History of Booz Allen Hamilton: Part II

Going Public, Going Private (1970-1980)

We now pick up from where we left of in Part I of BAH’s history. Booz Allen in 1962 had converted from a partnership to a corporation to implement profit-sharing and retirement plans for its partners. Arthur D. Little, another consulting firm with a rich and long history, went public in 1969. It was now time for Booz Allen to go public.

Booz Allen in the 1970s

In January of 1970, Booz Allen Hamilton decided to go public with an initial offering of 500,000 shares at $24 per share. The “partners” of the firm were the source of the shares to the public and thus the company did not raise any new capital in the process. James Allen and Charlie Bowen had retired, but both remained on the board of directors after the IPO. James “Jim” Taylor became president and started leading the firm in 1970.

Another reason behind the IPO was to have a currency with which to acquire other specialized consulting businesses to help diversify its business lines. Between 1969 and 1972, Booz Allen acquired several small firms involved in areas such as transportation, household chemicals, airport management, real estate, market research, and television advertising testing. In 1972, the firm also established a Japanese subsidiary, further expanding its international presence.

During the early 1970s, Booz Allen’s subsidiary, BAARINC (Booz Allen Applied Research Inc.), continued to gain a reputation in space systems work. This was thanks in part to its report in 1966 that predicted the failure of the NASA Orbiting Astronomical Observatory. NASA rejected the study and and launched it anyway. The satellite failed after just one day in orbit. Ever since, Booz Allen was consulted for its technical recommendations to increase satellite life spans.

However, despite success in consulting and technological assignments, the early 1970s presented many challenges. The economy went into a recession. Government assignments leveled off as the Vietnam War wound down. Commercial work suffered during the highly inflationary period, as consulting services became a discretionary budget item for many companies. Booz Allen’s broad range of services had also fallen out of favor with clients seeking specialized expertise.

Finally, the firm in 1972 learned distressing facts from an internal study it conducted on its own capabilities:

“[T]he firm’s leadership asked three young partners—Dick Reagan, Paul Anderson, and Al Meitz—to study the firm’s administrative capabilities. They got permission to analyze Booz Allen’s prospects as they might for a client, and what they found was sobering: if nothing changed the most valued partners would leave.”

—Booz Allen Hamilton: Helping Clients Envision the Future (page 59)

The immediate effect of the RAM report (acronym for Regan-Anderson-Meitz) was that Jim Taylor resigned as president in January 1973. The firm named 42-year-old James Farley to replace Taylor as president.

