Crossing Bridges Before Coming to Them

Booz Allen Hamilton and Lessons From Sequestration in 2013

“There are more things likely to frighten us than there are to crush us; we suffer more often in imagination than in reality.”

—Seneca

There are a few natural laws that apply to the markets. For example, one natural law is that when interest rates go up, bond prices go down. Another law is that everyone hates uncertainty.

Uncertainty has been unleashed once again. The new administration in the White House has pledged to cut budgets and root out wasteful spending. With a steadily increasing budget deficit, enormous programs like social security and healthcare that are seemingly untouchable, there does need to be cutting and readjustment.

As a result, a few public company sectors have taken big hits over the last few months. One sector is the defense contracting companies such as Lockheed, General Dynamics, and L3Harris. The other sector is the government consulting and solution provider firms, with one in particular taking a wallop to its share price: Booz Allen Hamilton (BAH).

Booz Allen Hamilton

BAH was founded in 1914 by Edwin Booz, one of the pioneers of management consulting, and originally had the name Business Research Service. Early clients included U.S. Gypsum, Goodyear Tire & Rubber, Chicago’s Union Stockyards and Transit Company, and the Canadian Pacific Railway. In 1940, the firm began serving the U.S. government by advising the Secretary of the Navy in preparation for World War II.

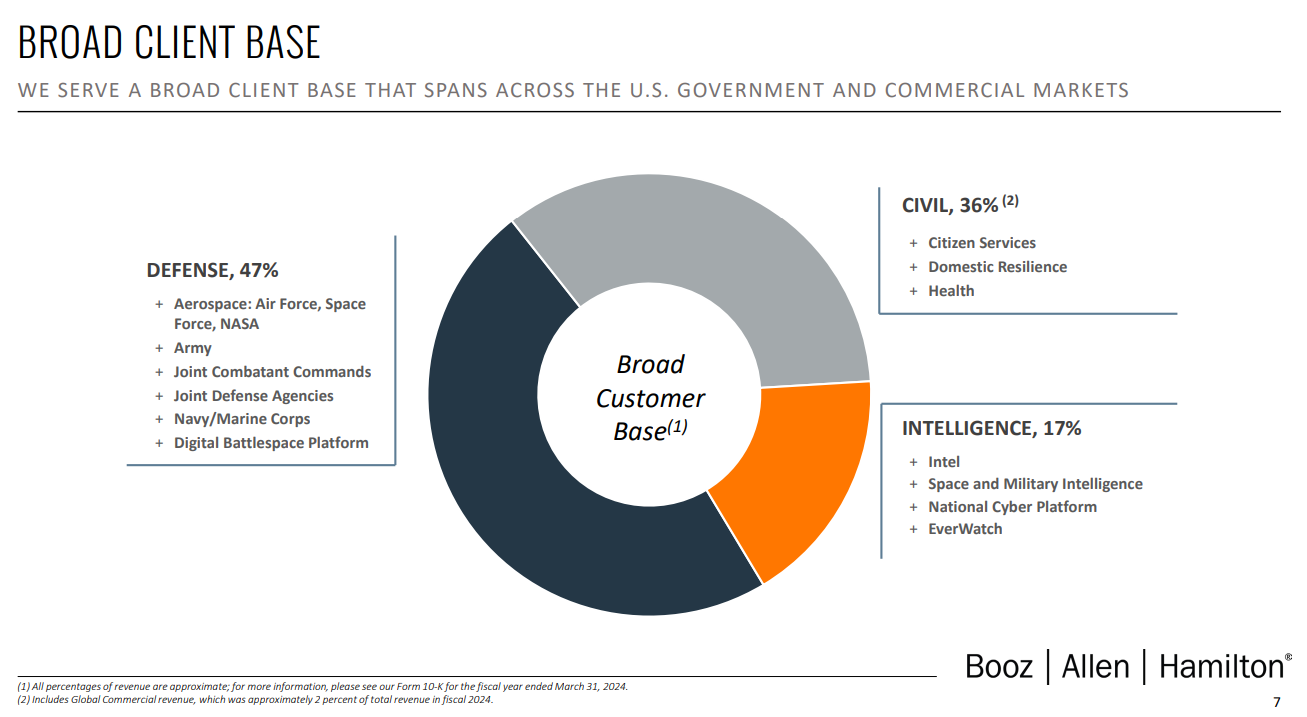

Over the last 110 years, BAH has continuously grown. Over the last twelve months, the company earned $11.8 billion in revenues, $1.4 billion of EBITDA, and $844 million in free cash. The company specializes in providing services and overseeing large projects mostly to the U.S. government. Over 64% of their business serves the defense and intelligence sectors while 36% is for the civil market.

