Copart FY2024 Results

Dominant Online Vehicle Exchange Continues to Execute

With Copart recently reporting its full year 2024 results last week, I wanted to share some of my thoughts. Note well, I am a shareholder, so please read the disclaimer at the bottom of this post. The content of this publication is for entertainment and educational purposes only and should not be considered a recommendation to buy or sell any particular security.

Recent Results

Copart shares were down 6.7% the day after it reported its results for FY2024. Apparently, expectations were a bit high. The consensus estimate for the quarter were earnings of $0.36 per share compared to actual earnings of $0.33 per share. Consensus estimate for quarterly revenues was $1.081 billion compared to actual revenues of $1.068 billion.

Right now, Copart’s share price is unchanged since November 14, 2023. Its share price is currently about 15% below its all time high reached in April this year.

In general, Copart continues to execute well and its management continues to be distinguished in its industry (as well as virtually ever other industry) for its extraordinarily long term view towards managing the business and taking advantage of the opportunities that still lie ahead.

Thinking in Decades, Not Quarters

One of the several things Copart management has constantly repeated is they think about and manage their business in terms of decades. By doing this, Copart has earned the right from its insurance customers to have significant market share in North America.

Pinpointing market share is challenging given that Copart does not report this data. However, when IAA (Copart’s main competitor) was spun out from KAR Auction Services in 2019, KAR estimated that IAA had 40% share and Copart had 40% share, so this is the figure most people throw around.

But let’s move from 2019 to 2023 when Ritchie Brothers acquired IAA. Luxor Capital was against this deal and one of the reasons they cited was IAA had ceded significant share to Copart in the U.S. from 2016 to 2022. If data in the chart below is credible, then Copart now has more than 50% share, and perhaps upwards of 60% share in the U.S. by unit volume.

A prime example of Copart translating its long term ethos into action is the company choosing to own, rather than lease, the land for its salvage yards. Land ownership has given them greater control over many costs in the long run. And so, over the decades, Copart has assembled an irreplicable portfolio of real estate that serves as the bedrock of its core operations. Land purchased decades ago by Copart in a rural area outside of a city is now likely suburban or even urban. Today, it is nearly impossible for any salvage yard to obtain the necessary approval to operate in these areas. Several good locations in and around a metro area means lower transportation costs for Copart as well as an ability to handle greater volumes of vehicles more quickly.

[W]e run this business for the next decade, two decades, it’s not for each quarter. So we're not being reactive to any one specific market condition. Our balance sheet reflects that. We have been very disciplined around how we pursue investments investing in land, investing in our technology, investing in logistics.

All of that is on behalf of our customers, and we’re making sure that we’re doing that in a programmatic way that is very focused on long-term value creation.

Leah Sterns, CFO, June 7, 2023

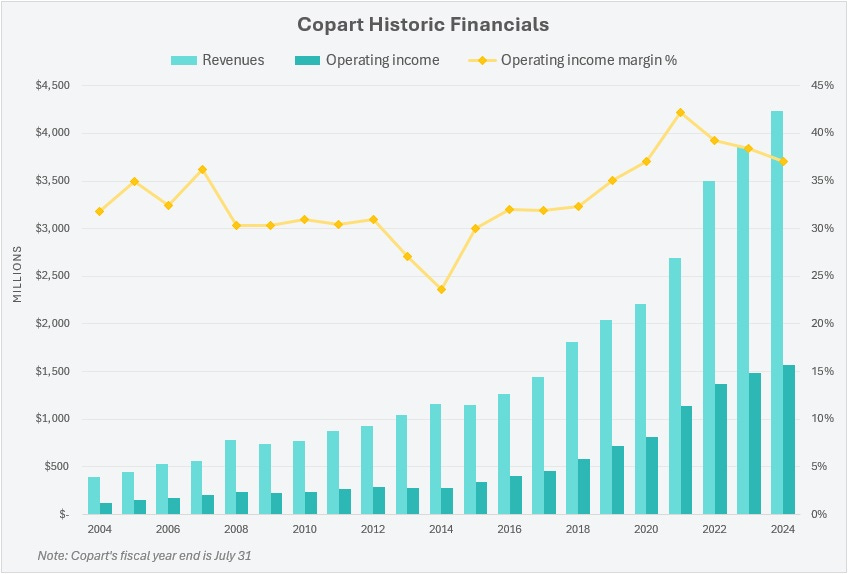

Speaking of Decades, Here’s Some Historic Results

For a company that helps connect buyers and sellers of damaged and salvage vehicles, the financial characteristics are surprisingly good. Below we see revenues going up 10.8x from FY 2004 to FY 2024. Operating income has gone up 12.6x and free cash flows have increased 19x in the same time.

