking company in 1927. Arthur’s father, Jack, immigrated to Chicago—all by himself, no more than 10 years old—in the 1860s or 1870s. Jack eventually became a traveling salesman with the ability and drive to sell nearly anything.

There’s an illustrative Jack story in Allison Kitrell’s book about Gallagher (the company) that is impossible for me to ever forget:

As a young man, Jack became a salesman, beginning a Gallagher tradition of sales. In fact, decades later his grandsons, owners of one of the largest insurance brokerage companies in the world, would refer proudly to themselves as “peddlers.”

Jack Gallagher was an impressive salesman, with a certain amount of wanderlust. A photo shows him in Dallas in the 1870s, for example, and he also spent time in Salt Lake City.

His experience in Salt Lake City showed his keen understanding of the importance of knowing your customer. He was selling zithers, and he discovered that it was very hard for an Irish Catholic immigrant to sell zithers to the largely Mormon population of Salt Lake City. So he became a Mormon—and sold a lot of zithers. Later, when he left Salt Lake City, he converted back to Catholicism.

Not that Jack, or his sons or grandsons, would literally do anything to make a sale. But this example is emblematic of a deep desire to do whatever it takes to make a personal connection, to understand the customer and their needs, and to provide excellent service. Although Jack had no explicit part in the founding of his son’s brokerage firm, he is still truly a part of today’s AJG, still helping drive its success and growth.

A Big Acquisition

On December 9, 2024, AJG announced its agreement to acquire AssuredPartners for a gross consideration of $13.45 billion. Prior to the announcement, AJG had a market cap of $65.1 billion and a trailing twelve month adjusted revenue of $11.1 billion and adjusted EBITDAC of $3.7 billion for their Brokerage & Risk Management segments. Assured had $2.9 billion of TTM 9/30/2024 pro forma revenue and $938 million of TTM 9/30/2024 pro forma EBITDAC (EBITDA before the change in estimated acquisition earnout payables). Thus, AJG is paying a multiple of 14.3x of EBITDAC for Assured. AJG’s EBITDAC multiple before this announcement was in the high-teens.

With AJG likely issuing a hefty $8.5 billion in new shares (about 63% of the total purchase price) to help finance this deal, AJG’s stock has declined from all-time highs of $315 to now $281.

AJG’s Remarks on the Acquisition

One of the more interesting remarks on AJG’s recent call is they firmly believe the acquisition will provide more opportunities to more people. AJG fully recognizes the value of the franchise AssuredPartners has built. Likewise, AssuredPartners fully recognized that AJG is the acquirer that can help them and their producers get to the next level, faster:

Mark Hughes

And the other part of that was just employee retention at AssuredPartners.

J. Patrick Gallagher

Well, that’s a really key thing here, Mark. You’ll notice that in the details, our integration savings, $160 million is not coming from laying a lot of people off. That’s not the gist here. Gallagher in the United States probably has to hire 5,000 people a year just to keep up with our turnover at the present state that we’re in now. So with this addition of these people, we’re getting a great group of people that looks just like Gallagher about 12 years ago.

Systems are different around with the branches they bought, et cetera. And there’s a very deep understanding on their part that integration of their systems and the like is necessary. So we’re actually giving them a path forward that is additive to all the work that they’ve already done. So this is not about finding a lot of jobs to let people go. Quite the opposite.

We are viewing this as a better opportunity for everybody. We’re telling our leadership team, “Get ready. Your job is growing.” We’re telling their leadership team, “Get ready, your job is growing.” We’ve got lots of needs for good solid people in this company, and this is not about synergizing our jobs.

…

And culturally, Mark, I think you understand the culture quite well. This is a very producer-centric organization. They get up just like us every morning thinking about what do we sell today? What accounts are we keeping? What are we growing? Who’s the new account on the list? And it just fits very, very naturally.