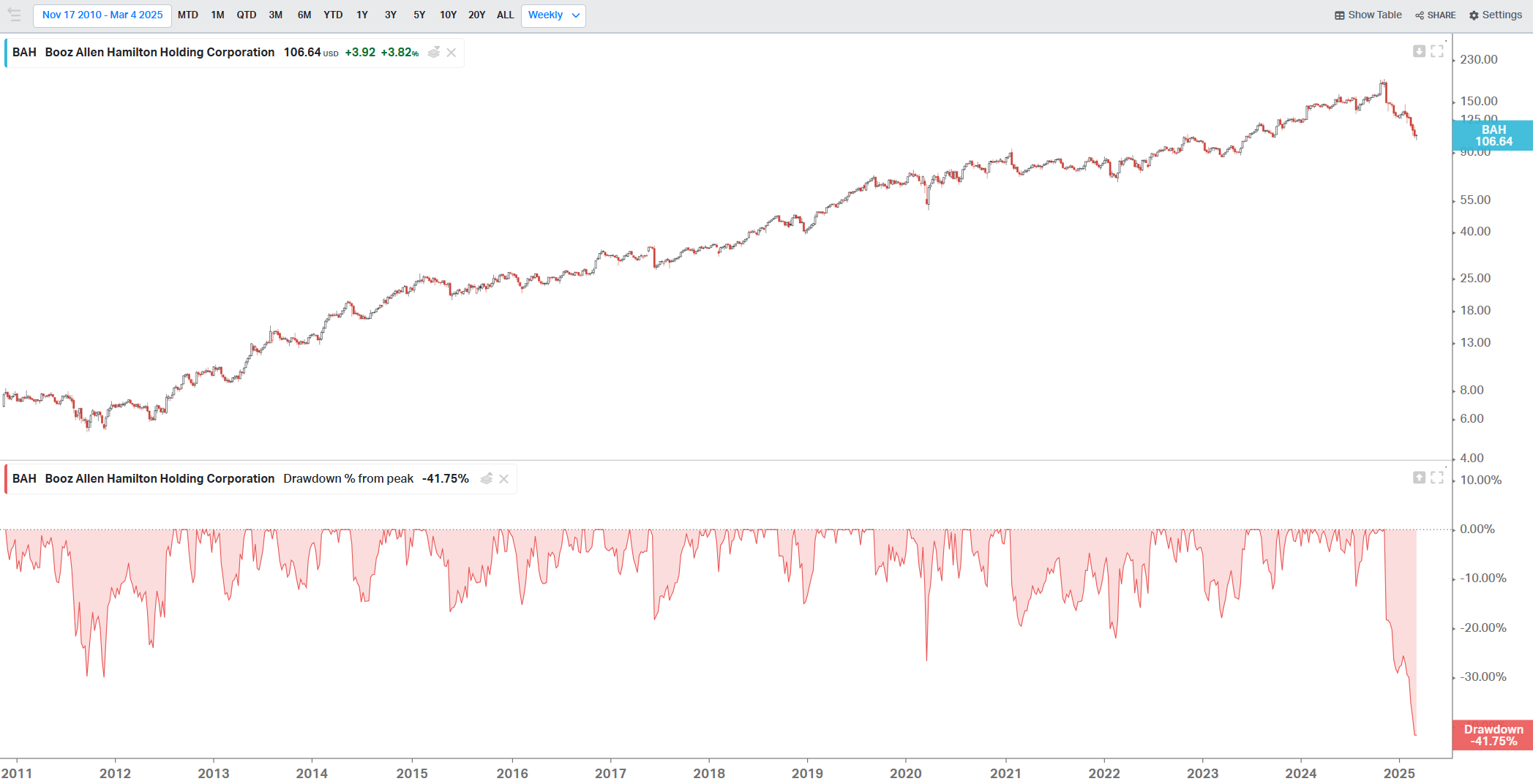

With the advent of DOGE and government budget uncertainty, and such a heavy tilt to serving various branches of the federal government, it is no wonder BAH’s share price has taken a big hit since last November. It is now in its largest drawdown (down 41% from its all-time high) since the fiscal and sequestration worries that dominated headlines from late 2011 through early 2013.

Looking back to the last period of extraordinary fiscal uncertainty, BAH’s share price reacted in a similar negative fashion as today.

Sequestration of 2013

Below, I created a chart showing various headlines from the New York Times as well as quotes from BAH executives during the lead up to—and the aftermath (if you can call it that) of—sequestration.