What Are Owner Earnings?

My basic definition of owner earnings is the free cash left to the owner of a business after everything has been paid to maintain the business. Given that nearly all of Copart’s capex investments have been for growth, owner earnings should be higher than its free cash flows.

Growth Capex

Copart executives have frequently commented on quarterly earnings about the percent of capex that was for growth or capacity additions. In all years from the end of 2016 to the end of 2023, Copart has spent 75–90% of its capex to further grow its business. The remainder, 10–25%, is presumably the capex required just to keep the current operations running smoothly.

Q4 2023 Earnings Call, Leah Stearns:

“And in addition, during 2023, we invested nearly $517 million in capital expenditures with over 80% of this amount attributable to our physical infrastructure and more specifically, capacity expansion, which contributes to our ability to serve our customers, while simultaneously reducing our transportation costs, and corresponding fuel consumption.”

Q4 2021 Earnings Call, John North:

“We invested $98.6 million in capital expenditures for the quarter and approximately 76% of this amount was attributable to capacity expansion. For the year, we invested $463 million in CapEx of which approximately 85% was associated with capacity expansion.”

Q4 2020 Earnings Call, Jeff Liaw:

“As noted previously, we continued to invest in our business long-term with land as one critical dimension, but certainly not the exclusive one. We invested $112.7 million of CapEx in the fourth quarter alone, 90% of which was attributable to capacity expansion alone.”

Q4 2019 Earnings Call, Jeff Liaw:

“We generated operating cash flow for the quarter of $193 million with CapEx of $114.5 million, more than 90% of which was attributable to capacity expansion and lease buyouts. We continue our efforts to invest in land—to purchase and develop land to meet both current and prospective demand for our services.”

Q4 2018 Earnings Call, Jeff Liaw:

“CapEx in fiscal ‘19 will continue to be dominated by capacity expansion. So it will be land developments and acquisitions, in some cases, lease buyouts. So I think it was—the rough number, over the past 8 quarters, would be 85% or so of our CapEx has been for those ends.”

Q4 2017 Earnings Call, Jeff Liaw:

“CapEx was $47.5 million for the quarter, the vast majority again for land and development.… During fiscal 2017, we opened 11 new yards, 3 of which were outside of the United States. We expanded 15 existing facilities, and we opened 1 CAT yard, which is a nonoperational facility except in CAT event. In total, we added almost 700 acres of capacity. Our expansion activities will continue as we believe industry trends will drive significant future growth in volume.”

Q4 2016 Earnings Call, Jeff Liaw:

“CapEx of $30 million for the quarter and $173 million for the full year. Of that full year number of $173 million, approximately 75% was for land, lease buyouts and development, so in some sense, capacity or land acquisition.”

The Copart Cash Pile

Despite investing significant capital to grow its business, the cash continues to pile up. Further, Copart has been debt free since 2022. Net cash to operating income now stands at an all time high of 2.2x.

Although Copart’s reported total cash and investments is $3.4 billion, I believe the true value is somewhat higher. Why? Because of its strategic importance. To the largest and the smallest of Copart’s insurance companies, it gives assurance that Copart can weather pandemics and catastrophic weather events. That it will actually position its people and assets prior to a storm’s potential landfall, knowing full well that it might never touch land.

Jeff Liaw, CEO, provides additional color on the Q2 2024 Earnings Call:

“The one afterthought I’d offer is that our capitalization with our clients is a distinctive competitive advantage. Our conservative balance sheet, our net cash balance, equips us such that we can be patient even through a crisis. So in the midst of a pandemic, when nobody knew for how long driving an economic activity would be shut down, we were able to continue our business as it stands today. We didn’t lay off folks. We didn’t suspend CapEx, et cetera.

Our insurance clients have a long memory, and they know those things. They know that when land is available for us to acquire, so that we can preserve it for the industry’s use for the next 50 years, that we’ll do so gladly and proudly, despite it of course coming with big ticket prices as well.”