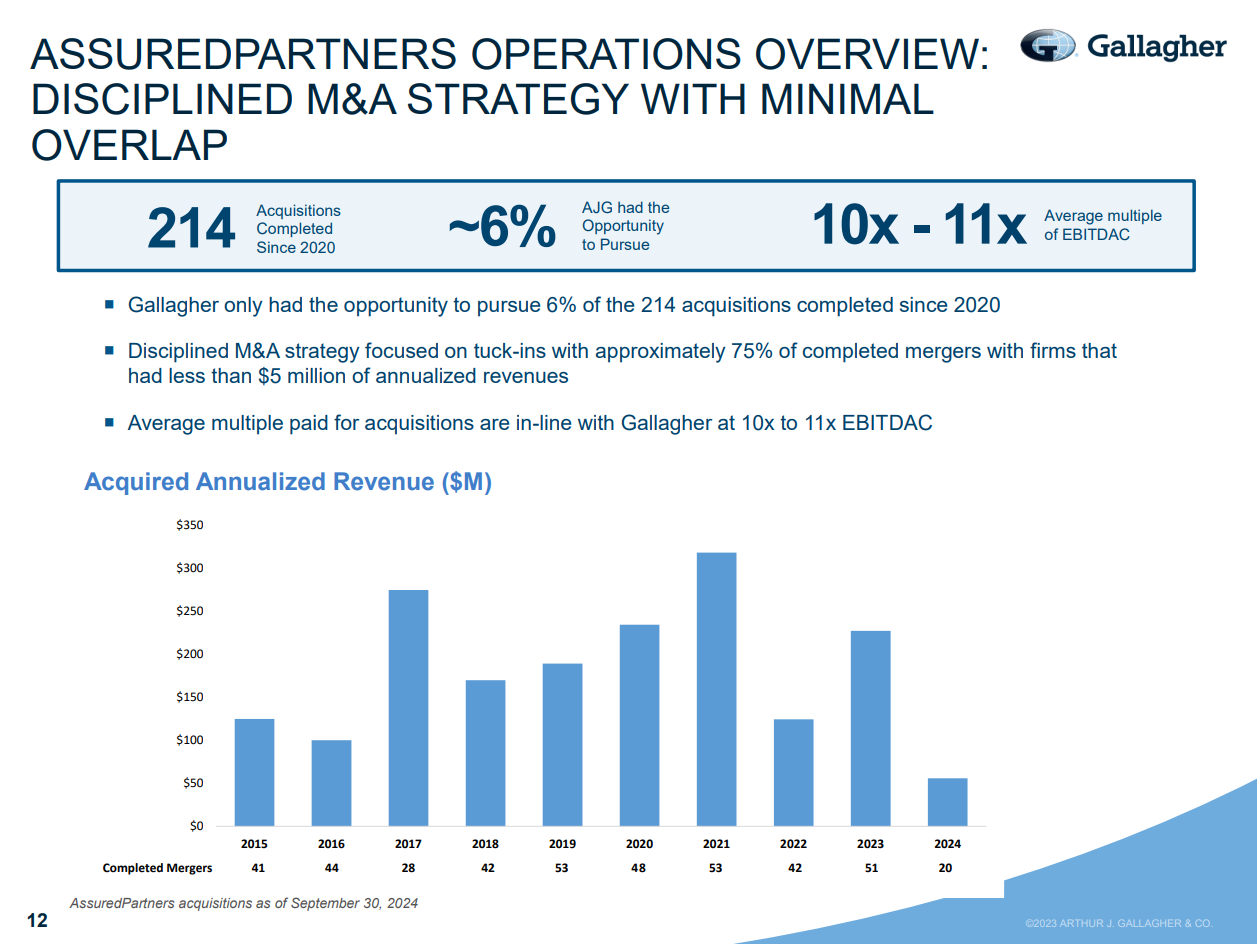

Additive to M&A

The acquisition will also likely add to AJG’s M&A pipeline rather than subtract from it. AJG analyzed the deals done by Assured and found that for 94% of their acquisitions, AJG never even got a look.

I think it’s just as exciting as it can be. I mean we’ve got 50, 60 people that do this [M&A] all day. We’ve looked at their pipeline and our pipeline, there’s not that much overlap, which surprised me. And actually, when I looked at the data that was put together for this presentation and realize that 94% of their acquisitions, we never even got to look at, these guys are pretty good. I mean, I can't believe they could get that many done without someone popping their head up and saying, and saying “Hey, I wonder if Gallagher is interested.”

So they did a pretty good job in the marketplace. And we look at—if you look at itthis way, Greg, we’re doing something on the order of 50 to 60 of these things a year. As you know, most of these are tuck-ins at less than $10 million in revenue. They fit right in. They’ve got a pipeline that is very similar.

Most of it is sourced in locations that they have in the field, which is a little different than ours, which I think is a good example for our people. And I think you add them together, could we maybe do 100 deals a year, 110? I think we could. And I think that’s a real positive. So their pipeline added to our pipeline is as excited as I’ve been on the quarters telling you that we’ve got $1 billion in motion.

This is going to be very additive.

AJG’s CFO Doug Howell also added that fewer acquisitions is not going to be a cost or side-effect of acquiring Assured:

We’re trying to do 100, 120 deals a year. Between the two, there’s 25,000 opportunities out there for us to knock on doors and say, “Would you like to be a part of our family and use our resources, our capabilities, all the tools you get overnight by joining Gallagher?” So I think our story is going to resonate more. I think that the opportunities are immense. So I think the two teams will come together and I think that the way we’re financing this, we’re not … shutting down our acquisition pipeline to pay for this deal.

Summary

The sales and service culture at Gallagher remains on full display and is exciting as ever. The opportunity to grow organically, and inorganically, even after this large acquisition, remains large. As Patrick and Doug noted in the call, the number of acquisitions of small and mid-sized firms per year could increase to more than 100. As an outsider, the positive attitude remains infectious—in a good way. I can’t imagine what it feels like to an actual member of the AJG team. The company continues on in the tradition of Jack Gallagher and his descendants.

Please Subscribe

If you enjoyed this content, please share and subscribe.

Disclaimers

The content of this publication is for entertainment and educational purposes only and should not be considered a recommendation to buy or sell any particular security. The opinions expressed herein are those of Douglas Ott in his personal capacity and are subject to change without notice. Consider the investment objectives, risks, and expenses before investing.

Investment strategies managed by Andvari Associates LLC, Doug’s employer, may have a position in the securities or assets discussed in any of its writings. Doug himself may have a position in the securities or assets discussed in any of his writings. Securities mentioned may not be representative of Andvari’s or Doug’s current or future investments. Andvari or Doug may re-evaluate their holdings in any mentioned securities and may buy, sell or cover certain positions without notice.

Data sources for all charts come from SEC filings, Koyfin, and other publicly available information.