The prior period of uncertainty lasted roughly from 2011 to the end of 2012. During this time, investors in government contractors got to experience the effects of fun headlines like these on their holdings:

“War of Ideas on U.S. Budget Overshadows Job Struggle”, NYT, June 3, 2011.

“Debt Ceiling Impasse Rattles Short-Term Credit Markets”, NYT, July 28, 2011

“Panetta Pleads for No More Cuts in Defense Spending”, NYT, Aug. 4, 2011.

“Low Expectations, and Trepidation, Over Meeting a Debt Deadline”, NYT, Nov. 17, 2011

In preparation for sequestration, BAH’s plan was to make its costs as variable as possible to protect its margins in case revenues declined:

“[W]e started a … strategy several years ago to get ourselves in the position to get our costs as variable as we could make it. And so our commitment is to ensure that we continue to manage our costs in relation to our revenue. … But in this environment, we realize that’s going to be difficult, particularly through the balance of the government fiscal year ‘14 if the government goes into sequestration. So our commitment is to make sure that we stay agile and responsive so that we can protect the margins we have even if revenue does take a hit from sequestration or government shutdowns or whatever.”

—Samuel Strickland, CFO of BAH, 1/30/2013

When sequestration finally and officially took effect on March 1, 2013, BAH’s share price went up. And then the next leg up for BAH’s share price started in February 2014 after the legislative branch approved higher debt limits for the U.S. government.