Jeff Liaw, CEO, Q4 2023 Earnings Call:

And we think the fortress balance sheet is of value to ourselves and to our clients. I think it positions us to act very aggressively when we see land purchase opportunities, for example. It equips us to respond to a pandemic in a way that a lesser capitalized company could not, right?

Another reason for Copart’s robust cash balance is the company’s discipline and high standards when it comes to deploying capital. If Copart had lower standards when it comes to returns and risk, I imagine the cash balance would be lower than it is today. In addition to the stringency of Copart’s capital allocation, management and many other employees at Copart have a business owner’s mindset, because they are owners.

Jeff Liaw, CEO, Q3 2023 Earnings Call:

[W]e’ve fielded a number of questions already from some of our analysts and investors about our growing cash balance, and I thought I’d address that question proactively here. I’ll start with our long-standing position and follow with a more nuanced current view. Our evergreen position is that we take our responsibility as stewards of capital seriously and evaluate prospective investments with an owner’s mindset because we are owners; from Willis Johnson, our Founder, to our newest employees who elect to participate in our employee stock ownership program.

And as we have done episodically but very substantially over the years, we ultimately return excess cash flow to our investors and subject to how the tax code evolves, generally in the form of share buybacks. Regarding where we stand specifically today, I do want to emphasize how the strength of our balance sheet empowers and differentiates Copart. In comparison to other participants in our industry, we do not prioritize interest payments, debt paydown, dividends or massive cost reduction initiatives.

Additional Avenues of Growth

Copart continues to invest heavily to increase its ability to handle greater volumes of damaged vehicles. It has had growth initiatives overseas in Germany and other European countries that still have not yet reached full potential.

More Services

Copart also continues to add valuable services to its core auto auction offering. One growth area is the vehicle titling process. Copart has become highly efficient at handling the process of obtaining and transferring vehicle titles between various parties. Because of its size, Copart handles more titles than almost any one of its customers. With scale comes efficiency. It’s the logical choice for any insurance company that does not have the same scale as Copart in titling to offload that function to Copart.

During Copart’s Q4 2024 earnings call, Jeff Liaw, CEO, explains how more insurance company customers are choosing to outsource parts of their operations to Copart:

“Another theme I’d like to highlight is the deepening of our relationships with our insurance company clients. As reflected recently in the ongoing expansion of our Title Express service offering.

Historically, auction houses like ours have obtained salvage certificates from the states in which we do business after the insurance companies have first obtained the original title either directly from policyholders if they own their cars outright or from lenders if the vehicles have claims outstanding. Insurance companies have always reasoned that for a pivotal touch point with their own customers, typically after a claims event, it would be best to keep this function in-house.

Today, however, our offer of an integrated one-stop solution for title procurement, which we call Title Express, has achieved substantial traction in the industry. On behalf of our carrier clients, we obtained original titles from policyholders and from lenders. Each state has its specific nuances in what it requires, as documentation, signatures, secured forms, powers of attorney and so forth. And each lender too has its own requirements for the provision of payoff balances and per diems and the releasing of clean titles.

The lender universe, in particular, is an especially fragmented constituency between our online lender portal AI-powered outbound calling systems and access to other intermediaries, we believe we offer a substantially more efficient title procurement process than our insurance customers can otherwise achieve.

Today, we’re pleased to note that we are approaching a run rate of 1 million titles obtained per year on behalf of our insurance clients, a testament to their trust in us to provide excellent service to them and importantly, to their own customers as well.”

Evolution of Services Offered by Copart (2003–2023)

Electric Vehicles

Are electric vehicles (EVs) a tailwind to Copart’s business or is it a headwind? One might logically think that with fewer total parts and with extra safety features compared to non-EVs, that there would be fewer accidents and collisions involving EVs. Thus, a current and future headwind to Copart. But I disagree.

First, despite growing adoption, electric vehicles (EVs) are still an insignificant portion of the entire vehicle population. According to CCC Intelligent Solutions, EVs “make up 1.1% of vehicles in operation (~3.3 million vehicles) while internal combustion engine vehicles account for 92% of the mix.” Further, EVs account for a greater proportion of repairable claims than their population would suggest. CCC again reports on recent claims data: “EVs represented 2.4% of all repairable claims in Q1 2024, up from 1.6% in Q1 2023 according.”

