Flat For Four Years: Hangover Stocks

IDEXX Laboratories, Brown-Forman, and Pool Corporation

There are many high quality businesses out there right now whose share prices have gone nowhere for the last four or five years. IDEXX, Brown-Forman, and Pool Corporation are just several. Despite the overall stock market making new all-time highs, these three companies have had their results and their share prices pressured for a few similar reasons. One is related to the enormous demand during 2020 and 2021 that was pulled forward from the future. Another has been from the simmering inflationary pressures over the last few years.

Here they are.

IDEXX Laboratories

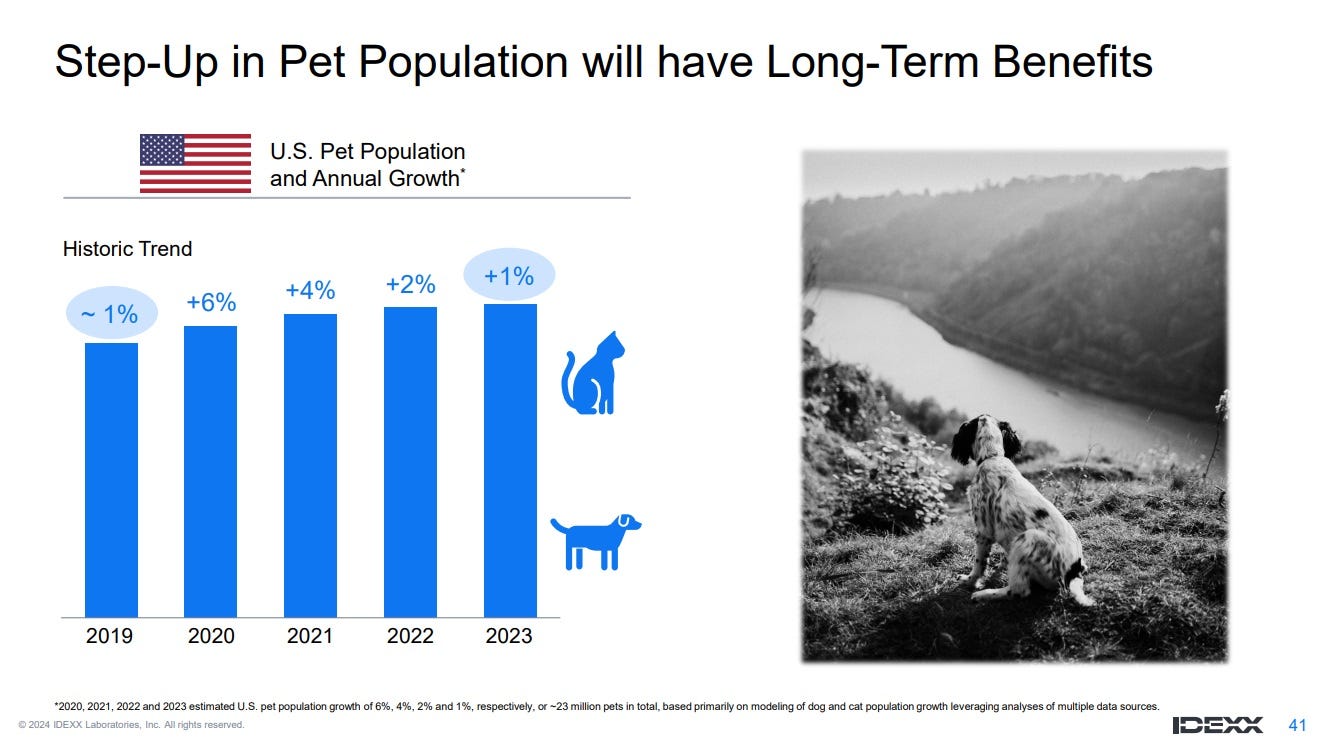

IDEXX Laboratories (IDXX) is a global leader in veterinary diagnostics, software, and water microbiology testing. They saw accelerated growth during the COVID years as more people purchased or adopted cats and dogs. Prior to COVID, the pet population in the U.S. had been increasing at a rate 1% annually. Then in 2020 and 2021, the pet population grew 6% and then 4%, respectively. Since then, the pet population growth has fallen back to its historical 1%.

Another factor that has weighed on IDEXX is the fact that the growth of clinical visits by pets has been slightly negative since the beginning of 2022. This is something the management team at IDEXX has admitted they had not expected to happen.