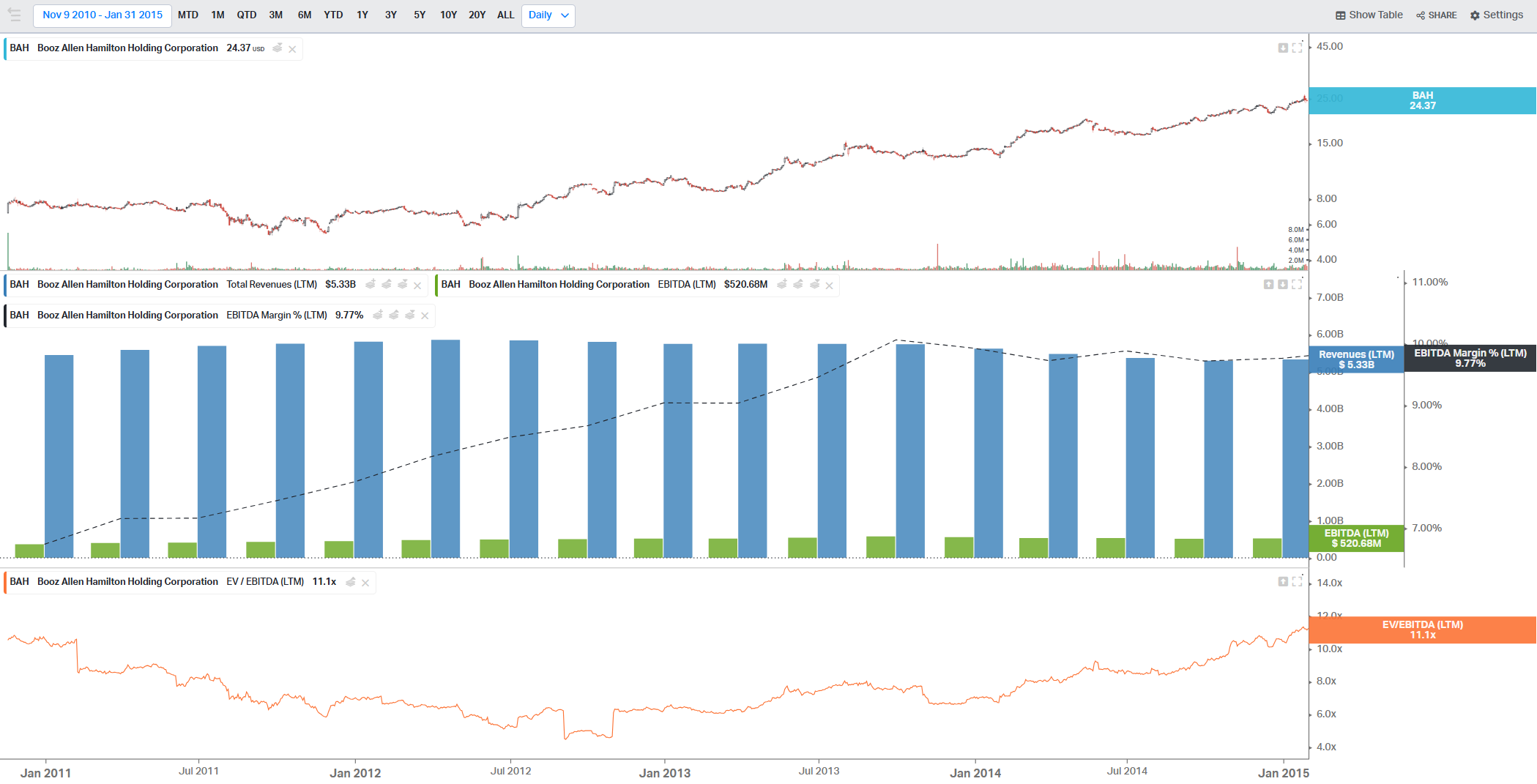

True to the words of BAH executives, BAH maintained and improved margins while LTM revenues declined from $5.8 billion to $5.3 billion.

Uncertainty and Certainty

Part of the appeal of almost any U.S. government contracting business is the dependability of revenues coming from a client that will always pay you and generally increases its spending on essential items over the long term:

“And while we cannot predict with any certainty, exactly what the budget situation is going to be, whether sequestration will occur or not occur, we know that there are a lot of essential functions that are still going to have to be performed by our federal government clients and we want to be in the center of that. We want to be providing the most essential services in the most high quality fashion that can be provided and therefore be very relevant to whatever work is going on. So for that reason, we have a lot of confidence in how we have invested in cyber and cloud and the markets that we have invested in. There is going to be still continued demand out there for Booz Allen service even in turbulent times.”

—Ralph Shrader, Chairman and CEO of BAH, 5/30/2012

Revenues did decline for a year before sequestration taking effect in March 2013. They also continued declining a bit afterwards as well. But even though it was a short- or -medium-term storm cloud for BAH’s business, the silver lining of sequestration actually taking effect was that people finally had certainty:

“It’s the uncertainty that really inhibits our clients from making long-term decisions in the government space.

And it almost doesn’t matter—in our business anyway—what the answer is, but it’s clarity, it’s certainty that makes a difference to our clients so that they can plan on which programs and which priorities they want to fund. And … that’s the whole reason the sequestration is so irrational. There have been programs inside DoD that the defense leadership wanted to cancel. And under sequestration, not only did they have to maintain them, they had to fund them at roughly 90% of the prior-year budget as opposed to saving all that money and redeploying it towards programs that were more important to their mission.”