Second, despite having fewer parts, they certainly have more electronics and sensors. These are more expensive to replace and to calibrate. Adding to repair expenses for an EV is the fact it takes technicians longer to diagnose and repair the damage. And there still remains a shortage of trained EV technicians across the auto repair network. All these facts suggest an insurance company will more likely decide to total an EV, which will be good for Copart’s business.

Here is Leah Sterns, Copart’s new CFO talking about ADAS (Advanced Driver Assistance System) and EVs:

So ADAS is something that I think people when they hear it first think that will certainly bring down frequency of accidents. What we have found is it actually has driven an increase in accident severity, which is the underlying cost to repair a vehicle once it's been in an accident.

The reason for that is because the components required … for a car to have ADAS are extremely expensive to repair. And we found that the cost of the parts as well as the labor availability and the cost of that labor are continuing to increase.

In terms of EVs, … EVs tend to have a lot of ADAS components embedded in them. And that is another factor that we see in terms of EV as having a higher frequency of being totaled than a traditional ICE vehicle.

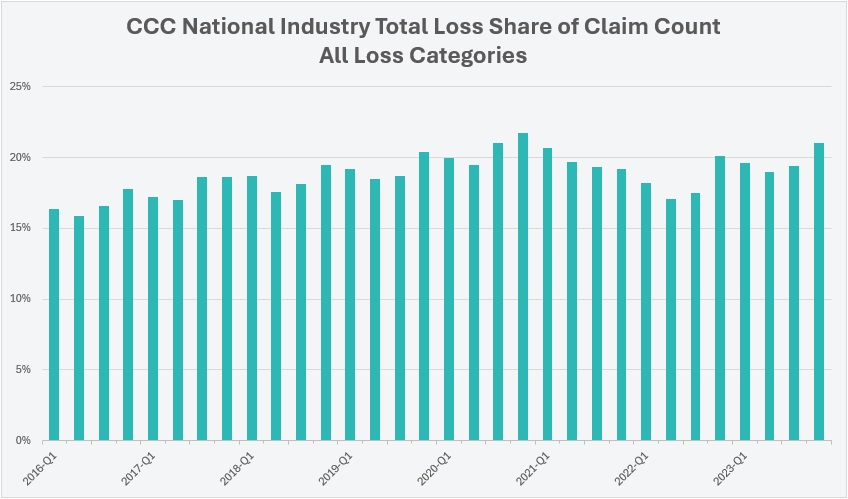

Whether the vehicle is electric or not, the trend remains that cars are getting more expensive to fully repair post-collision. Total loss rates will continue to go up which is a long term tailwind for Copart.

Learn more about total loss rates and the auto repair ecosystem in the below post

Takeaways

Copart continues to perform well, but the current valuation does seem to be on the expensive side. If investors continue to expect too much from the company, the share price could continue to slide downwards.

But in terms of the qualitative aspects of Copart’s business, there are three things I like the best:

Management that thinks in decades and acts accordingly;

A strong moat due to the network effects embedded in its core online vehicle bidding platform;

And a real estate portfolio that is likely impossible to duplicate.

I see a unique management team running a business with a moat surrounded by another moat. This is a great business worthy of your time for further study.

Please Subscribe

If you enjoyed this content, please share and subscribe.

Disclaimers

The content of this publication is for entertainment and educational purposes only and should not be considered a recommendation to buy or sell any particular security. The opinions expressed herein are those of Douglas Ott in his personal capacity and are subject to change without notice. Consider the investment objectives, risks, and expenses before investing.

Investment strategies managed by Andvari Associates LLC, Doug’s employer, may have a position in the securities or assets discussed in any of its writings. Doug himself may have a position in the securities or assets discussed in any of his writings. Securities mentioned may not be representative of Andvari's or Doug’s current or future investments. Andvari or Doug may re-evaluate their holdings in any mentioned securities and may buy, sell or cover certain positions without notice.

Data sources for all charts come from SEC filings, Koyfin, and other publicly available information.

copart is an amazing business and I’m a happy shareholder. good job capturing some of the insights into this gem.

Also, do you have any insights into how they are progressing in Germany and Western Europe? From reading the transcripts it sounds like execs are positive directionally but I don't have hard numbers. This could also be a growth area given them stating the market size is similar or greater than USA.