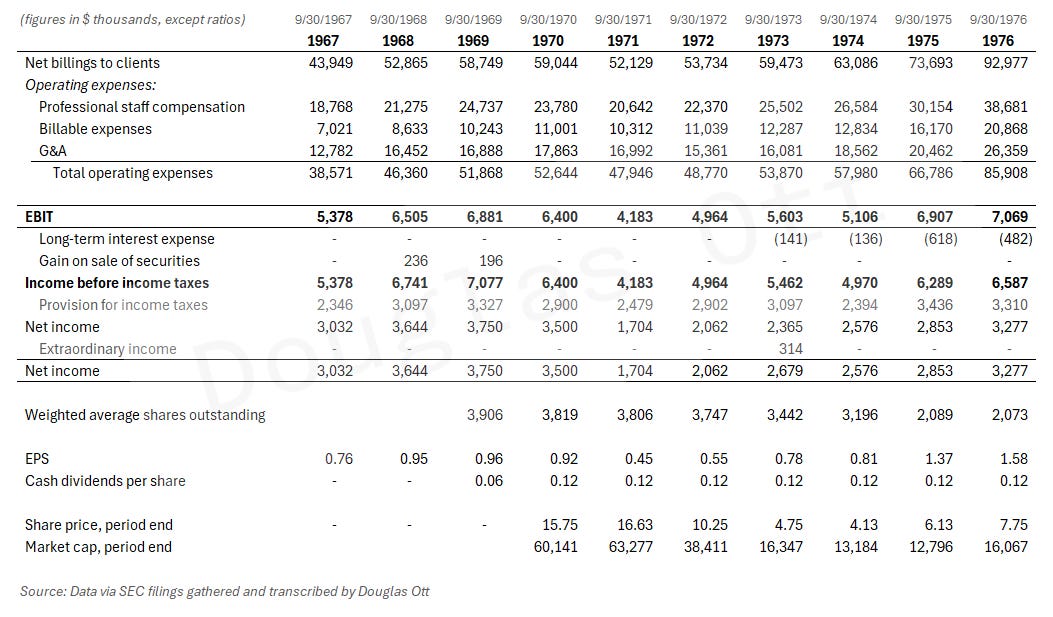

BAH’s Financials: 1967-1976

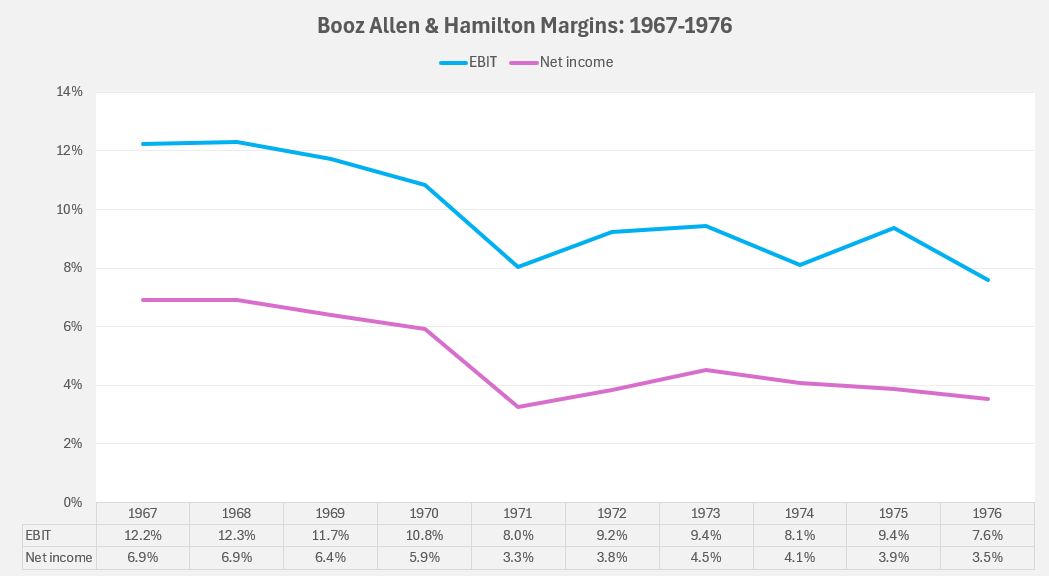

To put all the above in terms of financial effects, Booz Allen’s profit margins had decreased and its stock prices declined for several years. The financials below come directly from SEC filings I collected for this period. Although BAH’s revenues (net billings to clients) grew during the entire period, you can see the dip in margins and revenues begin in 1971 to 1972.

Furthermore, BAH’s revenue composition by client type more or less stayed the same. Roughly 60% of revenues came from state and federal entities and the rest came from commercial, educational, health, and non-profits.

Despite overall revenue growth for the entire period, profit margins shrunk.

With a decline in margins, and due to the highly inflationary period, BAH’s share price declined from its IPO price of $25 per share in 1970 to below $5 per share. BAH’s share price remained between $4 and $6 between 1973 to 1975. The P/E ratio compressed from the 20s and 30s to just 5x.