—Kevin Cook, CFO of BAH, 1/3/2014

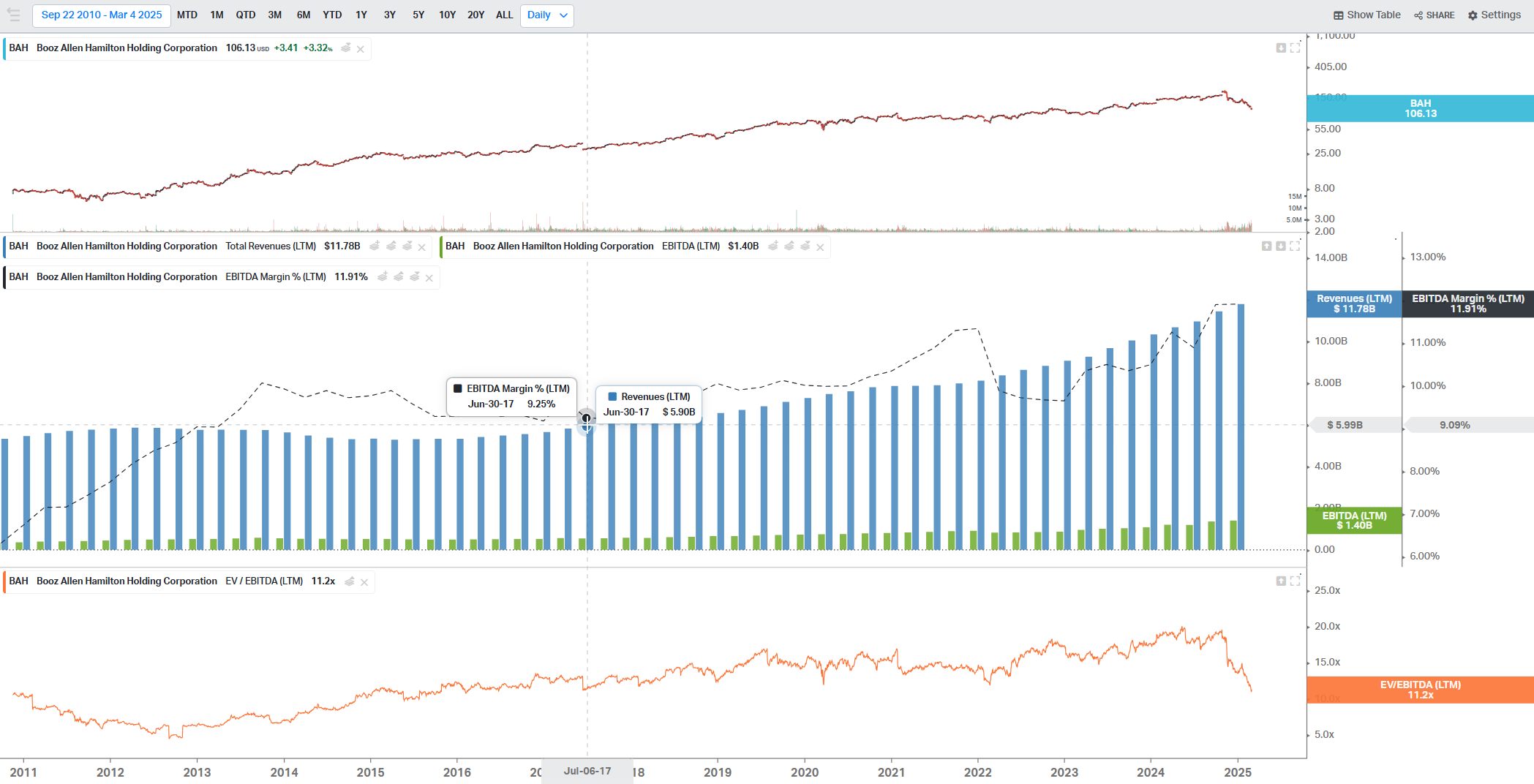

Trailing twelve month revenues at BAH would continue to slowly decline after March 2013. But they would begin to grow again and surpass the prior all time high of $5.8 billion by June 2017. BAH’s TTM revenues now sit at $11.8 billion and the company has undoubtedly attempted to make itself even more essential to the U.S. government over the years.

Looking below at the absolute and relative levels of defense spending by the federal government, the absolute level of spend troughed a few years after the 2013 sequestration began and then exceeded prior all-time highs in 2019.

The five year period from 12/31/2012 to 12/31/2017 was generally a good time to be a shareholder of the defense primes (and BAH) despite knowing that defense spending would shrink.

Nothing Ever Happens

Death and taxes. These two are certainties, forever and always. I posit a third is that nothing ever happens when it comes to government spending: it will continue to grow over the long-term despite any successful, short-term efforts to curb it. The federal government will cut a bit, it will reprioritize its programs, then spending will grow again when new projects and new contracts are awarded to continue providing vital services.

Knowing that nothing ever happens to the growth of government spending, it might be worthwhile for investors to stop drowning themselves in minutiae in an attempt to analyze the potential fiscal impacts on the companies that provide essential services and products to this country. Focus more on the big picture.

Frame by frame (suddenly)

Death by drowning (from within)

In your own, in your own analysis

Step by step (suddenly)

Doubt by numbers (from within)

In your own, in your own analysis

—“Frame by Frame” by King Crimson from their album Discipline (1981)I believe the odds are high the next five years will be a repeat of the 2011-2016 period for a company like BAH. They could very well endure some years of shrinking revenues, but they will defend their margins. Further, if the number of government employees does decline over the next several years, it is also likely that the services and expert consultants at companies like BAH will be in even higher demand. With a current backlog worth $41+ billion, BAH should be fine. And when growth in government spending resumes, so will the growth of BAH.

“Anticipating pain was like enduring it twice. Why not anticipate pleasure instead?”

—Robin Hobb

Please Subscribe

If you enjoyed this content, please share and subscribe.

Disclaimers for this Substack

The content of this publication is for entertainment and educational purposes only and should not be considered a recommendation to buy or sell any particular security. The opinions expressed herein are those of Douglas Ott in his personal capacity and are subject to change without notice. Consider the investment objectives, risks, and expenses before investing.

Investment strategies managed by Andvari Associates LLC, Doug’s employer, may have a position in the securities or assets discussed in any of its writings. Doug himself may have a position in the securities or assets discussed in any of his writings. Securities mentioned may not be representative of Andvari’s or Doug’s current or future investments. Andvari or Doug may re-evaluate their holdings in any mentioned securities and may buy, sell or cover certain positions without notice.

Data sources for all charts come from SEC filings, Koyfin, and other publicly available information.