IDEXX management believes the lower than expected total visits by pets to clinics are explainable by two reasons. One is that vet clinics continue to suffer from capacity and staffing challenges. The total hours of work put in by vet clinics have declined since 2022 and this has not yet come back to the levels seen in 2020 and 2021. Management also thinks more pet owners have been pinching pennies due to the effects of inflation.

The period of high optimism during the COVID years contributed to an extraordinarily inflated valuation for IDEXX. The EV/EBITDA multiple reached a peak of 65.9x in the summer of 2021. Now, the EBITDA multiple is at COVID lows as the company deals with the normalization of pet population growth and the short-term headwind of fewer clinic visits.

Brown-Forman

Brown-Forman (BF.B) is a spirits company that owns the formidable American whiskey brands of Jack Daniels and Woodford Reserve. The company also has in its portfolio the tequila brands of El Jimador and Herradura—as well as a few other brands in different spirits categories. Thanks to good, multi-generational stewardship from the founding family, Brown-Forman has been an excellent business that has rewarded shareholders amply over the very long-term.

However, Brown-Forman is another company that is still dealing with a COVID hangover. Reported and organic growth remains negative or flat across its major categories.

The reasons for the current headwinds are similar to what IDEXX is dealing with. First, spirits sales are still normalizing since the spike in demand caused by COVID.

CEO Lawson Whiting recently explained the destocking dynamic the company is wrestling with:

“But consumers bought a lot of bottles in that ‘21, ‘22, first half of ‘23 time period. And some of those bottles are still sitting in their cabinet at home. And … a lot of people have said, well then, when is that going end? And … that is a tough question.

Generally speaking, … about 80% of consumers in the United States drink about two bottles a year at home. And so then you’ve got to estimate how many bottles do they have at home…. I know I’m tying together a few dots that are not that easy to tie together. But I would say that the turnaround ought to be coming relatively soon.”

Brown-Forman also continues to deal with inflationary pressures. This hits the company both on their costs of labor and materials as well as on the sales front. More consumers have been trying to save money for more essential goods and services.

We see these headwinds play out in the financials and share price of Brown-Forman. Over the last five years, the EBITDA margins have declined from the mid-30s to 29.5%. The EBITDA multiple has declined from a high of 34.4x in June of 2021 to now 18.9x. The share price has gone slightly down over this period and sits at levels last seen during COVID.