With little to no debt and a highly cash generative business, management decided to take advantage of the market’s undervaluation of BAH. The company began to repurchase shares beginning in FYE 1971. As time went on, the repurchases became more aggressive (note well—BAH started out in 1970 with 3.9 million shares):

FYE 1972 — BAH repurchased 136.2 thousand shares

FYE 1973 — BAH repurchased 54.5 thousand shares in the open market in addition to completing a tender offer for 258.5 thousand shares

FYE 1974 — BAH repurchased 76.4 thousand shares in the open market in addition to completing a tender offer for 1.77 million shares

With shares trading at a ridiculous price of less than $5 even after BAH retiring over 50% of shares, the company’s shareholders approved on August 5, 1974, the “1974 Officer Stock Purchase Program”. Under the terms of the program, up to one million shares of the common stock of BAH could be sold to officers of the company or its subsidiaries.

For officers of BAH choosing to participate, the terms were excellent (emphasis mine):

“The price per share is payable one-tenth in cash and the remainder with an unsecured promissory note (the “Note”). Notes will mature on the ninth anniversary of the purchase date and will be payable in nine equal installments on each anniversary of the purchase date. Notes will bear interest on the unpaid balance at the annual rate of five percent payable on each anniversary of the purchase date. Purchasing officers (or their estates) will have the right to prepay at any time the entire, and from time to time any portion of the, unpaid principal of the Note, together with interest accrued to the date of such prepayment on the amount of principal so prepaid.

…

As part of its compensation program, the Company will forgive on each anniversary of the purchase date five percent of the purchase price per share (but not accrued interest) by crediting such amount against payment of the installment of principal of the Note due on such date if, and only if, the purchasing officer is on such date, and has been at all times during the preceding 12 months, an active officer.”

Unsurprisingly, 115 officers of BAH participated in this program. They collectively purchased 871,500 shares for a total cost of $2.93 million, or a weighted average cost of just $3.36 per share.

At this point, management, officers, and directors of BAH owned about 59% of shares outstanding. They decided in 1976 to take the company private again and thus offered all other shareholders $7.75 per share in a leveraged buyout. The buyout price was double what officers had recently paid for their new shares of BAH a year earlier.

Fire in the Belly

Ostensibly, BAH management took the firm private again to allow for reorganization and long-range investments, which might not have been palatable for a company beholden to public shareholders. Another reason behind going private was the passionate belief of James Farley that it was necessary to put “the fire in the belly” again of the officers and partners as well as to rekindle “a partnership spirit.” A final, and unsaid, reason was the unique opportunity for enormous wealth and value creation for BAH’s management and key employees.

After going private, James Farley was named Chairman (the fourth in the history of BAH) and CEO, and John L. Lesher became president. The return to private ownership also coincided with the beginning of a turnaround for the firm with its billings reaching $100 million at the end of calendar year 1976.

With 100+ partners with even more skin in the game (to pay off their personal debt from the 1974 compensation plan and to increase the value of their interest in the business), business rebounded.

Joseph Nemec Jr. remembers this initial period after going private again:

“The business grew because we were highly incentivized. We had meetings every Monday morning in New York, where we would ask each other: ‘What are you going to sell this week’ If you didn’t sell, we would not eat.’”

—Booz Allen Hamilton: Helping Clients Envision the Future (page 62)

Two years after going private, BAH had repaid most of the debt it had taken on for the LBO. Annual billings had increased by 20%.

Notable Projects of the 1970s

The mid and late 1970s saw Booz Allen expand its expertise in the telecommunications market. For example, it conducted studies for AT&T on the telecommunications market and the Bell telephone system. The firm also embarked on a significant seven-year assignment for the city of Wichita, Kansas, to help establish a prototype municipal computer information system, which brought national recognition. This period of technological diversification led Booz Allen into new, specialized markets, including communications security, strategic and national command and control systems, and intelligence systems. A key outcome of this focus was a contract to work on the Tri-Service Tactical Communications Program, involving the coordination of U.S. Army, Navy, and Air Force communications.

In 1978, BAARINC changed its name to Public Management & Technology Center (PMTC), later known as the Technology Center. PMTC refocused its services on office automation, manufacturing technology, and space systems, leading to work on the commercialization of space stations. PMTC diversified into new markets like nuclear survivability, electronic systems engineering, avionics, and software verification and validation, offering clients cost containment and flexible pricing options. Key contracts for PMTC included Navy assignments to help develop the Trident missile and help rebuild Saudi Arabia’s navy.

Perhaps the most notable assignment Booz Allen received in the late 1970s was helping Chrysler Corporation in a historic turnaround by devising a plan to secure federal loan guarantees and then serving as a troubleshooter after the bailout.

One of the last notable changes for BAH was the sale of three research units to Burke International Research Corporation in 1979. The three units that no longer fit within firm were: AdTel, an advertising copy research company; Market Audits, which did in‐store audits; and BAMIS, a telephone research unit.

Summary

The period between 1970 and 1980 was yet another dynamic era for Booz Allen Hamilton. It went public in 1970, encountered tough economic times, and the share price fell from $24 to less than $5. Under the leadership of James Farley, new life was breathed into the firm. BAH aggressively repurchased shares, retiring over 50%—and partners and officers purchased shares for themselves near all-time lows in 1975. Then they took the firm private again in 1976 in the largest LBO ever for a management consulting firm at the time.

Laden with debt and with their personal wealth tied even more tightly to the value of the entire firm, partners and officers at BAH now had an increased desire for growth and profitability. This desire, coupled with an economy that was returning to growth, enabled: the recovery of BAH’s commercial and government consulting businesses; the firm receiving high profile assignments from AT&T and Chrysler; and the expansion of BAH’s international opportunities.

Please subscribe to the Andvari Substack so you will be notified of the release of Part III of this history on Booz Allen.

And if you missed out on Part I of this series, you can find it here:

History of Booz Allen Hamilton: Part 1

“The business of advising management is based on the principle that companies, like people, are generally unable to see themselves as others see them. The soundness of the principle is proved by the fact that the management-consultant business, which has been expanding for years, is booming as it never has before. U.S. industry is now paying at least $6…

Sources and Further Reading

“Pentagon Forms Cost Study Group; Aim Is to Improve Efficiency of Any Major Build-Up”, New York Times, May 28, 1969.

“Booz, Allen Files Offering of Stock”, New York Times, Dec. 12, 1969.

“Booz, Allen and Salomon Fill Key Positions”, New York Times, Sept. 29, 1970.

“Paper Shifts On Ads of Reviews”, New York Times, June 22, 1979.

“Chrysler To Submit New Plan”, New York Times, Sept. 22, 1979.

“Carter Urges Plan to Back $1.5 Billion in Chrysler Loans”, New York Times, Nov. 2, 1979.

Kleiner, Art. Booz Allen Hamilton: Helping Clients Envision the Future. Old Saybrook, Conn.: Greenwich Pub. Group, Inc. 2004.

“Booz Allen & Hamilton Inc.”, Encyclopedia.com, accessed March 12, 2025.

“Booz Allen & Hamilton Inc. History”, FundingUniverse.com, accessed March 12, 2025.

Disclaimers for this Substack

The content of this publication is for entertainment and educational purposes only and should not be considered a recommendation to buy or sell any particular security. The opinions expressed herein are those of Douglas Ott in his personal capacity and are subject to change without notice. Consider the investment objectives, risks, and expenses before investing.

Investment strategies managed by Andvari Associates LLC, Doug’s employer, may have a position in the securities or assets discussed in any of its writings. Doug himself may have a position in the securities or assets discussed in any of his writings. Securities mentioned may not be representative of Andvari’s or Doug’s current or future investments. Andvari or Doug may re-evaluate their holdings in any mentioned securities and may buy, sell or cover certain positions without notice.

Data sources for all charts come from SEC filings, Koyfin, and other publicly available information.