Pool Corporation

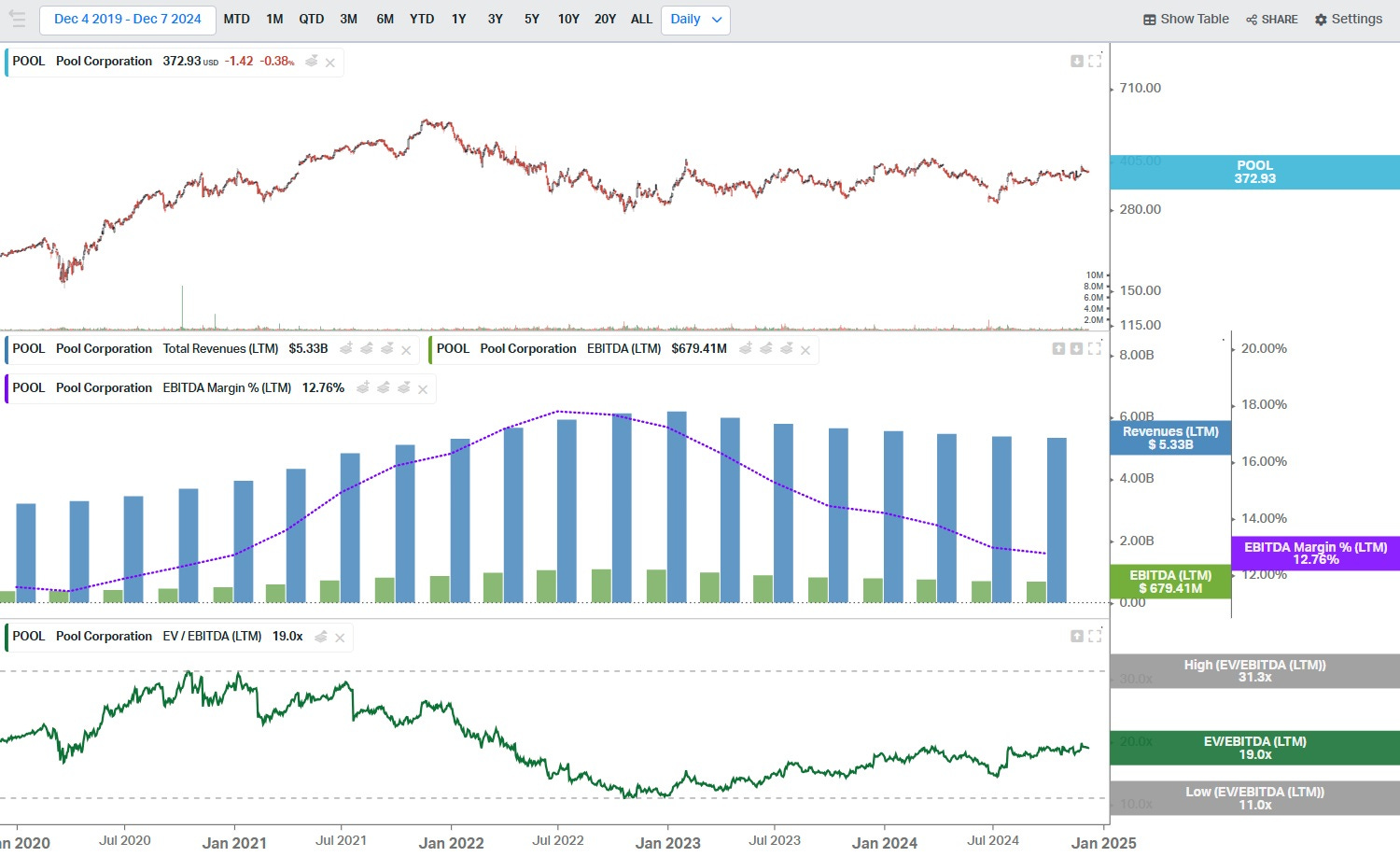

Pool Corp (POOL) is our last example of a business continuing to experience a hangover from 2020 and 2021. (Andvari Associates wrote about Pool in its Q2 2024 Letter). Pool is one of the largest distributors of pool supplies and equipment in the United States and Europe. During COVID, homeowners pulled forward a large amount of future demand. The number of new pools built in the U.S. increased in 2020 and then peaked in 2021 with 117,000 new pools built that year. Since the 2021 peak, the number of new pools built has declined each year. For 2024 new pool construction could be down nearly 20%.

As a result of this headwind, quarterly sales growth at POOL has been negative each quarter since Q1 2023. Rolling twelve-month EBITDA margins peaked in the summer of 2022 at and have declined to 12.8%. The EBITDA multiple has also declined 39% from a high of 31.3x in 2020 to 19x as of right now.

However, the silver lining for Pool is there are now more pools than ever that need continual maintenance and products related to remodeling. These product areas make up 86% of Pool’s revenues while supplies related to new construction make up only 14% revenues. It seems likely that its just a matter of time before Pool’s COVID hangover subsides and it returns to positive sales and margin growth. Over the long-term, Pool’s management expects the pool supply industry to resume growing at 4%-6% and that Pool itself will be able to grow faster than the industry by taking market share and through acquisitions.

Summary

These three companies are unique given how they all operate in separate, unrelated industries. However they all share many negative and positive traits. In the positive column, they are all leading companies in their respective industries with long-term tailwinds. IDEXX benefits from a growing pet population and increasing willingness of pet owners to spend more and more money on their “furry family members.” Brown-Forman has great spirits brands that will continue to spread and grow throughout the world as more people gain disposable income. Pool Corp will continue to benefit from a growing installed base of pools and will continue to gain market share as the largest and best distributor of associated products.

However, in the negative column, all three continue to experience short-term headwinds related to the COVID years. Much demand was pulled forward by the customers of all three companies. Inflation has increased costs and weakened the demand from consumers. The hangover has continued longer than management and shareholders expected, but this is often where the patient and enterprising investor can find excellent opportunities.

Please Subscribe

If you enjoyed this content, please share and subscribe.

Disclaimers

The content of this publication is for entertainment and educational purposes only and should not be considered a recommendation to buy or sell any particular security. The opinions expressed herein are those of Douglas Ott in his personal capacity and are subject to change without notice. Consider the investment objectives, risks, and expenses before investing.

Investment strategies managed by Andvari Associates LLC, Doug’s employer, may have a position in the securities or assets discussed in any of its writings. Doug himself may have a position in the securities or assets discussed in any of his writings. Securities mentioned may not be representative of Andvari’s or Doug’s current or future investments. Andvari or Doug may re-evaluate their holdings in any mentioned securities and may buy, sell or cover certain positions without notice.

Data sources for all charts come from SEC filings, Koyfin, and other publicly available information.